Terrific note from Charlie McElligott at Nomura who manages to cut through his usual robot babble to offer a precise take on what the Fed is about to do to markets:

- Simply a massive week ahead for markets, with Powell testimony and bunches of Fed speakers, along with US economic releases headlined by the market’s most important datapoint in the CPI release Wednesday, in addition to PPI, Retail Sales and Consumer Sentiment over the course of the week, plus two Duration-heavy auctions ($36B of 10Y and $22B 30Y, on top of tomorrow’s $52B 3Y),…and finally, US corporate earnings season kickoff (highlighted by JPM, C and WFC this upcoming Friday)

- Currently overnight we see a modestly-struggling attempt from USTs across the curve to consolidate the vapor-speed sell-off of the past 3 weeks (TY at least back to “unch-y” currently, after yields earlier blasted through 1.80), although ED$ Reds / Greens continue grinding lower as the market has now priced-in 3.5 Fed hikes by YE ‘22, while the sell-side in increasingly speaking to the potential of 4 hikes…of course in addition to recent “tie-breaker” bearish catalyst of outright Fed balance-sheet unwind beginning mid-year

- Upper left Vols / Gamma continues to bleed, however, as at this juncture, it would likely take some sort of further inflation or jobs upside surprise to “add more” Fed tightening than the substantial amount which has already been priced…meaning there is likely a modestly growing risk of an occasional day or two of counter-trend rally in Rates / USTs on “crowding” of bearish positioning alone

- Similarly, it is then worth highlighting that while TY and US Put Skews have continued to richen alongside the broad UST selloff YTD, FV Put Skew last week actually began to at least locally “plateau”

- JP Garry notes the richening in 2s10s Curve Caps to this point on increasingly “reversal risk” being picked-up by the market, particularly after curves have flattened so powerfully on the broad capitulation into “peak hawkish Fed” expressions….hence a steepening option / hedge in the case that the Fed would fail to deliver on such a path (either due to softening of, say, inflation data, OR financial conditions turbulence via “market tantrum” forcing the Fed to yet-again “Bend the Knee”)

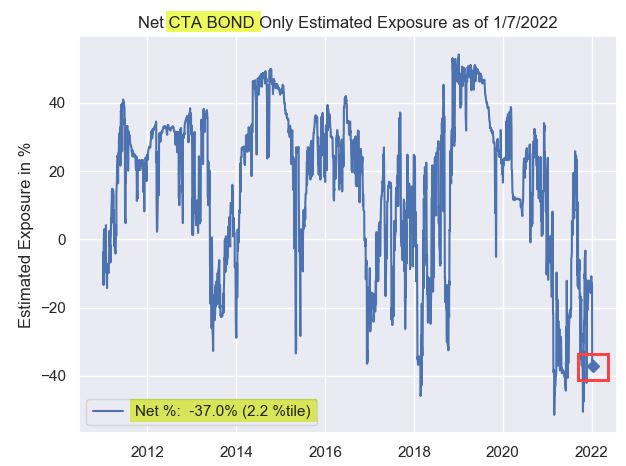

- Looking at the QIS CTA Trend model to get a sense of the “bearish momentum” and asymmetry within Fixed-Income positioning, we currently see the net exposure across G10 Bonds is back to 10 year historical “extreme Short” at just 2.2%ile overall exposure since 2011; further, the aggregate $notional position across the agg G10 Bond positions is now greater that -2 SD rank (i.e. very “net Short”) dating all the way back to 2002

Source: Nomura