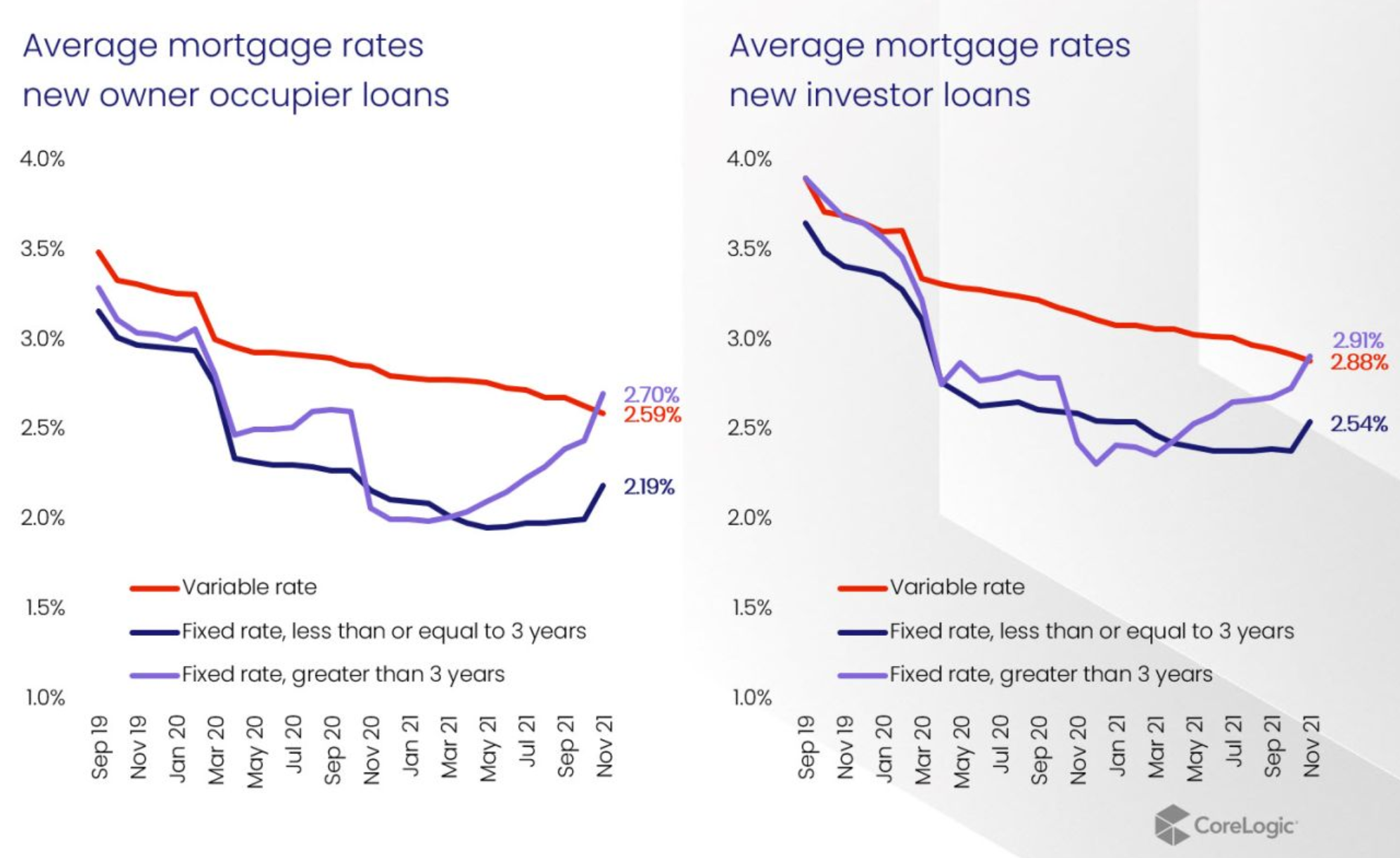

Fixed mortgage rates have risen sharply in Australia, as illustrated by new data from CoreLogic:

A year ago, owner-occupied homebuyers could find three year fixed rate mortgages on offer below 2%. But with the RBA tapering its quantitative easing program, average three-year fixed rates have now risen to 2.7%.

Smaller increases have also occurred for fixed rate mortgages below three years.

Advertisement