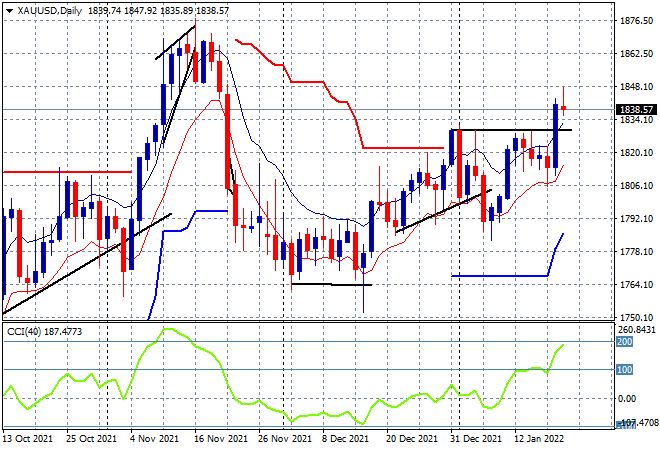

Wall Street stumbled going into the close as traders abandoned most of the confidence gained throughout the session with a big reversal that will wipe out any potential for a solid close for Asian stocks as the trading week ends. The USD also firmed against all the major currency pairs with moves in bond markets still expecting a surge in interest rate rises, even as the latest US initial jobless claims numbers came in higher than expected. Gold remains somewhat resilient to maintain itself above the $1830USD per ounce level while some heat came out of the oil markers with Brent and WTI both off slightly even as copper and iron ore prices continued to climb.

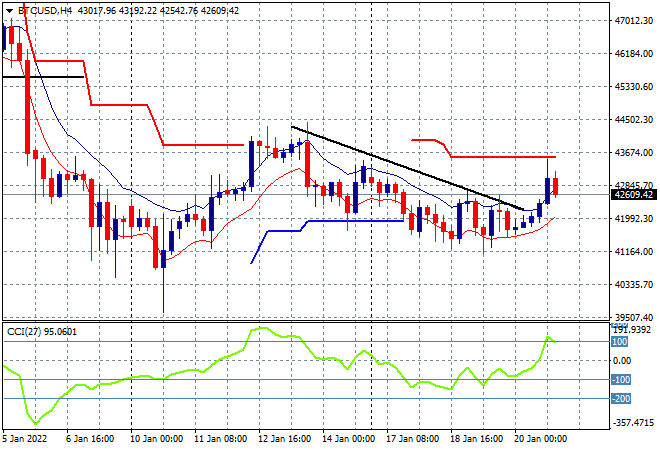

Bitcoin is having a minor breakout after being anchored at the $42K level all week with a small play up towards four hourly overhead resistance at the mid $43K level. This already looks done and dusted without a proper breakthrough as it failed to even get anywhere near the previous false breakout high from last week:

Looking at share markets in Asia from yesterday’s session, where mainland Chinese shares were largely unchanged with the Shanghai Composite sliding a handful of points to 3555 while the Hang Seng Index put in a big surge, lifting more than 3% higher to close at 24952 points. The previous breakout above the 24000 point level had been holding quite firm to provide this launch point as buying support developed here so we could be seeing a fill up towards the previous monthly highs near 26000 points next:

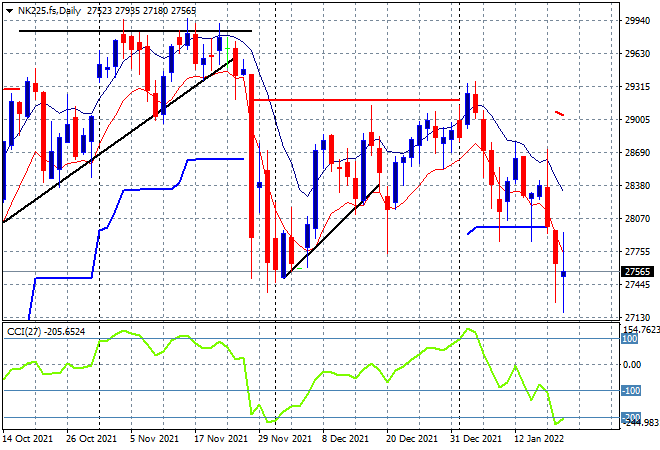

Japanese markets also bounced back from the previous steep drops with the Nikkei 225 closing 1.1% higher at 27772 points. Price action is likely to invert again however on the Wall Street selloff with activity contained here at short term resistance below the 29000 point level as safe haven Yen buying accelerated overnight. Watch for the November lows to be taken out next:

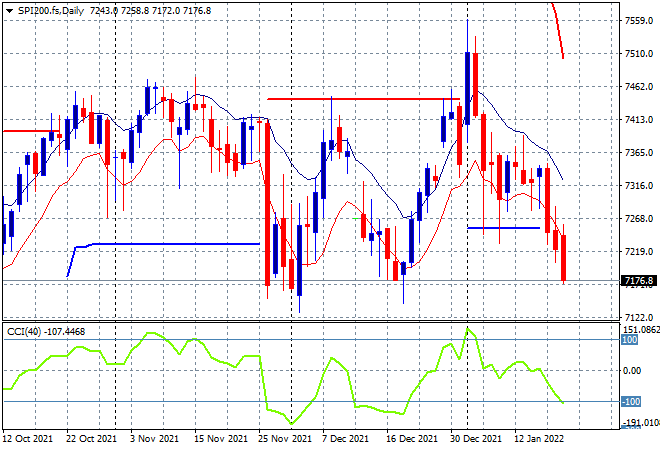

Australian stocks put in a very minor uplift with the ASX200 closing 0.1% higher to 7342 points. SPI futures are down more than 1% on the late slump on Wall Street, with support at the 7250 point zone likely to be taken out and the previous weekly lows tested as this sideways move since October last year leads to a lack of confidence:

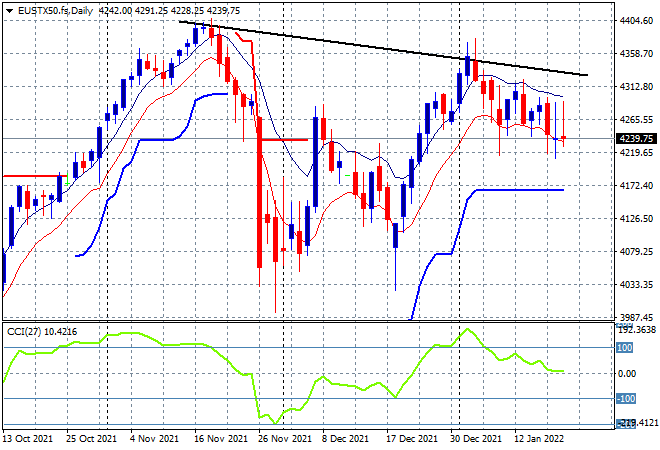

European shares were having a slightly better night with some modest gains across the continent as the German DAX and the Eurostoxx 50 index both finished up 0.5% or so, the latter finishing at just shy of short term support at the 4300 point level. However, post close futures which kept up with the Wall Street selloff are suggesting a rollover building, even as the weaker Euro fails to provide any help in stabilising price action at the 4200 point area where its ready to break:

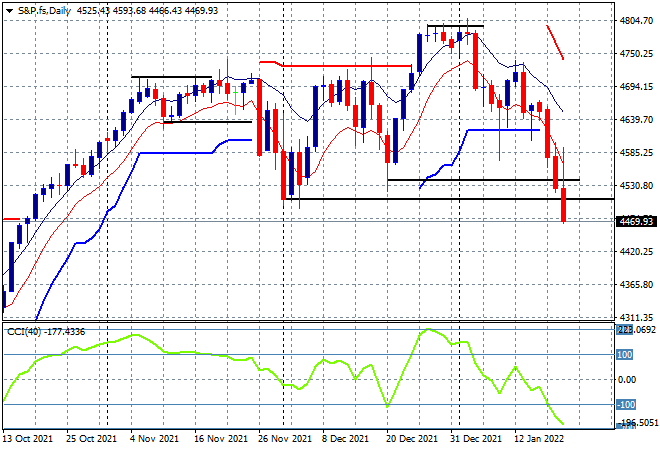

Wall Street was looking to forestall its current dip phase and was up more than 1% across the board at one stage but a late selloff screwed the pooch basically. The NASDAQ fell 1.3%, now off more than 12% from its highs while the S&P500 lost nearly the same to extend its falls below the 4500 point level, closing at 4482 points. This takes it back below the December lows, down more than 7% from its highs and ready to go lower as daily/weekly/monthly support is wiped out. And not even a single interest rate rise yet!

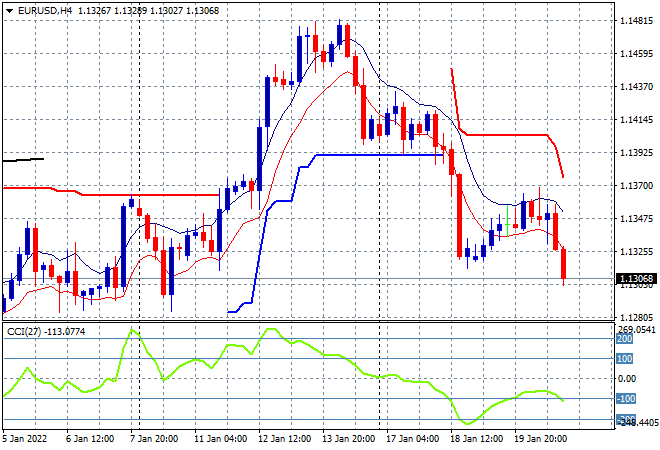

The release of the latest US initial jobless claims saw an unexpected uptick but it was more about a run to safety as USD firmed against everything on currency markets overnight, as volatility increased in the wake of the bond market selloff. Euro again sold off swiftly overnight, breaking back to the 1.13 handle to almost make a new weekly low with the next target at the 1.1280 level:

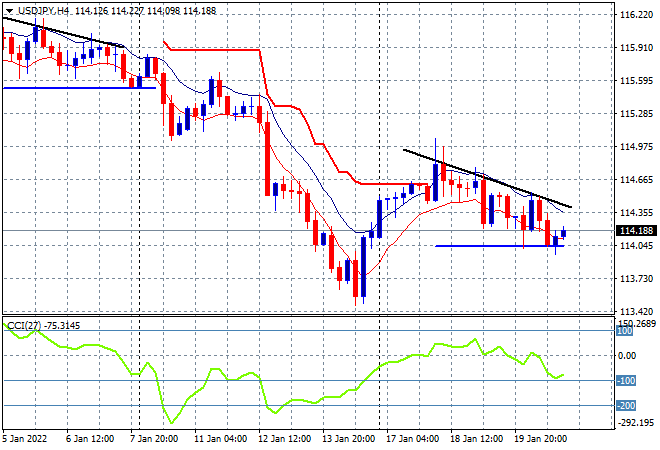

The USDJPY pair continues to stabilise somewhat here, with Yen safe haven buying offsetting the run to the USD. Price failed to clear overhead ATR resistance on the swing trade as activity starts to anchor itself to ATR support at the 114 handle instead. Momentum in the short term is switching to nearly oversold negative readings, so watch for a potential breakdown here if the risk off move accelerates:

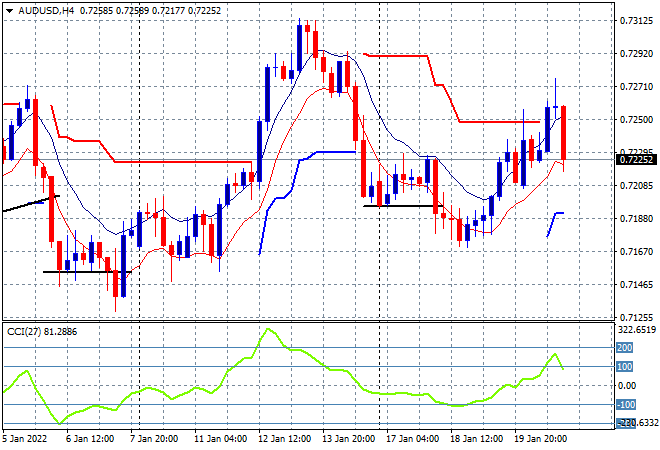

The Australian dollar was moving higher as its swing trade from the mid week slump continued through the 72 handle but this was swiftly knocked back into place later in the session, keeping price action well away from a new weekly high position. A nominally bearish engulfing candle on the four hourly chart does point to further downside here so watch the 72 handle to possibly break:

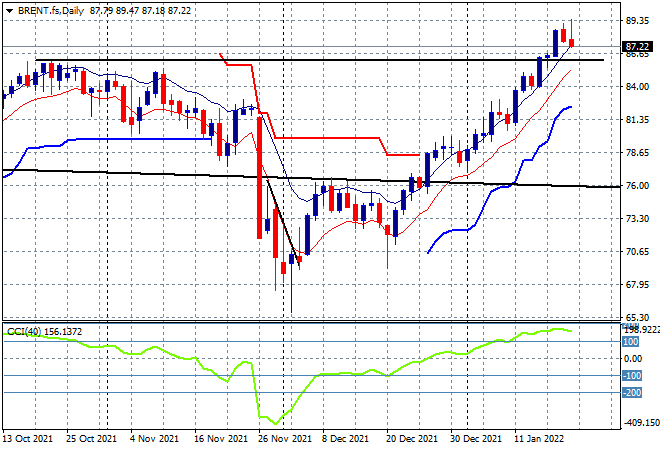

Oil markets are taking some heat out of their current big surge, with futures pulling back slightly as Brent markers retraced below the $88USD level overnight. Daily price action is suggesting a potential top (note the failure to make a new daily high, then an intrasession new high that was sold off to the close) but daily momentum remains well in overbought territory with price above the previous highs:

Gold is proving remarkably resilient here in the wake of bond market selloffs and runs to USD as it continues to push higher after clearing the key $1800USD per ounce level, finishing at the $1838 level overnight. The daily chart is looking more promising with the potential for a run up to the November highs gaining:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out!