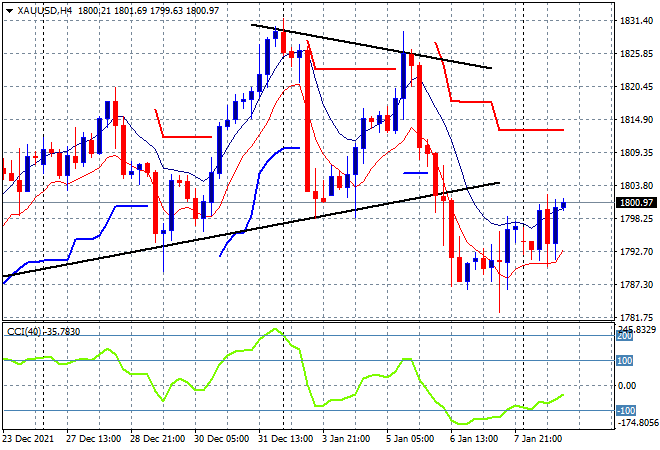

Wall Street was down over 2% overnight before a late bounceback saw it pare those losses as volatility across risk markets increases as the new year rolls on. The release of the latest US unemployment print last week continues to reverberate with 10 year Treasuries again up near the 1.8% level for new yearly highs as risk currencies oscillated against a volatile USD in an economic event free session. Gold climbed back to the key $1800USD per ounce level but no further while oil prices remained steady.

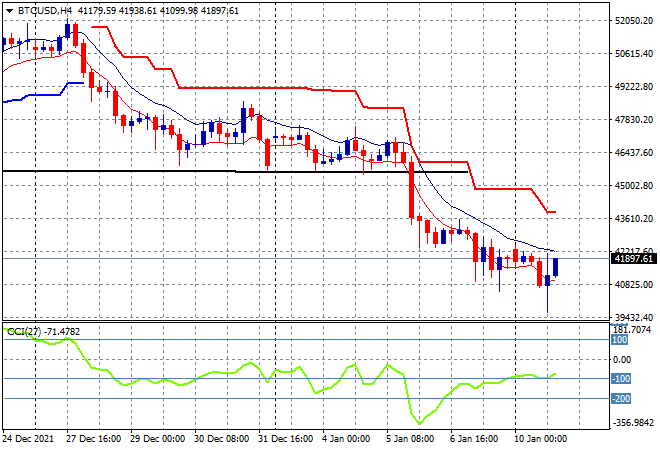

Bitcoin’s breakdown continued overnight with a small peekaboo below the $40K level before coming back to the start of week $42K level. There’s still daylight below to the next major support levels at $30K, with minor support at the September 2021 lows at $40K looking to firm up here given that late comeback in the session, but anything can happen next:

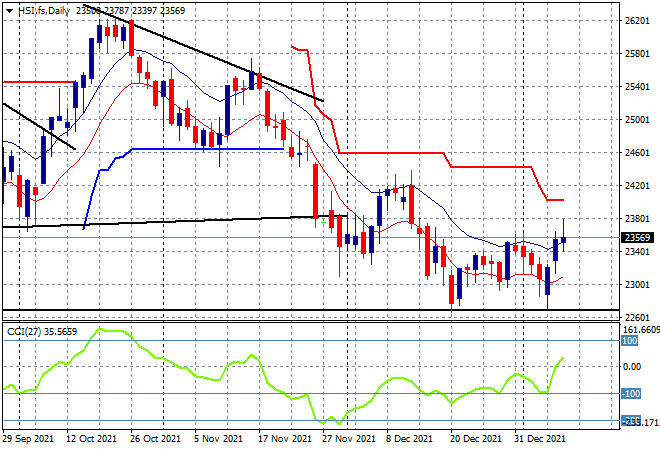

Looking at share markets in Asia from yesterday where mainland Chinese shares were relatively strong with the Shanghai Composite up 0.4% to 3593 points while the Hang Seng Index continued its bounceback, up 1% to remain well above the 23000 point level, closing at 23746 points. Price support is building at the 23000 point level where multi-month support lived previously, with a substantial break above the 24000 point level still required to get moving higher:

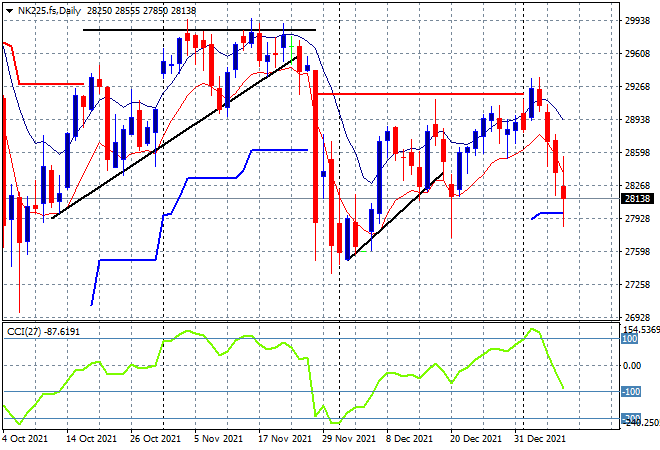

Japanese markets however were almost unchanged putting in scratch sessions with the Nikkei 225 closing 0.1% lower at 28478 points. Price action had tried to push through overhead resistance at the 29000 point level previously but the stronger Yen overnight plus volatility on Wall Street is broadcasting more falls as we head back to the December point of control at the 28000 point level:

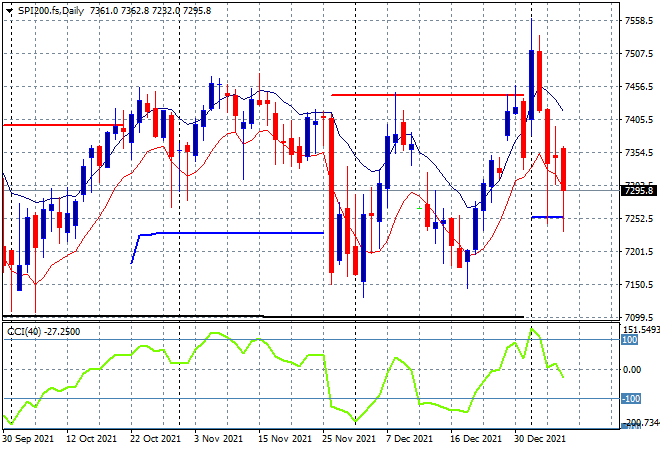

Australian stocks wavered throughout the session, with the ASX200 eventually closing a few points lower at the 7447 point level . SPI futures are showing at least a 0.4% loss to start the session with US stock volatility not helping at all here. The daily chart continues to look volatile with the previous false breakout above the 7500 point level possibly showing a return to previous weekly support at the 7100 point level if Wall Street doesn’t get moving soon:

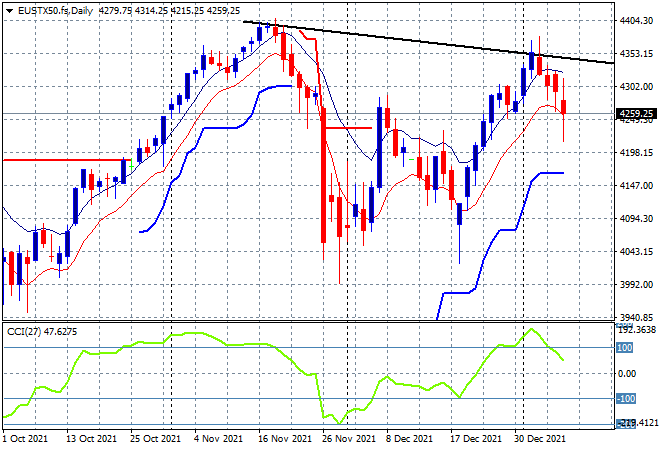

European shares had a wobbly start the trading week with losses across the continent, the German DAX closing 1% lower while the Eurostoxx 50 index finished 1.5% lower to break below the 4300 point level. The daily chart shows how this Santa rally could not pass the November highs with this rollover building, particularly with a stronger Euro that continues to dominate risk taking in the short term. Watch for any signs of breaking support at the 4200 point area next:

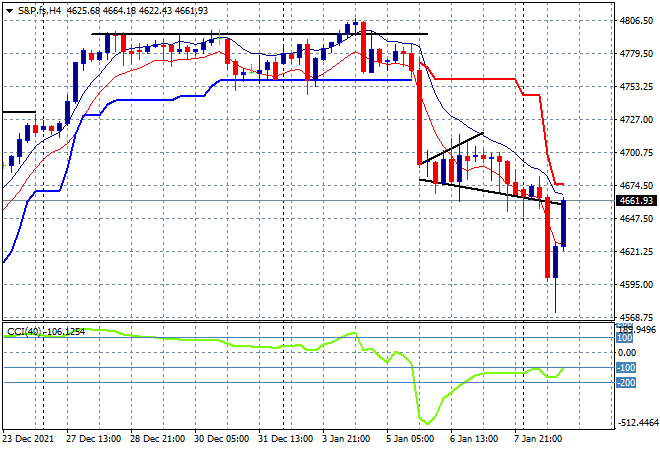

Wall Street fell sharply on the open with the NASDAQ off the most as its big hitters – Apple, Google etc – all fell out of bed – before a late recovery saw all three bourses barely put in scratch sessions. The S&P500 closed 6 points lower at 4670, still below the 4700 point level and unable to make a new session high since last week’s sudden pullback. The 4500 November lows are stil on the cards:

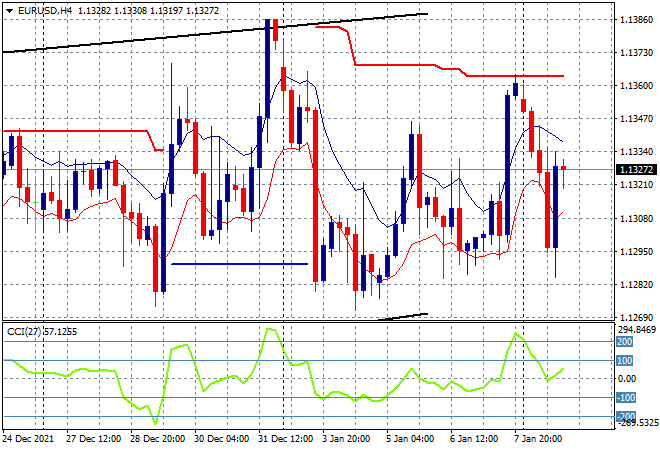

Currency markets were volatile and eventually directionless following Friday’s uncertain NFP print with the beleaguered Euro again bouncing back in line with Wall Street’s late surge to get back above the 1.13 handle. The four hourly and daily charts are starting to look very ugly indeed but there is a point of control in the middle here at the 1.13 level that should give an idea to actual direction soon:

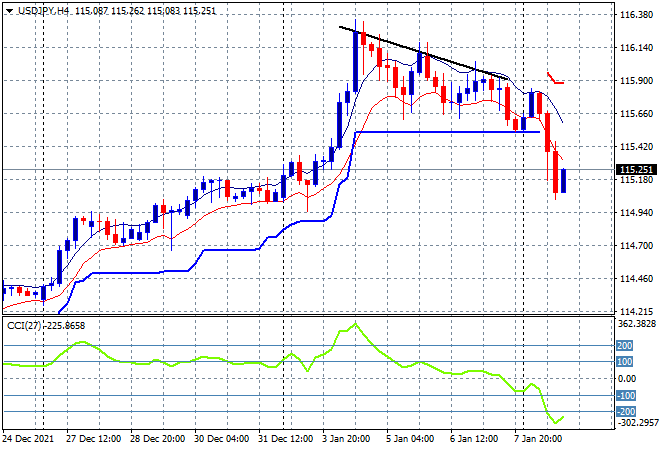

The USDJPY pair continued its very calm breakdown, after falling to trailing ATR four hourly support previously, it completely broke through the mid 115 level to almost make a new weekly low. This is a well overdone move going by momentum readings and a little bit of buying support on the last session so we could see a pause here at the 115 handle proper but its an ominous move for Asian stocks as Yen safe haven buying accelerates:

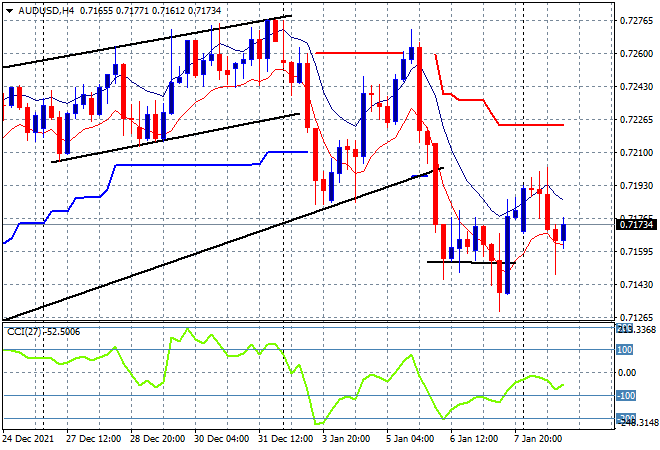

The Australian dollar remains under a lot of pressure which started even post NFP with its weak bounceback, with last night seeing another inversion as it remains at a three week low. Despite strong commodity prices, particularly iron ore, there’s not much support being provided here so I still contend we will see a move down to the 71 handle or lower:

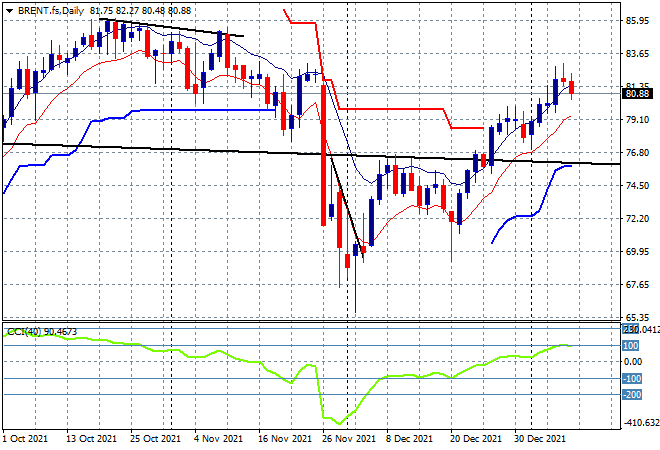

Oil prices are pulling back slightly despite the certainty around the OPEC+ decisions with Brent crude finishing down a little at just below the $81USD level overnight. After clearing its previous weekly highs the daily chart was showing a breakout building here, but the daily candles continue to show some hesitation to the upside that could be signs of resistance building at the $82-83 level as daily momentum is reluctant to move into overbought territory:

Gold is still struggling to get back on track as it scrapes back to the $1800USD per ounce level but no further overnight, with price action still below the recent uptrend line that broke post the hawkish Fed minutes. Price action is trying to overturn the clear signal of a return to the December 2021 lows, but will require a clear of overhead ATR resistance at $1810 at least to do so:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out!