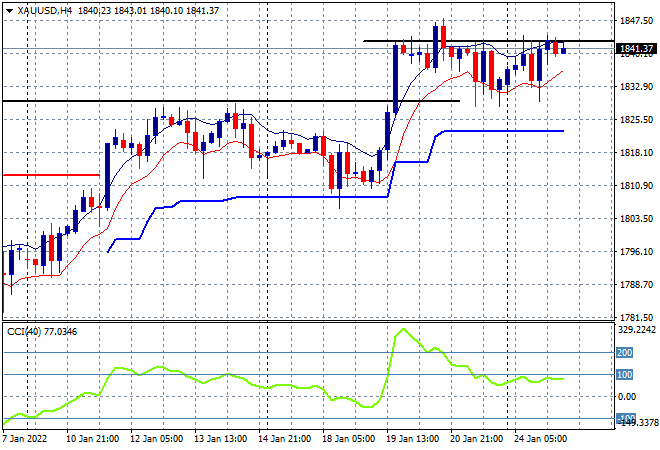

Asian stocks fell across the region in a heavy selling day, and while it didn’t replicate the overnight steep falls in Europe or the schizophrenic actions on Wall Street, its enough to get everyone very nervous as we head into tonights Federal REserve meeting. The latest (but late, and inaccurate) Australian CPI print was much higher than expected – quelle surprise – which gave the Aussie dollar a boost, but it may not be enough to get risk currencies moving as the USD remains very strong against most of the majors. Meanwhile, Bitcoin is up more than 10% from its lows, but still at the $36K level and ready to rollover while c gold holds on to its recent uncorrelated strength above the $1840USD per ounce level, setting up for a potential breakout during tonight’s Fed meet:

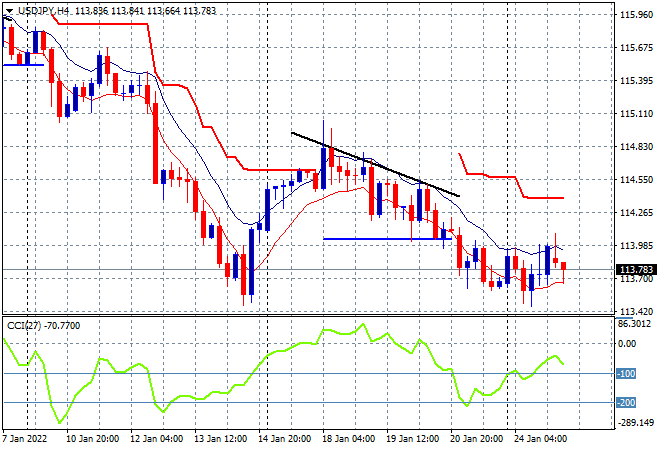

Mainland Chinese shares fell back with the Shanghai Composite down over 1.6% to 3466 points going into the close, while the Hang Seng Index did the same, currently down to 24274 points. Japanese markets all lost major ground with the Nikkei 225 closing 2% lower at 27051 points while the USDJPY pair was unable to translate its minor comeback overnight into anything substantial, still below the 114 handle and looking depressed:

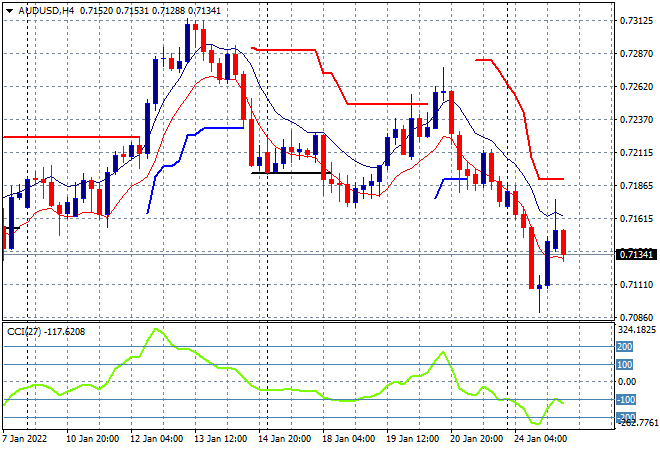

Not a good day for Australian stocks which caught up to the rest of the risk complex with the ASX200 closing 2.5% lower to crack below the 7000 point level and taking it back to the pre-COVID highs, as the Australian dollar is still remaining below the 72 handle despite the unexpectedly high inflation print, as the USD proves too strong:

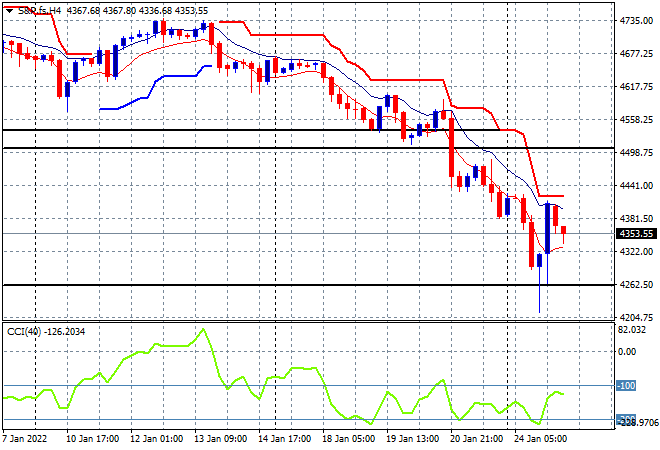

Eurostoxx and Wall Street futures are slowly turning over going into the London open, with the S&P500 four hourly chart showing a classic dead cat bounce after last night’s very steep crawl back up the stairs that lifted the market out of its dire position. The September 2021 lows at the 4250 level are the only support to look for here as four hourly trailing ATR resistance keeps this market in place:

The economic calendar includes the German IFO survey, US consumer confidence and then the start of the Fed meeting for January.