Goldman Sachs with the note:

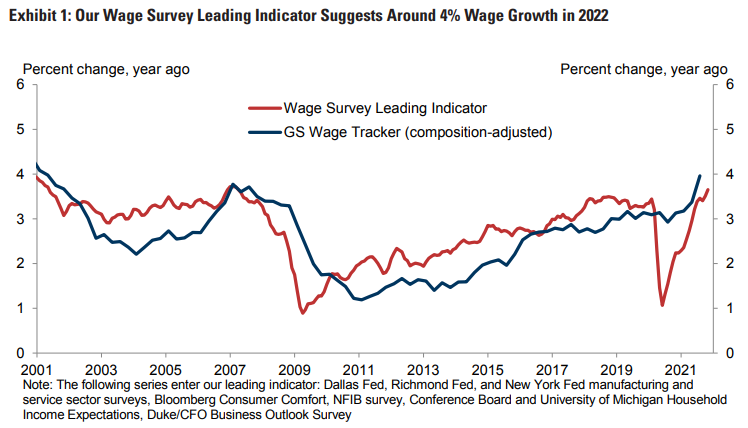

We expect that sequential wage growth will decelerate from its 5-6% pace in 2021 Q2 and Q3 to around 4% in 2022. An upside risk to this forecast is that if employers and workers expect wage growth to remain very firm, they might set wages and prices accordingly, leading to a persistent rise in wage and price inflation expectations. To evaluate this risk, in this US Daily we examine business and worker wage growth expectations for 2022.

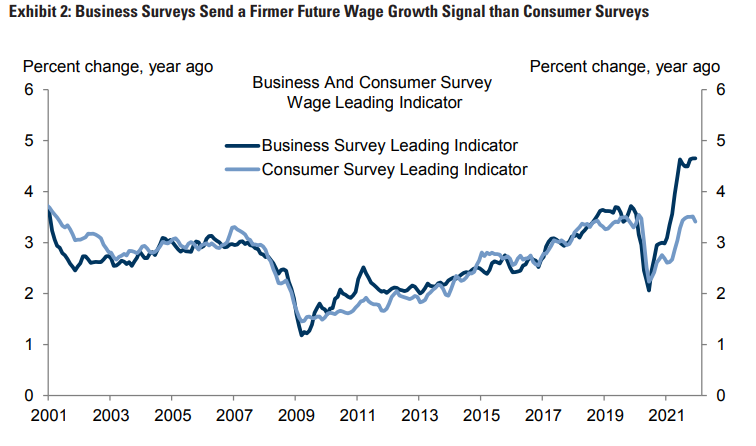

Our wage survey leading indicator—a composite measure of business and worker expectations about wage growth over the next year—is running just below 4%, but the pace implied by surveys of business expectations (+4.7%) is notably firmer than the pace implied by surveys of consumer expectations (+3.4%), possibly because a well-anticipated pullback in transfer income is confounding consumers’ responses.