Poor old Goldman, which forecast none of it, says now that the market correction is all a passing fad:

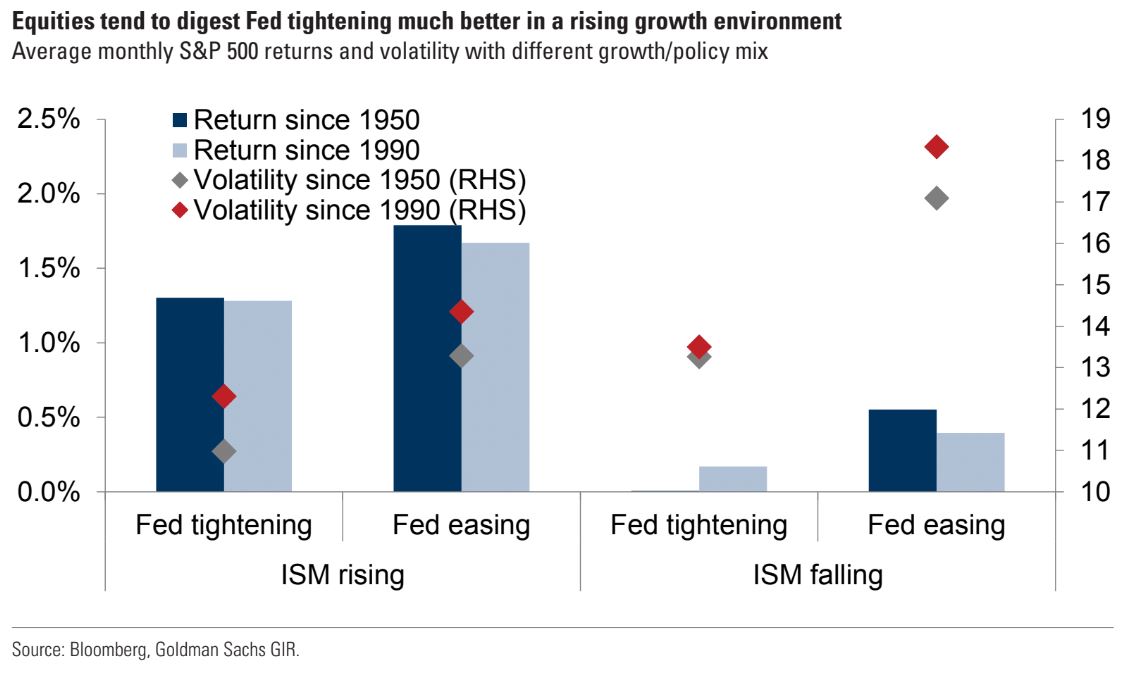

As markets continue to digest the outlook for the Fed, rates, and growth, we believe that the recent equity drawdown will prove to be a correction in a longer bull market cycle, rather than the start of a new bear market, and see remaining downside risk as limited so long as economies continue to grow. While the prospect of higher rates has weighed on equities, we think the crucial determinant for returns will be what happens to growth as rates begin to rise. As our chart of the week shows, equities tend to digest Fed tightening much better in an environment of rising growth, and we expect a modest improvement in activity in 2Q and 3Q even if rates are starting to rise. Despite our expectation that terminal rates will peak at around 2.75% (still around 100bp above market pricing), this would still be very low relative to history and unlikely to generate a recession, in our view, absent which equities are likely to make progress this year. With this in mind, we think any further significant weakness at the index level should be seen as a buying opportunity, albeit with more moderate upside given the starting point of this cycle is one of record low interest rates, high valuations, and high margins. We also believe that the rotation into Value has further room to run given that the transition from a world of QE to QT, and from risks of inflation to risks of deflation, should support further re-rating of selected value assets. That said, from a tactical perspective, equity investor length still remains elevated relative to history, and we think a near-term catalyst, such as a slowdown in inflation or extremely strong earnings, may be needed before investors re-risk.

Beyond equities, we think the strategic case for holding commodities in a diversified portfolio have rarely been as strong as it is today. Indeed, we expect the combination of depleted inventories across major cyclical commodities, elevated inflation, relatively robust global GDP, and a modestly lower USD will fuel a virtuous commodity cycle in 2022. We also recommend positioning for further upside in Gold, which we consider a defensive inflation hedge, and recently raised our 12m price target to $2,150/toz.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.