By Gareth Aird, head of Australian economics at CBA:

Key Points:

- We expect the headline CPI to increase by 1.1% in Q4 21 (3.2%/yr).

- The trimmed mean CPI on our forecasts will print at +0.9% (2.5%/yr).

- An underlying inflation outcome in line with our forecast would be a big upside surprise compared to the RBA’s central scenario for the inflation outlook.

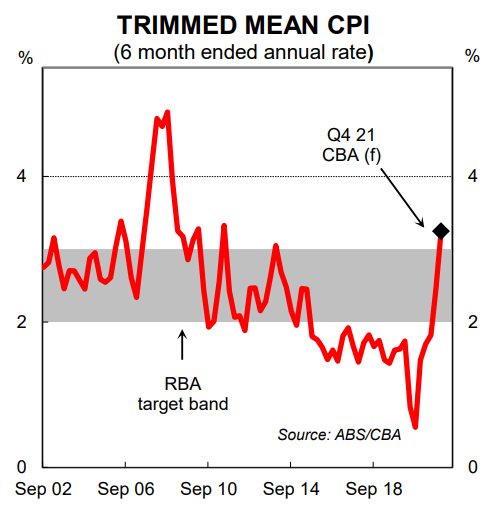

- It is our expectation that the upcoming CPI will be the smoking gun that sees the RBA end the bond buying program at the February Board meeting. It should also lay the groundwork for a rate hike in late 2022.

Overview

The Australian economy is currently being significantly disrupted by an explosion in COVID cases. More specifically, illness related to the virus and isolation requirements are having a large negative impact on both the demand and supply sides of the economy. In addition, concerns around catching the virus given the high number of new daily cases may also be weighing on the demand for some services.

But this challenging period is expected to be short lived and the economy should do very well on the other side. As such, the upcoming Q4 21 CPI, due 25 January, is an incredibly important data release for the monetary policy outlook. Indeed it could turn out to be pivotal for financial markets and the RBA’s narrative around the inflation outlook.

The RBA has been steadfast in their messaging on inflation over the pandemic. They have consistently argued that inflation pressures would only emerge gradually and modestly. The central bank have made some upward revisions to their central scenario for the inflation outlook along the way. But these forecast changes have generally just been a mark-to-market exercise (i.e. they have simply incorporated the stronger than expected actual inflation data into their forecast profile without making any substantive changes to their views around the inflation outlook).

Regular readers will know that we disagree with the RBA on the inflation outlook. We expect both inflation and wages pressures to emerge sooner and stronger than the RBA anticipates. Our forecast profile for an acceleration in inflation and wages over the year as we achieve full employment underpins our call that the RBA will commence normalising the cash rate in late 2022. It is our expectation that next week’s Q4 21 CPI will be a strong set of numbers.

A recap of the Q3 21 trimmed mean CPI and RBA response. The Q3 21 CPI, which printed on 27 October 2021, was a very big event for financial markets. The RBA’s preferred trimmed mean measure rose by 0.7%/qtr in Q3 21 which pushed the annual rate up to 2.1%. It was a solid upside surprise relative to the RBA’s inflation forecasts. At the time, the RBA had forecast the trimmed mean to be 1¾%/yr at Q4 21 which implied quarterly growth rates of 0.4-0.5% over the September and December quarters.

Money markets sold off aggressively and immediately on the Q3 21 inflation data. And over subsequent days a disorderly selloff continued in large part because the RBA did not defend their yield curve target which marked the implicit end of yield curve control (recall that at the October 2021 Board meeting the RBA reaffirmed the target of 0.1% on the April 24 Australian Government bond). At the November Board meeting following the Q3 21 CPI the RBA formally announced it would discontinue with the yield curve target.

The Q3 21 CPI highlighted the importance of the inflation data for the RBA’s policy decisions. Indeed the Q3 21 CPI was the data release that effectively saw the RBA walk away from their yield curve control policy in between Board meetings – a decision that generated a lot of dysfunction in markets.

What to expect in the Q4 21 CPI

We expect there to be evidence of both demand pull and cost push inflation in the upcoming CPI. Input costs have risen in part due to supply side bottlenecks, while strong demand will have enabled firms to lift their prices at the consumer level.

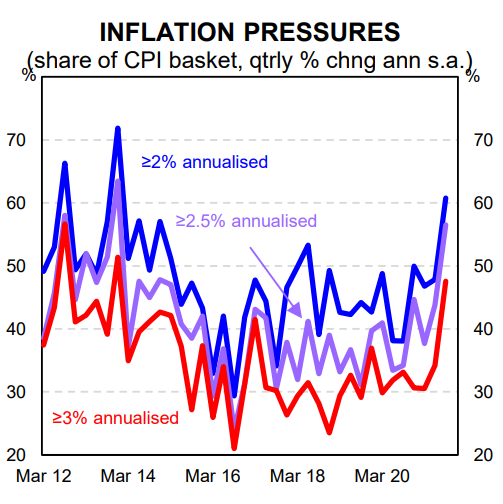

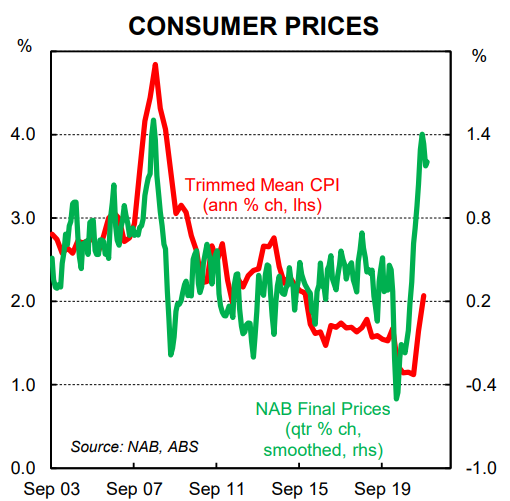

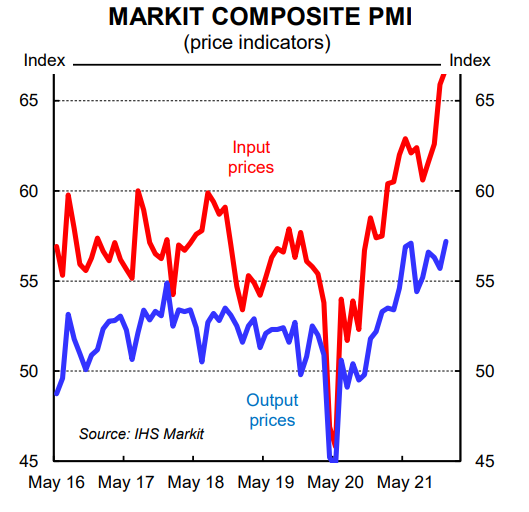

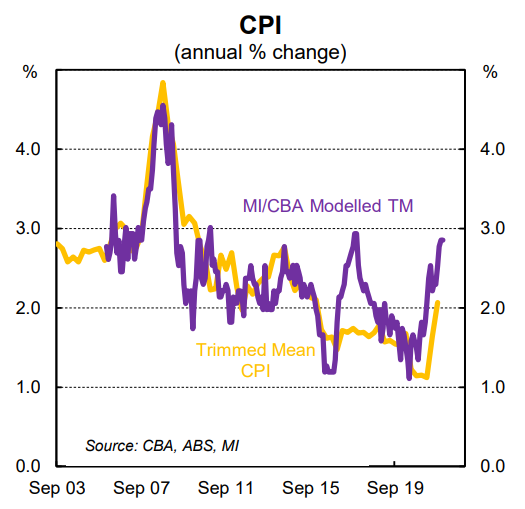

Private surveys like the NAB business survey and the Markit PMIs support our view that the rate of inflation accelerated over Q4 21 (see charts opposite). A lift in the inflationary pulse would also be consistent with our client discussions, particularly our corporates. In our view something would be amiss if we did not see inflation accelerate in the official data over the December quarter.

Our forecast is for the headline CPI to increase by 1.1% in Q4 21 which would see the annual rate edge higher to 3.2% (from 3.0%).

The more policy relevant trimmed mean on our figuring will rise by 0.9%/qtr. This would push the annual rate up to 2.5% (the mid-point of the RBA’s 2-3% target range). The six month annualised rate, which better captures the inflationary pulse, is forecast to step up to 3.2%.

The detail

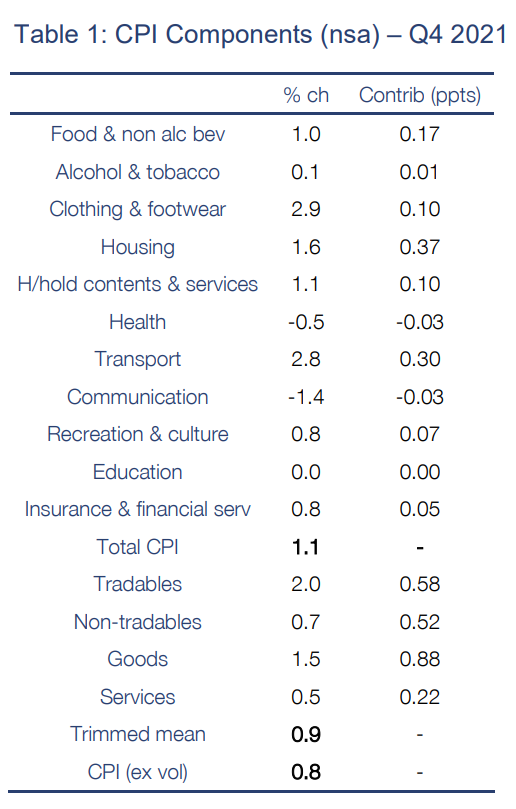

See Table 1 opposite for our detailed forecasts for the Q4 21 CPI basket.

The main features of our call are as follows:

- a decent rise in food prices of 1.0% following a modest 0.3% lift in Q3 21 (the risk lies with a stronger number);

- a solid 2.8% increase in transport primarily driven by a 7.4% increase in petrol prices;

- a large 2.9% lift in clothing prices following the lockdown induced 3.8% fall over Q3 21;

- a seasonally weak outcome for alcohol and tobacco prices given the expiration of the tobacco excise;

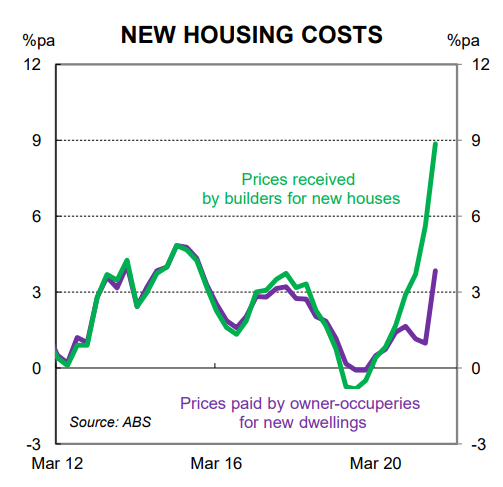

- a solid 1.6% increase in housing as the impact of the HomeBuilder grant fades which will put substantial upward pressure on the measured price of building a home (see chart on following page);

- a flat outcome for education prices reflecting the usual seasonal pattern;

- a small fall in in health prices due to a seasonal decline in pharmaceutical prices; and

- a decent 0.8% increase in recreation prices due to a big lift in domestic holiday and accommodation prices.

Inflation and the RBA

The RBA has forecast the trimmed mean to be 2¼%/yr at Q4 21 which implies a quarterly growth rate of ~0.6% over the December quarter. As such, if the trimmed mean CPI prints in line with our call it would be a big upside surprise relative to their forecast. Such an outcome we believe will see the RBA shift their narrative around the inflation outlook. It would also likely see the Board drop their forward guidance on the cash rate (albeit the RBA has more recently toned down their forward guidance).

In the RBA’s most recent communication, the December 2021 Board Minutes, inflation was described as being “low in underlying terms”. And on the outlook, “a further, but only gradual, pick-up in underlying inflation was expected. The central forecast was for underlying inflation to reach 2½ per cent over 2023.”

It would simply not be credible to continue with the current characterisation of inflation as “low in underlying terms” if our forecast proves correct. And the inflation outlook would need to shift gear if the 6 month annualised rate has accelerated to 3.2% (as per our forecast).

Of course, we may be wrong and economics is a humbling profession. If the underlying CPI prints in line with the RBA’s forecast they will persist with their current view on inflation and they will be unlikely to make any changes to their forecast profile for core inflation in the February 2022 Statement on Monetary Policy (SMP). Market pricing for RBA rate hikes would need to be pushed out if the trimmed mean Q4 CPI prints in line with the RBA’s forecast profile.

Overall our expectation is that the Q4 21 CPI will be sufficiently strong to see the RBA announce the cessation of the bond buying program at the February 2022 Board meeting. And we believe it will lay the groundwork for a rate hike in late 2022.