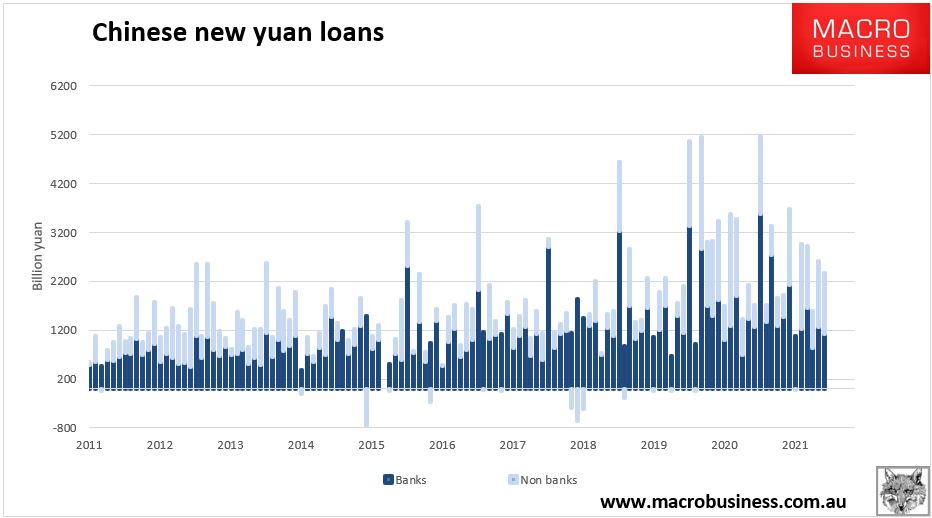

Chinese credit was out overnight and enjoyed a soggy bounce with TSF up 2.37tr yuan and banks 1.13tr:

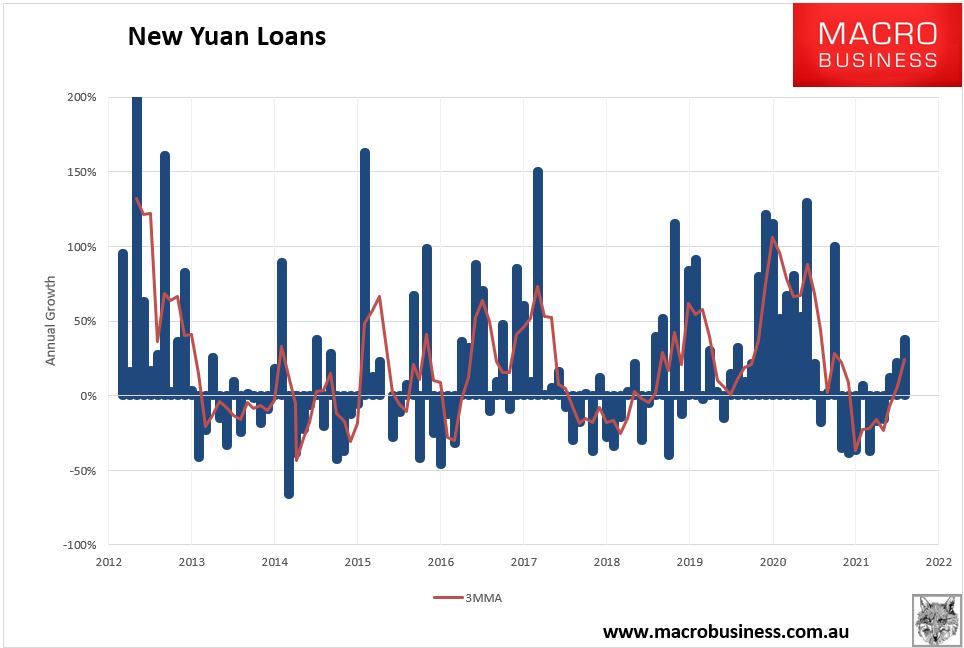

The flow of loans was up 34% year on year:

Advertisement

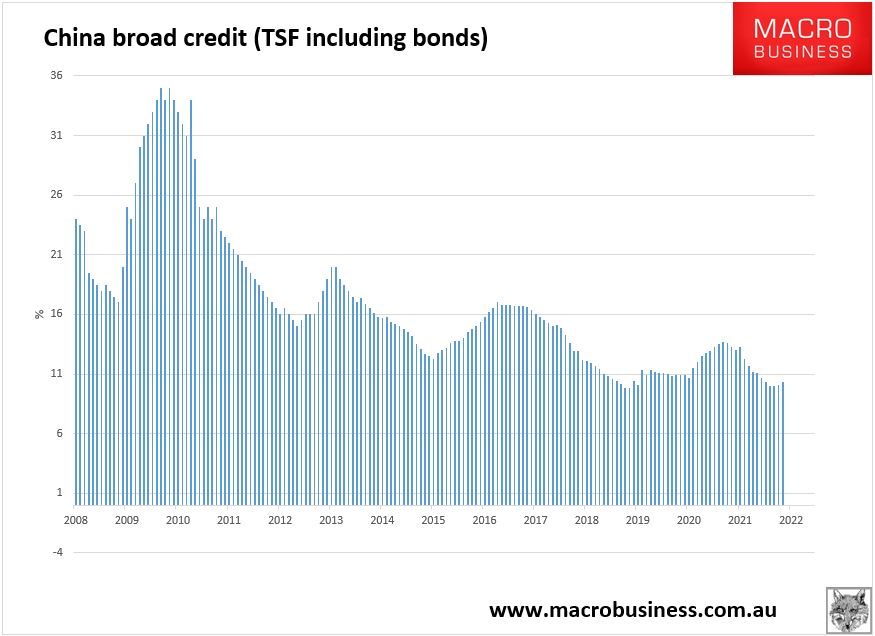

The stock of loans was up a little to 10.3%

Chinese credit was out overnight and enjoyed a soggy bounce with TSF up 2.37tr yuan and banks 1.13tr:

The flow of loans was up 34% year on year:

The stock of loans was up a little to 10.3%

The full text of this article is available to MacroBusiness subscribers