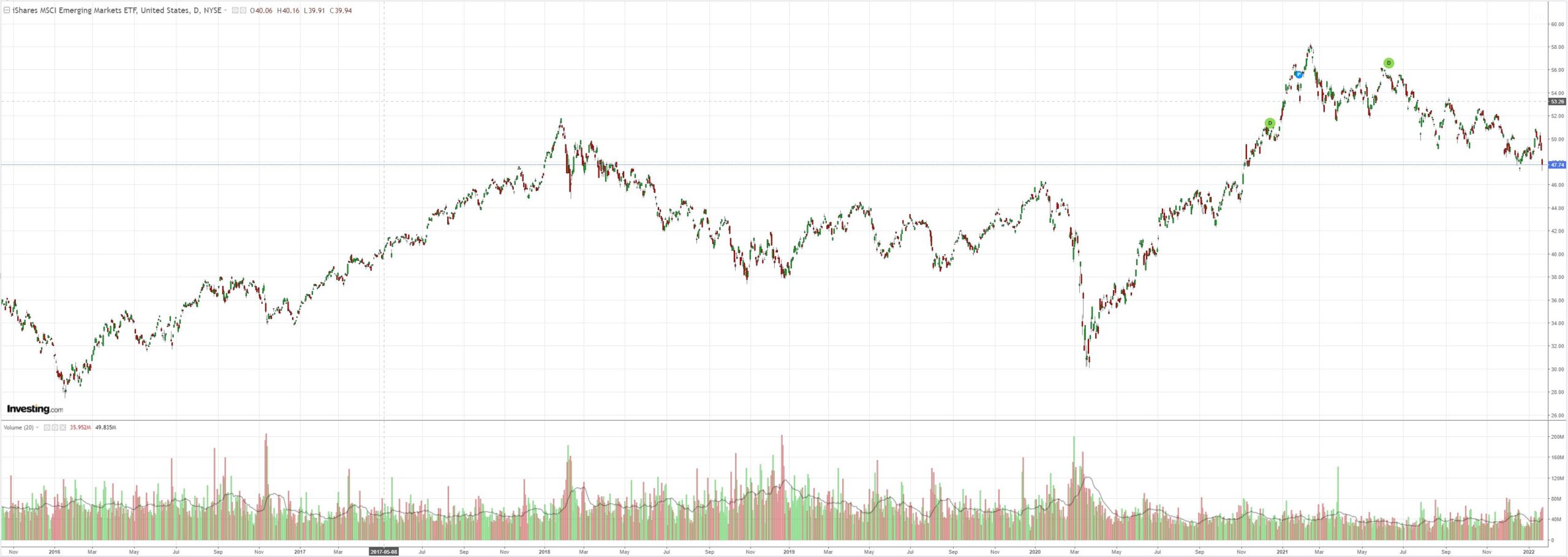

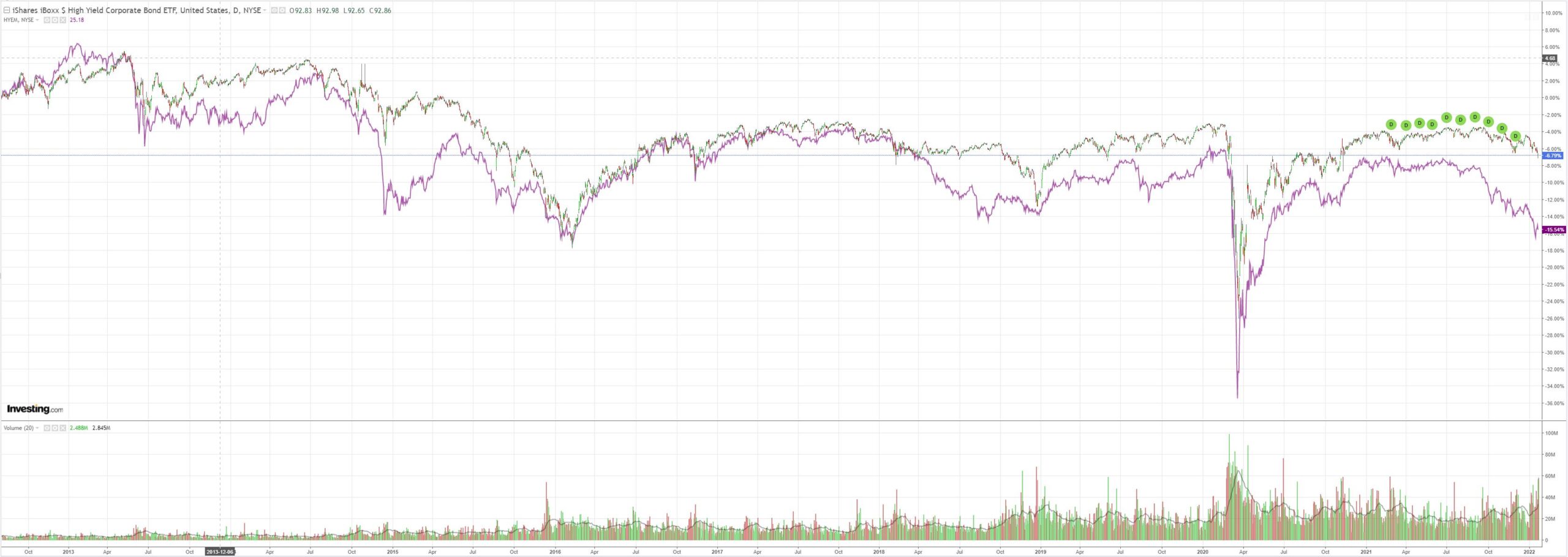

EM junk rolled over. A little stress appeared in US high yield but there is no need for any Fed pivot yet:

Advertisement

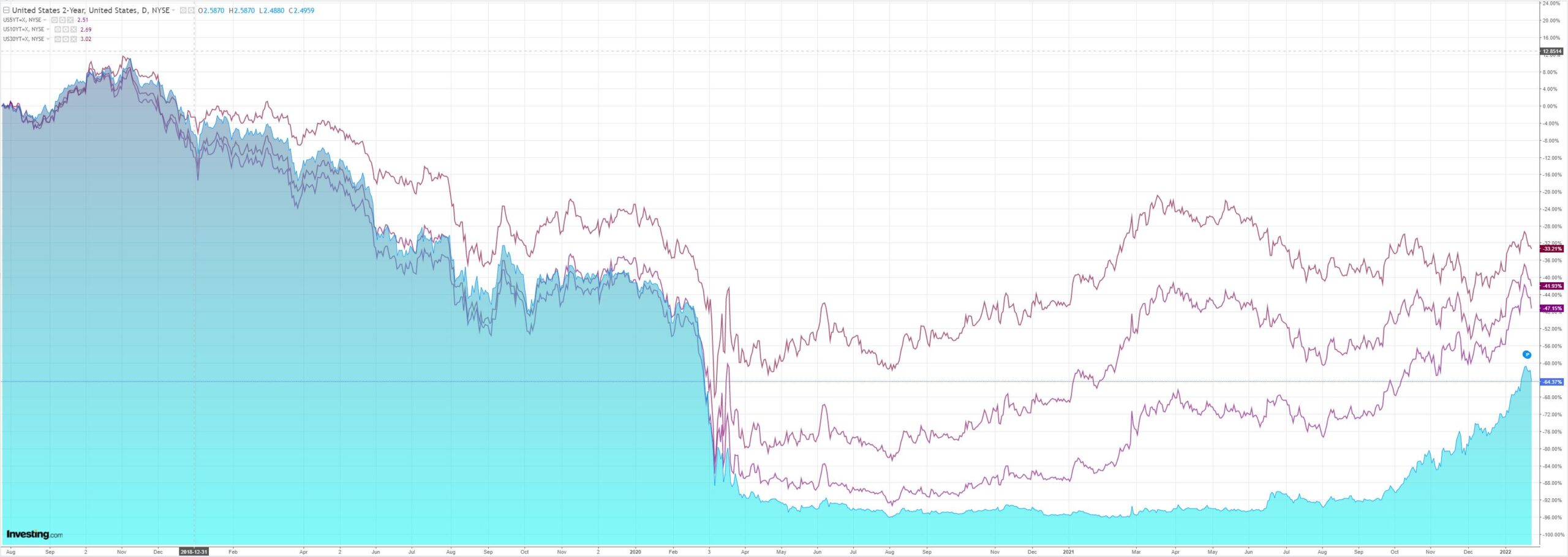

Treasury yields fell:

Which made the stock crash a little less worse:

Advertisement

Westpac has the wrap:

Event Wrap

US Markit PMIs disappointed, with a sharp fall in services to 50.9 from 57.6. and a fall in manufacturing to 55.0 from 57.7. Markit cited a sharp drop in activity due to output being impaired by Omicron-related staff shortages and increased supply disruptions, but also referred to solid demand and encouraging prospects for the near-term outlook as Omicron effects wane. The Chicago Fed National Activity Index for December declined to -0.15 (sub-zero indicates below trend growth) from a revised Nov. reading of 0.44 (initially +0.37).

Eurozone Markit Flash PMIs were close to expectations. Manufacturing PMI was solid at 59.0 (est. 57.5), while services were affected by Omicron, at 51.2 (est. 52.0). Market cited the dent to activity, notably in services, being less severe than in other Covid waves and that the outlook was more positive. However, pricing prospects suggest little easing of inflationary pressures.

The US ordered families of its diplomats in the Ukraine to leave the country amid growing speculation about a Russian incursion. The UK also said it would also withdraw some staff and families.

Event Outlook

Aust: Q4 CPI will be published. In terms of key drivers, dwelling purchase prices, auto fuel and food will play an important role, and holiday travel will also contribute. There is an upside risk to dwellings as Homebuilder grants expire and cost pressures lift. Uncertainty around durable goods remains. Westpac forecasts a 1.1% q/q and 3.2% y/y rise for the headline CPI (market median is 1.0% and 3.2%). The offsetting soft components in Q4 are seasonal, thereby supporting a solid 0.7% (2.4%yr) gain in the trimmed mean measure. Meanwhile, the December NAB business survey will highlight the impact of omicron on confidence and activity.

NZ: The December BusinessNZ PSI may see a small bounce as restrictions in Auckland eased.

Ger: The IFO business climate survey is expected weaken further in January as a consequence of omicron (market f/c: 94.5).

US: Growth in the FHFA house price index and S&P/CS home price index should remain robust in November, reflecting the continued strength in home demand (market f/c: 1.1% and 0.97% respectively).

What an idiot is the equity market these days. We haven’t even had a Fed hike and here it is on its knees begging for MOAR already. In my view, it has a lot more begging to do yet.

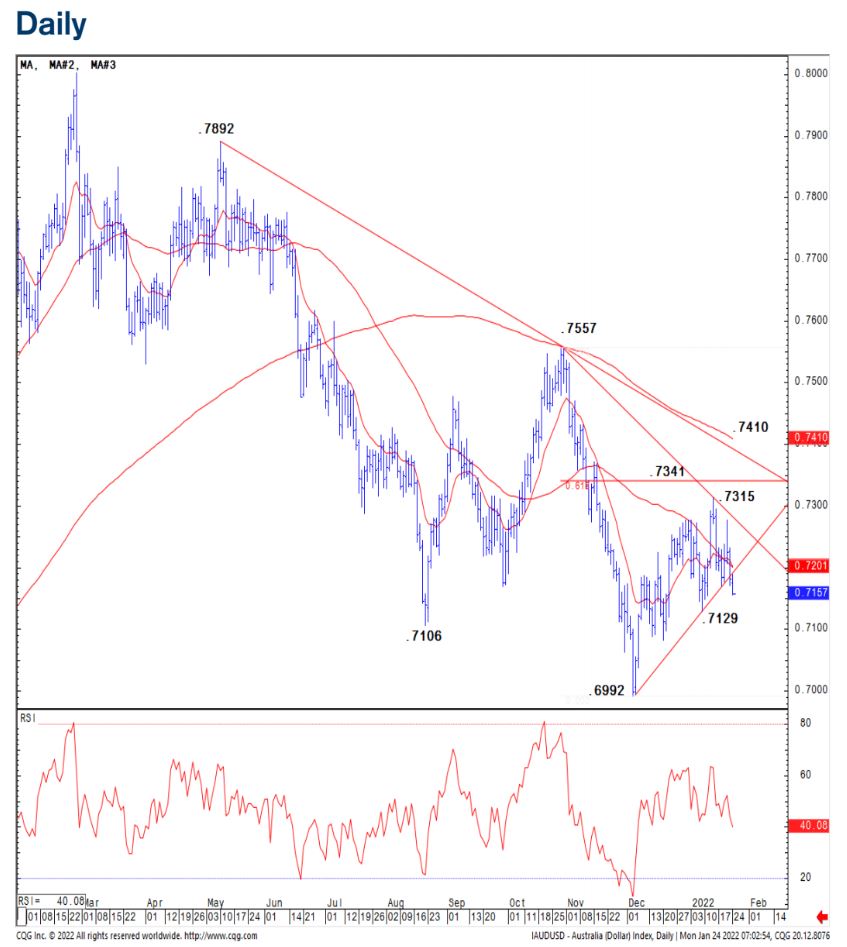

That is now the core driver of the AUD. The risk asset correction has further to run and so, therefore, does AUD selling. Credit Suisse offers some technical targets that are as good as any:

Advertisement

Below .7129 should confirm a resumption of the core downtrend AUDUSD has extended its rejection of its downtrend from last October for a break of its shorter-term uptrend from December to suggest the corrective recovery is over and broader downtrend is resuming. Key now is the January YTD low at .7129, removal of which should reinforce our view to add momentum to the decline for a move back to .7089/82 and eventually a retest of medium-term support at .6992/91 – the late 2020 and 2021 lows. Below here should then open up an eventual move to the 50% retracement of the entire 2020/2021 uptrend at .6758, which remains our core medium-term objective.

Short-term resistance moves to .7170 with resistance at .7216/33 ideally now capping to keep the immediate risk lower. A break can clear the way for a move back to the high of last week and downtrend at .7277/84, but with fresh sellers expected here.

Below .7129 should reassert the core downtrend for support seen at .6994/91.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.