DXY continued to swoon last night as it shakes out the longs:

That was enough to lift the Australian dollar despite falling markets though not so much versus crosses:

Dirt remained bid:

Miners were softer:

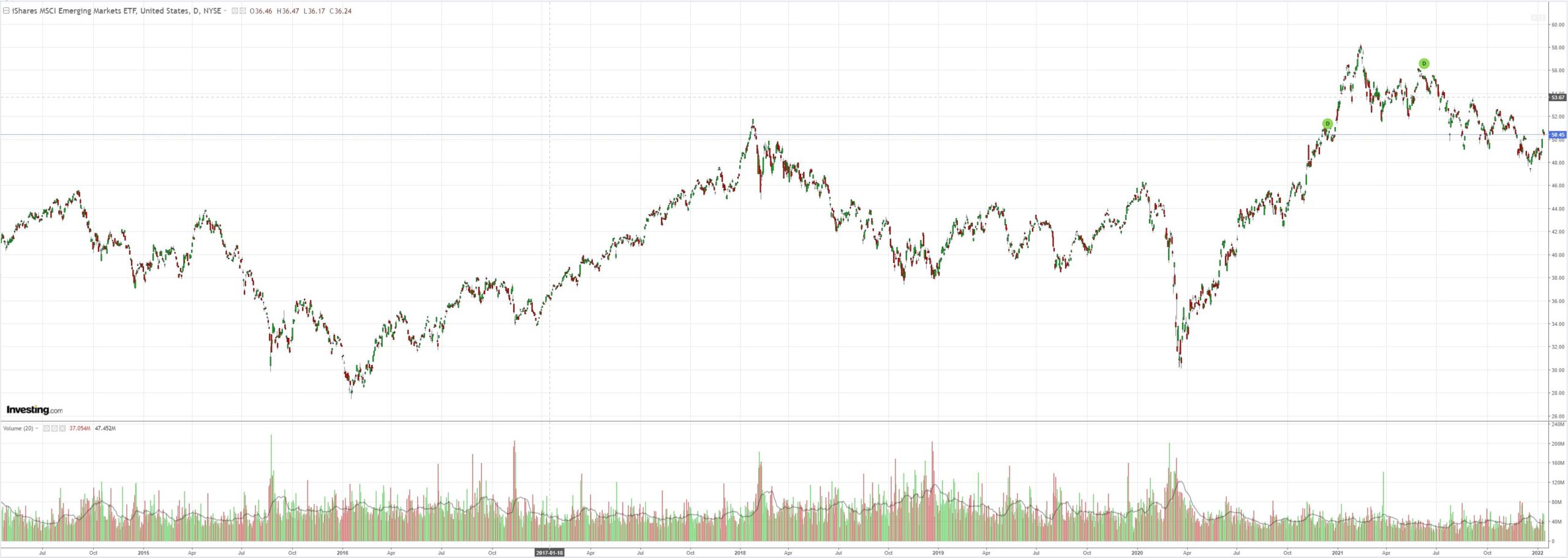

EM stocks flamed out:

As EM junk sends a crystal clear warnig that all is not well. The divergence from DM is unprecedented and no relief from a falling DXY alarming. Money is being sucked from risk assets on the periphery. That does not end usually until it makes its way back to the core:

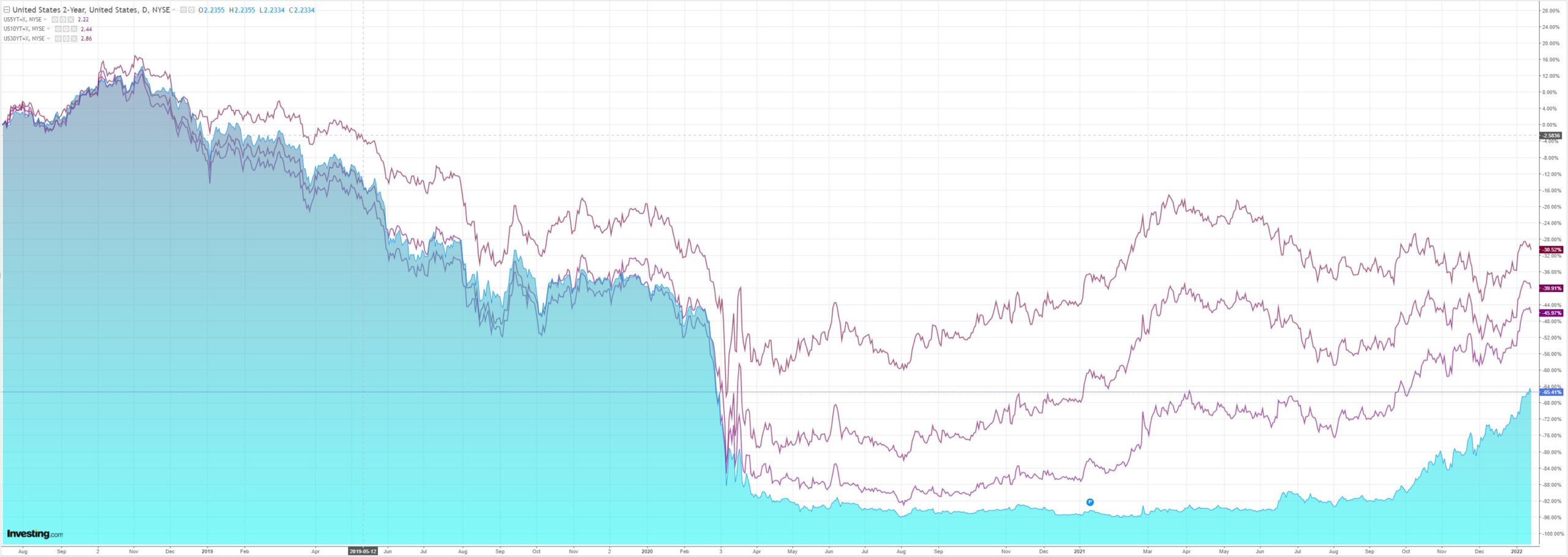

US yields fell:

And so did stocks:

I would characterise this as a slow breakdown of the bull market as the Fed tightens. Markets are still bidding commodities and the AUD on OMICRON disruption, US inflation and Chinese stimmies. But for how long as the Fed withdraws liquidity, Chinese property gets worse and it forced to ouotright slash rates, sinking the yuan and bringing crisis to the entire EM debt complex.

Credit Agricole sums the chaos nicely:

Asia overnight

Investors appear stunned at the moment. US inflation came out in line with market expectations and led to little further moves in market pricing for the Fed and UST yields. Indeed, even further hawkish speak from FOMC members did not really move rates markets. The USD did move, however, as investors exited long positions, which saw a collapse in the currency during North American trading. In the Asian session, investors seem to be waiting for the next impetus. Eyes are on China, where there are newswire reports that Chinese authorities have told local banks to restrict property loans to local governments. A majority of Asian bourses and S&P500 futures were trading lower at the time of writing. G10 FX remained stunned in the wake of the USD’s collapse and was range-bound during the Asian session.

AUD: help wanted

Data released this week showed that even before the omicron outbreak in Australia, employers were trying to fill 400k vacancies. These vacancies are mainly in the healthcare, accommodation and food services, administration, professional and scientific services and manufacturing industries. Omicron has made things worse for employers as some staff are reluctant to work for fear of infection and self-isolation rules for close contacts leading to staff absences. These absences are extended by a lack of rapid antigen tests that could clear staff to work. The Federal and state governments are looking at ways to address these issues, some states such as Victoria are loosening the rules on close contact and isolation. The Federal government has doubled the hours foreign students are allowed to work and is considering increasing the hours pensioners can work before having their welfare payments cut. The RBA will be paying close attention to next week’s labour market data release for December and CPI data the week after, where supply chain issues have seen retail prices head higher. Expectations in the market around this data are heating up.

USD/JPY great expectations

It is clear from the reaction in the USD following the US CPI number that the market had great expectations heading into the data release. Our proprietary positioning index showed long USD was the largest position in the G10, albeit in line with its 2M average. So, despite headline inflation meeting expectations, core inflation surprising slightly to the upside and the components of the CPI such as shelter pointing to persistent underlying inflation pressures in the US economy, the USD collapsed after the data release. This collapse was even in the face of UST yields holding steady and the Fed’s James Bullard (admittedly a hawk) calling for four rate hikes in 2022. The wash out in positioning is likely good news for the USD/JPY in the medium term. We continue to think the hawkish Fed willing to fight inflation will push the exchange rate higher and to 116 again by end Q1. The most important factors on this front will not only be the pace of the Fed’s rate hikes, but also its balance sheet run down. Our stop in USD/JPY was triggered during the USD rout and we have exited our long USD/JPY trade for a 1.0% profit. We will look to reenter a long USD/JPY trade again in the coming months.

USD: dazed and confused

The new year is not even two weeks old and we are already seeing the almost complete reversal of the FX moves from the start of the year. It has been a rollercoaster ride for the USD, which is more puzzling given that it is taking place against the backdrop of elevated UST yields and market expectations of a Fed rate hike already in March. The most straightforward explanation for the price action is that the USD is extremely overbought across the board at present and that FX investors are looking for fresh incentives to go long. In addition, for all the hawkish Fed rhetoric and the positive US inflation surprises of late, rates markets remain sceptical that the FOMC will be able to deliver on its longer-term tightening plans reflected in its December ‘dot plot’. As a result, with markets front-loading rate hikes from other G10 central banks as well, the USD’s rate appeal did not receive the boost it would have if the global tightening cycle were less homogenous. Finally, the market’s fears that the pandemic and the Fed tightening will spell out the end of the risk rally have started abating and this has hurt the safe-haven USD. On the day, FX investors will focus on speeches by Fed’s Charles Evans and Tom Barkin as well as the confirmation hearing of Fed vice-chair Lael Brainard at the US Senate. That said, the overbought USD could remain vulnerable to further profit taking on long market positions.

I still think there’s another DXY leg up and AUD leg down as it all ends in a washout for risk assets. The longer markets fight it with the commodity crazy town bid and falling DXY, the higher the Fed will be forced and the more dramatic the end tightening shock.