DXY was weak last night and looks like it might break down:

The Australian dollar popped with BTFD:

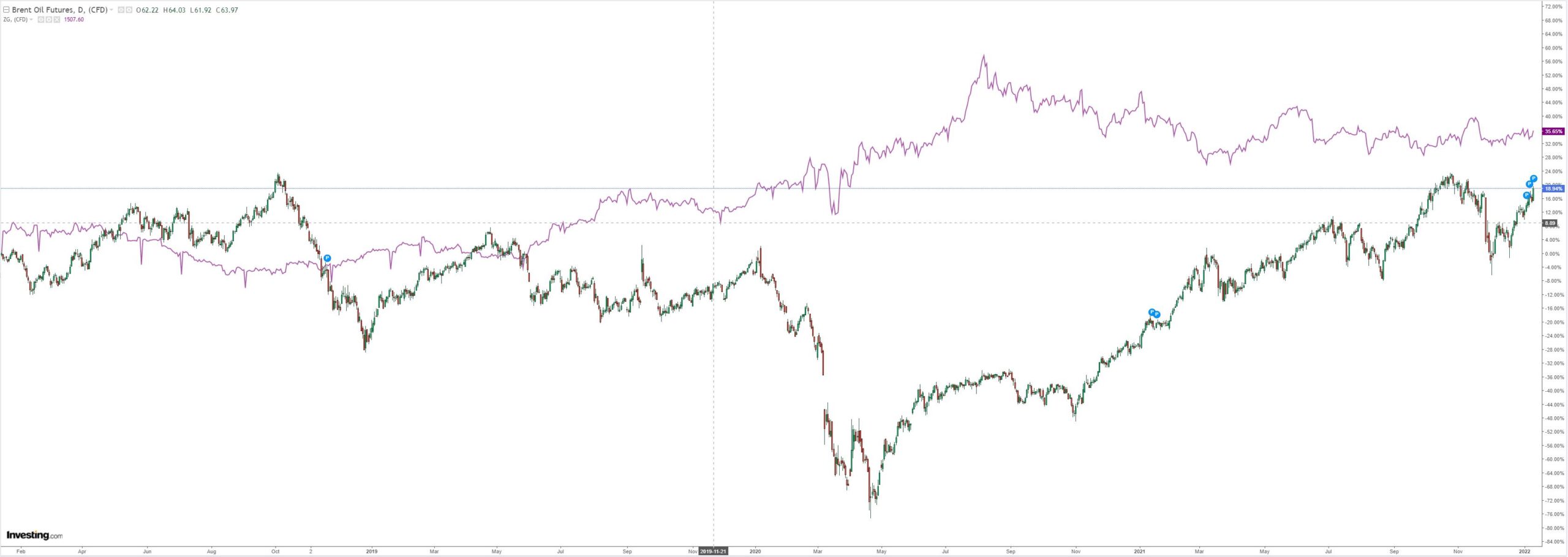

Oil is raging higher:

Advertisement

Base metals were strong:

And big miners:

EM stocks popped:

Advertisement

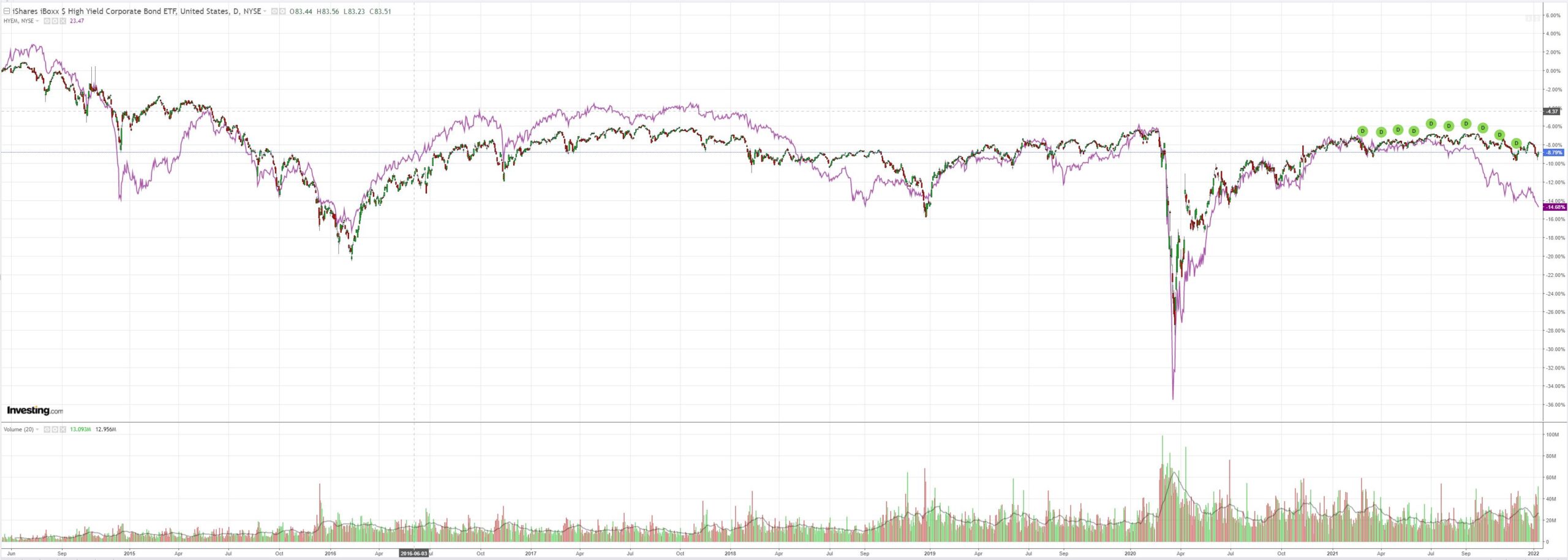

But EM junk is still warning about growth ahead:

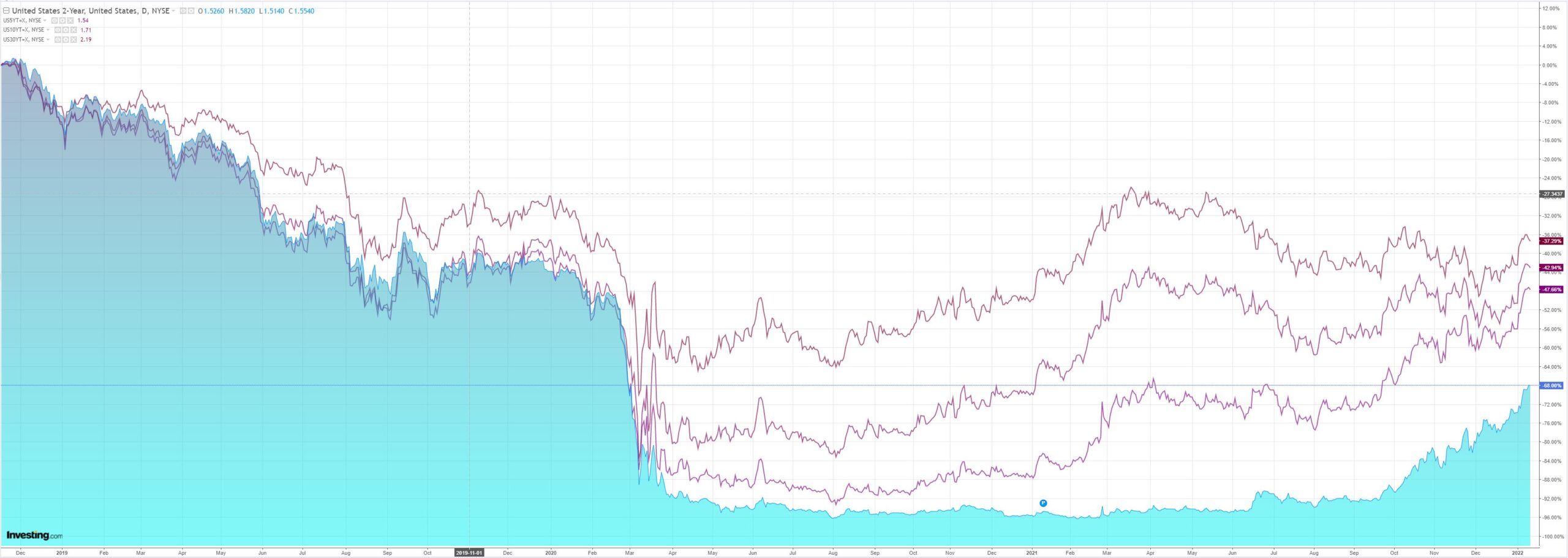

So is the US curve as it suddenly flattened:

Helping lift Growth:

Advertisement

Westpac has the wrap:

The weak US dollar is causing consternation. Morgan Stanley:

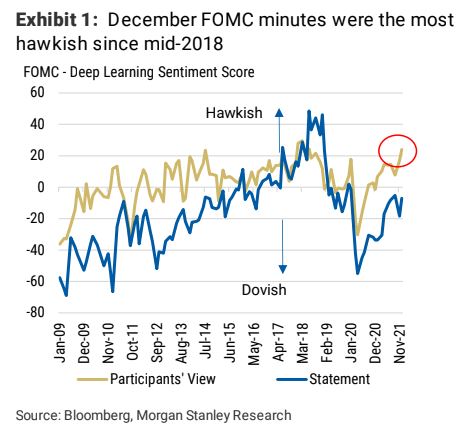

Our framework suggest that the USD uptrend has weakened relative to the strong momentum in 2Q21 and especially against the G10. The EM FX skew looks more balanced. This comes despite more hawkish Fed communication that will likely drive real rates higher and a flatter curve. FOMC communication cycle consolidating in ‘late tightening’: Chair Powell’s introductory remarks to the December press conference were already notably more hawkish than the previous ones and much more than the statement itself. This was confirmed by the latest FOMC minutes, where the FOMC opened the door for much earlier hikes and faster balance sheet normalisation.

For instance, based on our deep learning sentiment model, the participants’ views section was the most hawkish since mid-2018 (Exhibit 1), when monetary policy was certainly much tighter than now. This has also coincided with the shadow rate in the US increasing by more than 150bp over the past six months.

As a result, our framework suggests that the recent increase in real rates and in the short end will continue despite somewhat aggressive market pricing as monetary policy tightening tends to accelerate in the ‘late tightening’ part of the cycle. If confirmed by the January FOMC statement, current communication would be consistent with lift-off happening in 1Q22.

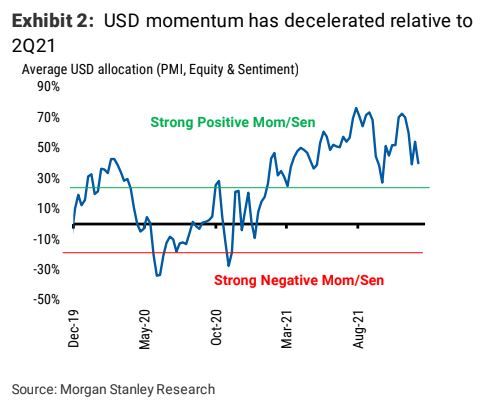

However, we see signs of the USD upside trend weakening, especially against the G10, towards more neutral levels: While the model continues to allocate a decent position to USD, we note a marked decline relative to the strong momentum in 2Q21 (Exhibit 2).For instance, the average of the three directional strategies (versus USD) currently allocates around +40% to USD, which compares to an average of almost +60% in the second half of last year. Most of the decline is explained by FX sentiment and the PMI strategy.

For me, there is a simple explanation for this. The death of Build Back Better has killed the one-way DXY bid. I still think there is one more decent leg in the rally as the Fed tightens and assets deflate but that is now a cyclical not secular bet.

That makes the terminal low for the AUD in this cycle higher as well.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.