DXY was stable Friday night:

AUD fell across the board:

Even oil flamed out:

Base metals were mixed:

Big miners woke in fright:

EM stocks are headed for new lows:

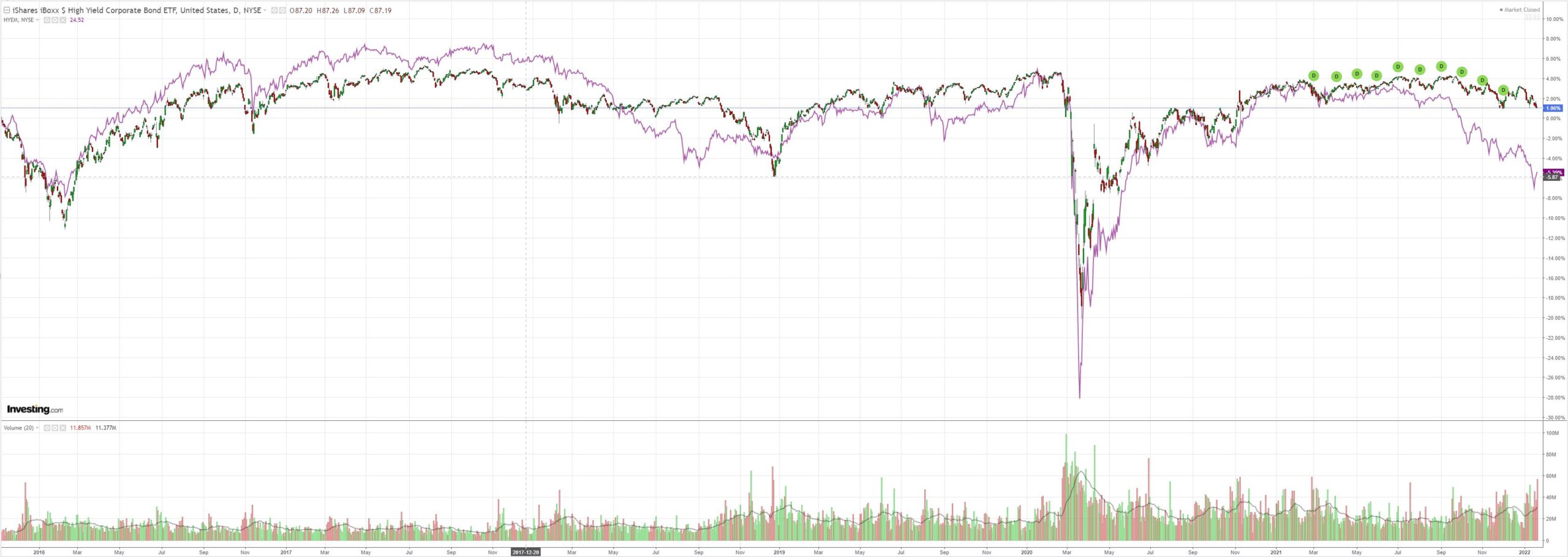

EM junk lifted a bit more but the trend is very bad. Moreover, US junk is fraying a little:

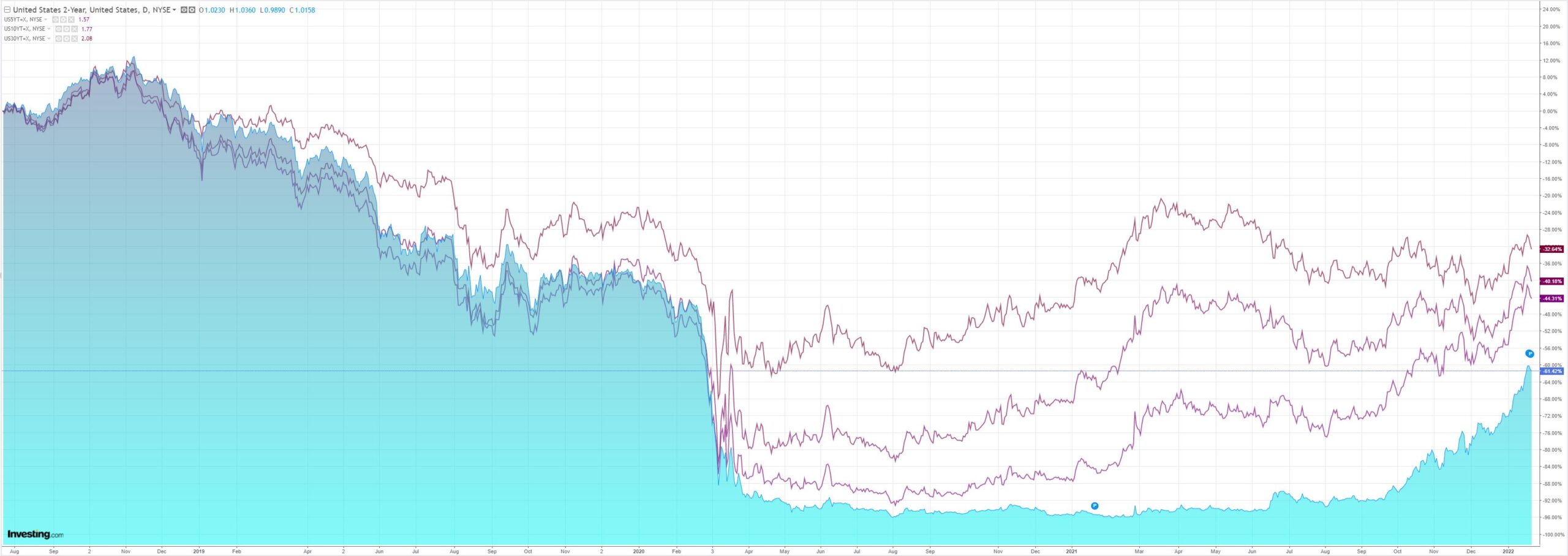

Yields were smacked and curve flattened:

As stonks gave way:

As expected, what I am still thinking of as a mid-cycle adjustment is underway. I don’t think it can stop until the Fed puts a sizeable dent into the oil price. Given Wall St has decided to step in front of this oncoming train with a crazed commodity bid, that’s going to take a while, and more rate hikes.

While the Fed cuts Wall St down to size, DXY is still likely to stay well bid and AUD struggle. Goldman sums it OK:

USD: Sticking with Dollar-neutral trades on front-end rate divergence. At this week’s FOMC meeting the committee will likely lay the groundwork for winding down its bond purchases and raising rates in March. Although the broad Dollar has stumbled to start the year—and our economists’ baseline forecast for four rate increases this year is now priced in—we continue to prefer USD-neutral expressions in FX markets for now. Front-end rate differentials have moved significantly in the Dollar’s favor vs the Euro, where front-end rates have increased less, and especially vs the Yuan, where front-end rates have recently declined on PBoC easing (Exhibit 1). ECB President Lagarde said Thursday that the US and Europe are “in very different situations”, and that the Governing Council (GC) has “every reason to not react as quickly and as abruptly as we could imagine the Fed might”. While the GC may turn its focus to rate hikes later in the year, for the time being changes in US-Europe rate differentials seem likely to favor USD. Moreover, our China economists see a policy easing process underway, and forecast another cut in the PBoC’s Medium-term Lending Facility (MLF) rate to 2.75%. The Dollar can depreciate alongside Fed rate hikes if global growth remains firm—the Dollar depreciated steadily during the 2004-06 tightening cycle, for example, even though the FOMC hiked 25bp at every meeting for two years. But we are not convinced the current macro backdrop favors sustained USD weakness, in light of upside risks to US inflation and downside risks to Asian growth on omicron outbreaks. Should domestic inflation begin to ease, allowing the Fed’s tightening process to remain gradual, we would again consider outright USD shorts (the US Employment Cost Index, reported Friday, will be important to monitor in that regard). For the time being, stick with USD-neutral but pro-growth expressions, including long CAD vs JPY and AUD, and long CLP vs EUR (more details below

AUD: Still less constructive. The Australia labor market report for December beat expectations, particularly the four-tenths drop in the unemployment rate to 4.2%, its lowest level since 2008 and only about 20bp above our estimate of full employment. As a result, we now expect the RBA to end QE in February 2022 (vs May previously) and to start raising rates in May 2023 (vs. November 2023 previously). But our forecast for liftoff remains well beyond the market’s current pricing of a first 15bp rate hike later this year. Moreover, we see downside risks to China growth in the near-term—and broader underperformance in the Asia region due to stricter Covid-related policies—to which AUD is exposed. Thus, we still see reasons to stay more cautious on AUD (and like it as a funder for CAD longs), but the following data releases will be key to watch in the coming weeks and likely important for near-term direction: the CPI report on January 25 (local time), Governor Lowe’s speech the day after the RBA meeting on February 1 (local time), and the Wage Price Index on February 23 (local time).

I see the RBA as very much in the ECB mold. It has plenty of time and will be in no hurry to tighten. It will “look through” any OMICRON wage pressure and demand will be weaker than expected until after winter, participation is strong, labour tightness is much about conditions as wages, immigration is going to return, house prices are weakening fast, China is in bad shape, and the Fed is going to break something.