For the past year BofA Chief Investment Strategist, Michael Hartnett, has been one of Wall Street’s gloomiest strategists (perhaps just below Albert Edwards and Michael Wilson on the permabear scale) warning that global markets are on the precipice of a very ugly turn of events, and predicting that 2022 will unleash a “rate shock” that will hammer risk assets, and as 2022 gradually rolls out, doling out major pain for the bulls, his predictions are finally coming true.

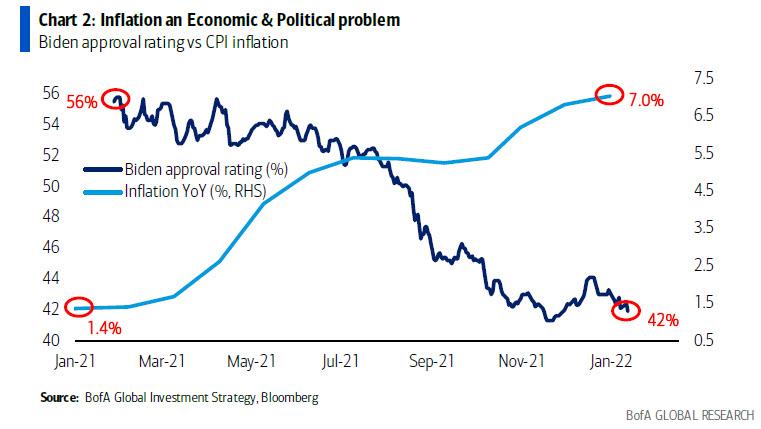

But for all the complaints from stock investors, nowhere is the pain more acute than in the White House, because as Hartnett writes in his latest weekly Flow Show note, US inflation is up from 1.4% to 7.0%, while Biden’s approval rating is down from 56% to 42% past 12 months. One can almost imagine what Biden told Powell during that renomination phone call…

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.