Westpac is out with an updated research note on commodities, contending that 2021 was the top for commodity prices, citing production costs now far outweighed by a “fundamental correction to high(er) prices”. There’s stormclouds on the horizon as the US Federal Reserve begins to taper its bond purchases and stamp on the interest rate hikes, combined with a demand problem in China as production shifts away to consumption, hampering fundamental growth.

This has drastic implications for the one-horse economy that is Australia, because there’s nothing to back up the mining sector if its profitability falters.

Here are the highlights:

High prices are often a cure of high prices as they spur on production and reductions in demand, even more so when technological changes increase demand elasticity.

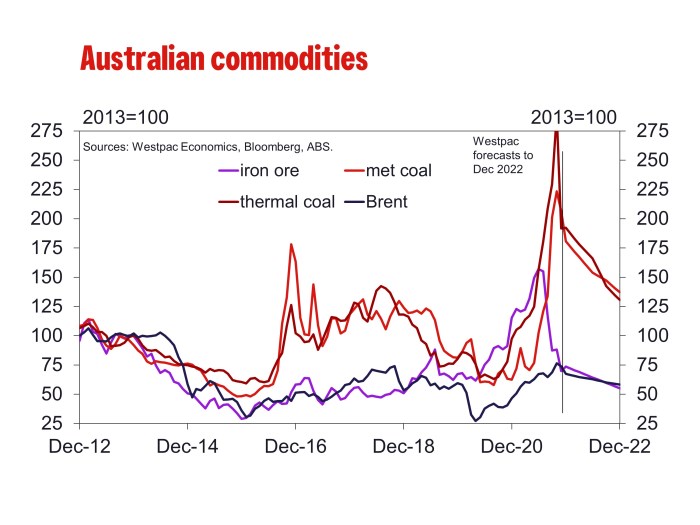

Iron ore is set to continue its drift down to US$75/t by end 2022 while the weather induced shocks to Australian coal exports will be short lived with coal prices set to fall between 24% and 33%.

The current market has significant potential for a strong supply response to combine with demand becoming more sensitive to higher prices (i.e. higher demand elasticity) due to rapid technological advances and ongoing demographic shifts.

At US$70/bbl Brent is now less than half of its 2008 peak (US$147/bbl) and is down almost 20% from the 2021 peak of US$86/bbl.

At around US$9,500/t copper is where it was a decade ago, close to 10% down from the 2021 peak of US$10,500.

At US$101/t iron ore more than halved from its 2021 peak of US$234/t (a record high) while met coal has fallen 22% from its 2021 peak of US$346/t and thermal coal is down 37% from the US$257/t peak this year (also a record high). The record high for met coal was US$370/t in early 2011.

Our forecasts have iron ore drifting down to US$75/t by end 2022.

Met coal prices are forecast to fall to US$205/t by end 2022 while thermal coal is expected to ease to US$110/t.

Our Brent forecasts ease back from US$70/bbl to US$63/bbl by end 2022. Next year is going to be a significant test for the mantra that “high prices are a cure for high prices” particularly for energy.

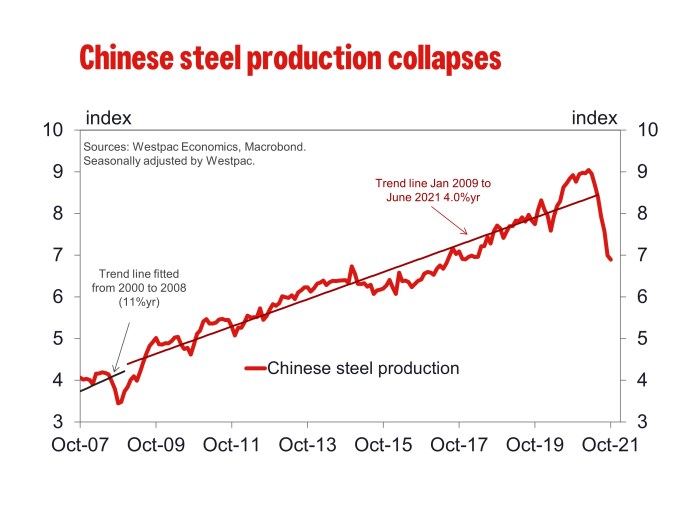

The Base Metals Index is forecast to fall around 10% to 202 by end 2022. China has been a primary source of demand for base metals since 2003 but we think this trend has started to come to an end. With the decline of investment and production as key growth drivers, this will see diminishing incremental economic growth and a reduction in materials demand as a share of output just as a declining required reserve ratio and ongoing property issues portend a peak