Westpac sees yesterday’s Federal Reserve policy decisions, whereby the pace of tapering was doubled and indications of rate rises in 2022 was both brought forward and doubled in scope, as indicative of US economic strength and why “normalization” is being accelerated. Although where that normalization of interest rates will occur in the next cycle is far from discernable – probably only just above 2% and below the peaks of the last cycle:

More:

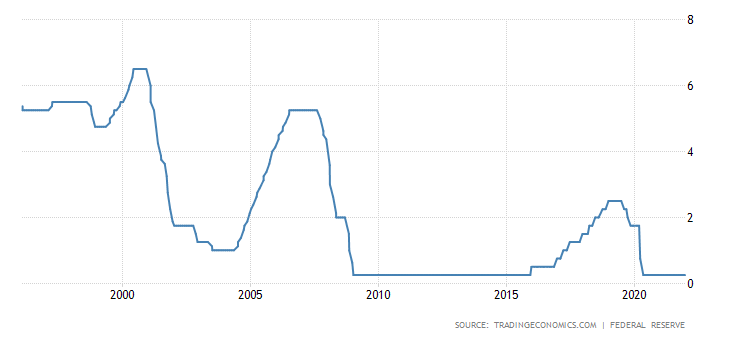

There was a significant shift in FOMC policy expectations between the November and December meetings given strength in the labour market and consumer inflation. Regarding the taper, at the December meeting, the FOMC met our expectations and those of the market, announcing the taper pace will double from January, bringing their asset purchases to a conclusion by mid-March. The Committee’s fed funds rate view is now also in line with our expectation for 2022, with three hikes to 0.875% forecast. In 2023 and 2024, the FOMC see two more rate hikes than we do, leading to an end-2024 level for the fed funds rate of 2.1% (Westpac 1.625%).

The primary justification for this decision and forward view is persistent strength in the US economy. A small net downward revision to the cumulative gain to end-2024 notwithstanding, annual GDP growth is expected to remain above trend throughout – 2021 to 2024 growth is now forecast to be 5.5%; 4.0%; 2.2%; and 2.0%.

Offsetting the impact of higher interest rates over the period, the labour market is anticipated to strengthen, the unemployment rate falling from 4.3% (previously 4.8%) at end-2021 to 3.5% (previously 3.8%) in 2022 – a level it is expected to maintain until the end of 2024. This rate of unemployment is in line with the multi-decade lows seen prior to the pandemic, implying the Committee believe the economy will not only achieve ‘maximum employment’ but sustain it.

Though the FOMC clearly see upside risks for inflation, with both supply and demand factors supportive, their core view remains that inflation will come back to target through 2022 and 2023 – the 2021-2024 median forecasts are now 4.4%; 2.7%; 2.3%; and 2.1%.

The range of inflation forecasts of the Committee are biased to the upside; however, by 2024, the difference is immaterial, the core PCE range for that year is a tight 2.0-2.3%. It should be noted however that the fed funds rate range underlying this inflation forecast is heavily skewed, being 1.9%-3.1% (previously 0.6%-2.6%). Although, the upper end of this range is a minority view, with only 5 of 18 participants seeing the fed funds rate around 3.0% in 2024, and just 2 of 17 expecting a longer-run rate around that level. For both periods, the next highest forecast is 50bps lower, circa 2.5%.

Consistent with the forecasts of the Committee, the comments made by Chair Powell at the press conference had a heavy focus on the strength of US economic activity and the persistence of momentum in 2022. While these gains are expected to support inflation, they are not projected to stop it falling back to target as supply-side factors and the demand-side influence of fiscal policy abate.

History supports this view. In the decade prior to the pandemic, inflation consistently disappointed the FOMC’s 2.0%yr target, even when the labour market was fully employed. Arguably though, given the starting point for inflation and low labour force participation, persistent strength in employment and above-average inflation expectations run the risk of continued upside surprises for wages and inflation over the forecast period.

All in all, the FOMC’s December decision and guidance is consistent with our views. While we believe the FOMC will eventually only raise the fed funds rate to 1.625% instead of 2.1%, over the forecast period the risk of additional rate hikes will be priced into term interest rates, particularly the 10-year yield which we see rising to a peak of 2.30% as the hiking cycle begins. To this view, the anticipated long-duration of this growth cycle and a tight labour market is critical, along with the consequent risk that inflation will print meaningfully above target in 2023 and beyond.

Promoting sustainable growth and managing related inflation risks requires the measured but pro-active approach to policy that the FOMC is undertaking.