Welcome to the new post-iron ore Chinese stimulus pattern. There’ll be some stimulus around infrastructure and property, but it will be much smaller and less iron ore intensive than previously. Morgan Stanley with the note:

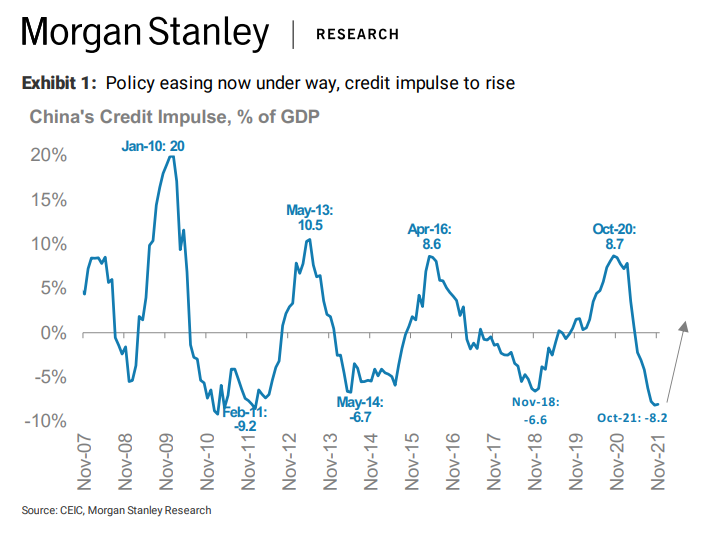

Over the years, China has experienced a number of mini-cycles. This year brought another iteration – the economy started the year on a strong footing but has entered a policy-induced downturn. The policy cycle has shifted from overtightening to easing, and our chief China economist Robin Xing estimates that GDP growth will accelerate to 5.5%Y in 2022. Investors we speak with are less confident in the recovery, but we think that this mini-cycle repeats a familiar pattern and policy-makers have already taken steps to reverse the downturn. Moreover, the recent statement after the Central Economic Working Conference confirms their resolve and increases our confidence on the recovery call.

China’s mini-economic cycles tend to follow policy cycles. Most downturns begin because of macro or regulatory tightening. Tighter policy starts out as countercyclical, typically when external demand is strong. But eventually it becomes pro-cyclical, sometimes because external demand conditions deteriorate (e.g., the onset of trade tensions in mid-2018). Once growth decelerates beyond the policy-makers’ comfort zone, their priorities shift to stabilising growth and preventing an adverse spillover impact to the labour market. Their policy stance shifts accordingly – they first pause on tightening macro and regulatory policies, and then start to ease.

The full text of this article is available to MacroBusiness subscribers