The dual threats of rising inflation and the spread of the new omicron variant are spooking risk markets going into the last sessions of the trading year, with a Santa Rally definitely off the table. Wall Street fell over with European stocks having high volatility amid lower finishes while currency market volatility abated somewhat with more safe haven buying in Yen, but also Euro as USD strength waned a little. Commodity markets didn’t see any relief from selling with oil prices down more than 3%, while gold deflated back below the $1800USD per ounce level.

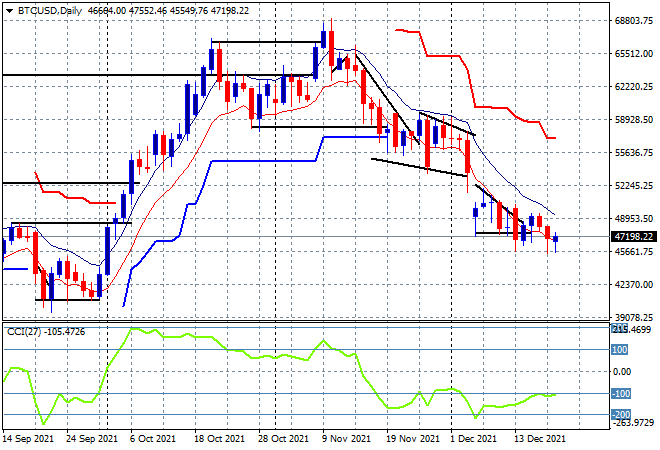

Bitcoin is continuing its deflation, unable to gain traction as it retraces back down to the $47K level, making a series of new daily lows last week as momentum remains nicely oversold with no upside pressure evident. The technical picture still remains grim for crypto with the next support levels are quite far away at the September lows around $43K, with daylight below to $30K next:

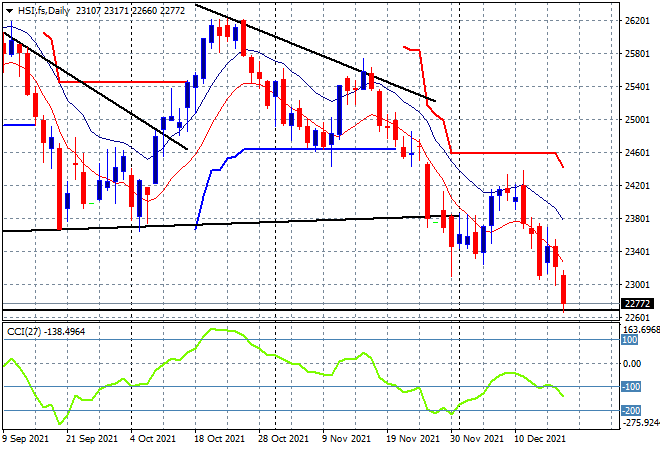

Looking at share markets in Asia from Monday’s session, where mainland Chinese shares put in very poor sessions to start the week, with the Shanghai Composite down over 1% to 3593 points while the Hang Seng Index slumped again, down nearly 2% to 22744 points. As this dead cat bounce turns into a full on correction, the price moves below the 23000 point level have now wiped out any support, heading to the 2020 lows (lower black line) with the potential to start a new bear market:

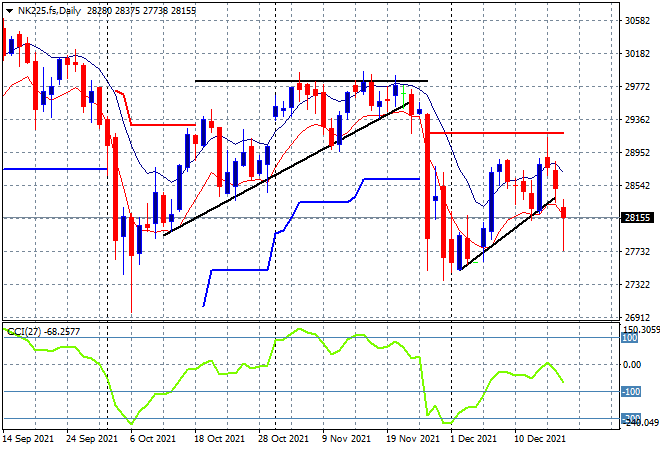

Japanese markets also pulled back sharply due to monetary easing comments from the BOJ, with the Nikkei 225 down over 2% to 27937 points. Price action has broken below the nascent uptrend line from the start of the month, with resistance too heavy here as daily momentum rolls over further into the negative side. This looks like yet another failed ascending triangle within a downtrend, essentially a bull trap that should see price revert back to the 27000 point proper soon:

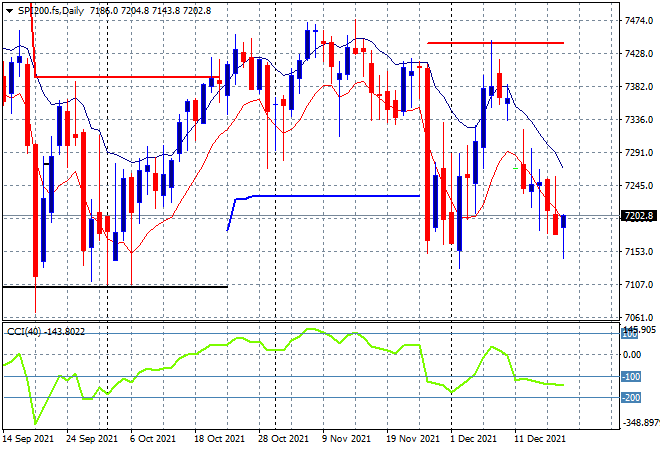

Australian stocks were the relative outperformers, with the ASX200 closing only 0.3% lower but looking very weak here too, closing at 7284 points. SPI futures are indicating a potential open around the 7200 point level, so its not looking good for a Santa rally as the market returns to the November lows. The daily chart does not look pretty with daily/weekly support coming up very quickly:

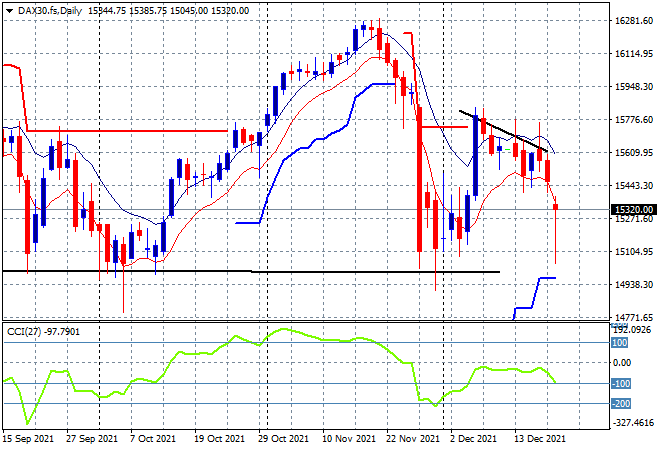

European markets all had lower finishes with the FTSE off by 1% while the German DAX finished nearly 2% lower at 15239 points. Intrasession volatility was very high here with even lower lows before a late recovery alongside Wall Street still saw steep losses. As I said yesterday, any falls below the low moving average indicate short term support has evaporated and with possibly more lockdowns on the continent up ahead as Christmas comes around, confidence is evaporating:

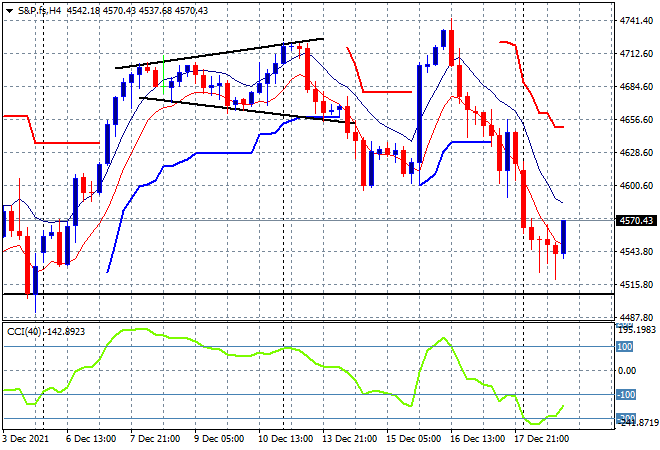

Wall Street suffered yet another loss on the OMICRON fears with the NASDAQ leading the way, down over 1.2% while the S&P500 lost over 1% closing at 4568 points. The four hourly chart is now showing the way with this dip taking its down towards the 4500 point level, although there is some hope here as a deceleration short term pattern is quite evident, with that last candle showing the BTFD team may yet be stepping in:

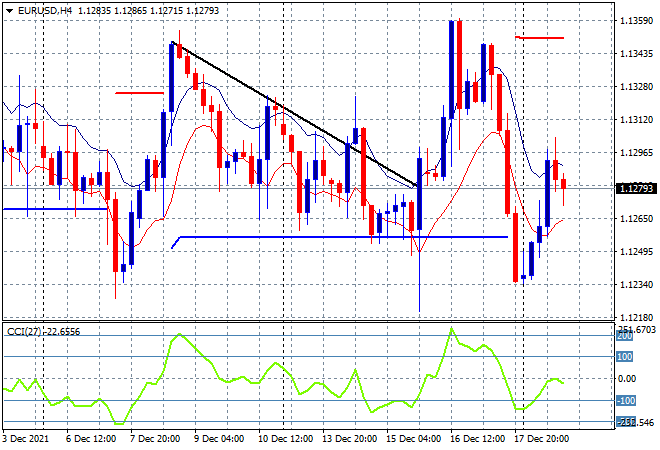

Currency market volatility remains high although without any economic catalysts last night there was little for algos’ to go on, with Euro experiencing a reversion to the mean trade heading it back towards the 1.13 handle. The four hourly chart shows price getting back above the previous ATR support at the mid 1.12 level that had nominally held the last few weeks, with momentum getting back to more neutral settings, but this pair is still looking weak at best with a sideways bent still evident amid the volatility:

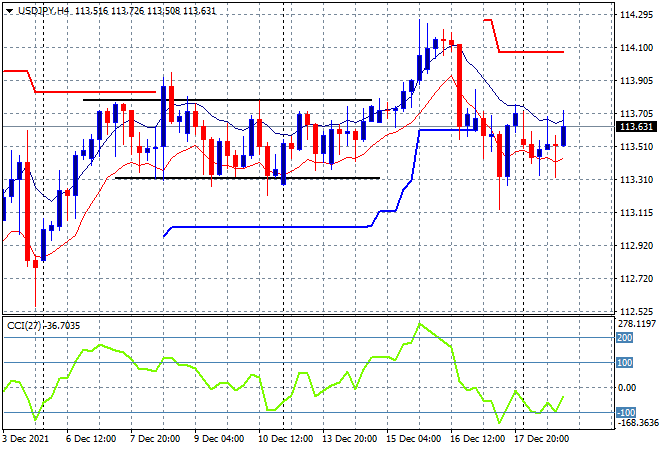

The USDJPY pair also showed a return to it mid week point of control at just below the 114 level in a very mild lift overnight despite the interesting comments coming out of the BOJ. The four hourly chart is looking quite sanguine again with that point of control keeping prices stuck at just below the 114 handle, although a new weekly low has not yet been made, momentum remains slightly negative at best and the high moving average is not under threat to the upside:

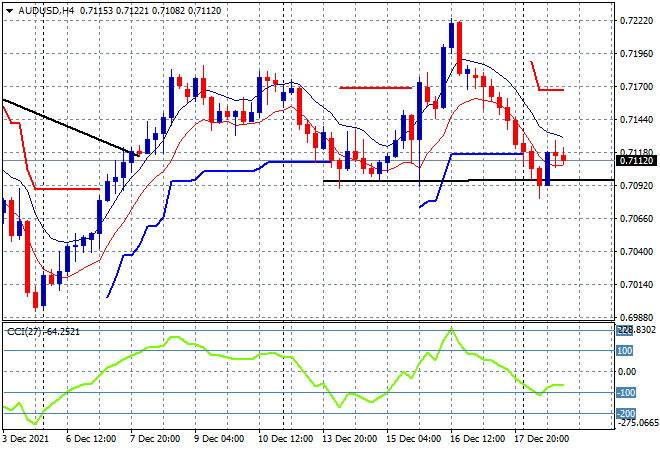

The Australian dollar had a flat start to the week despite the surprise PBOC cutting of rates, with a weak finish just above the 71 handle overnight, not helped by more selling on commodity markets, still making for a very interesting short term picture. The failure to breakout after clearing the previous weekly highs continues to spell more downside volatility for the Pacific Peso, where I’m watching support at the 71 level that must hold:

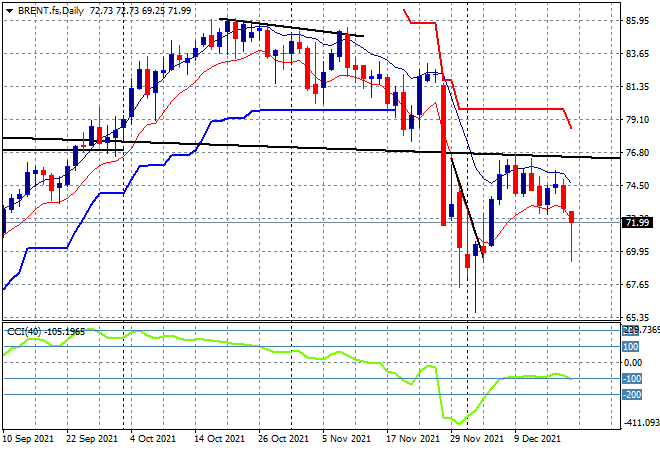

Oil prices exhibited higher volatility alongside European equities as demand concerns continue to mount with Brent crude dropping below the $72USD level, although it slide far further intrasession to break the $70 level. The nascent bounceback still has all the hallmarks of a dead cat bounce as daily momentum inverts and price moves down towards the psychologically important $70 level:

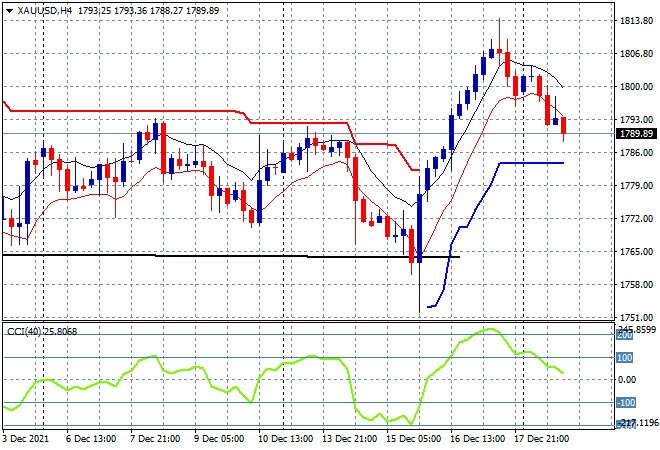

Gold is disappointing the bugs again with another slide back below the $1800USD per ounce level, failing to provide a counter to the other safe havens as concerns over inflation evaporate amid COVID concerns. As I said previously, sentiment alone cannot push the shiny metal higher but watch for potential support to come up shortly here at the recent weekly highs:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out!