Goldman Sachs with the note:

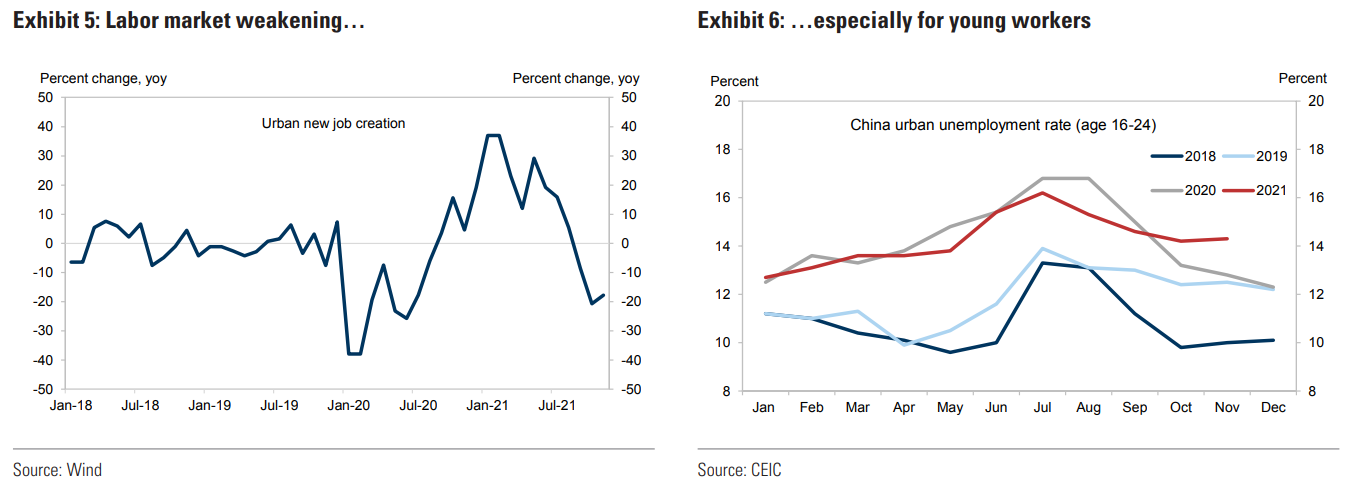

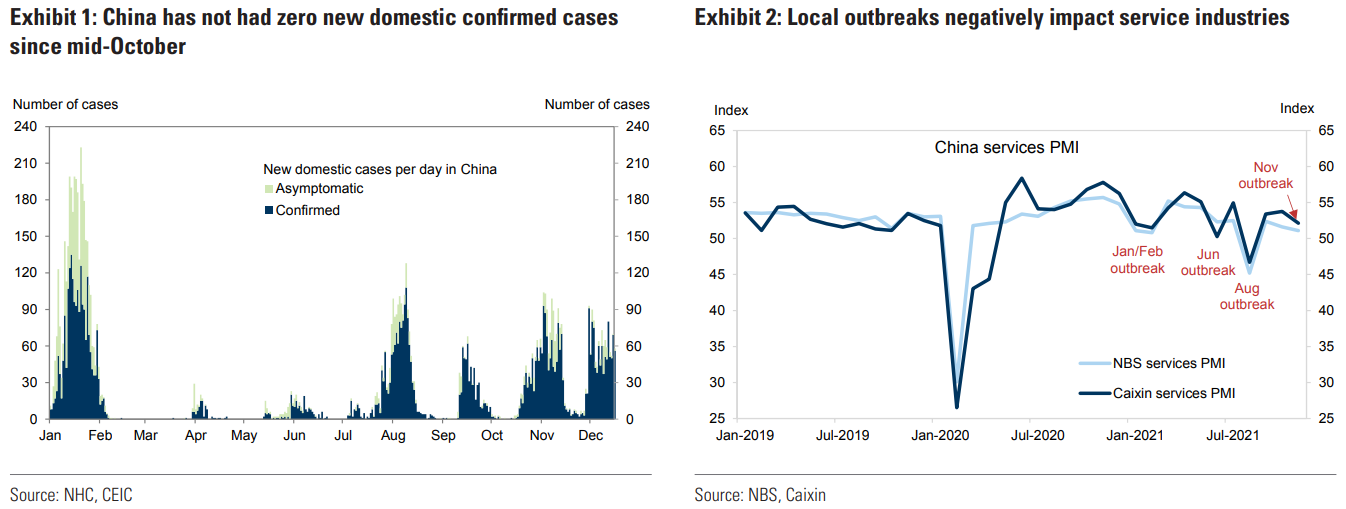

Covid restrictions weighed on consumption and services in November: Local outbreaks have become more frequent in China in recent months. November data show clear evidence of Covid-related restrictions weighing on consumer activity. Consumer services and small businesses are most affected and remain 10%-15% below their pre-Covid trends. Labor markets have softened because sectors hardest-hit by Covid restrictions tend to be more labor-intensive.

From “zero Covid” to “dynamic zero Covid”: Despite the toll “zero Covid” policy has taken on the economy and the risk from the more transmissible Omicron variant, we do not think the Chinese government will change course and adopt a “live with Covid” policy anytime soon. The human and economic costs from such a change could be enormous given China’s large population and low vaccine efficacy. Policymakers have shifted to a “dynamic zero Covid” approach, aiming at controlling local outbreaks early on rather than zero infections.