Tim Wilson is one of several Liberal MPs arguing that Australians should be able to access their superannuation to pay a housing deposit.

However, the Labor-aligned McKell Institute has slapped down the proposal in a new report, claiming it would send prices soaring:

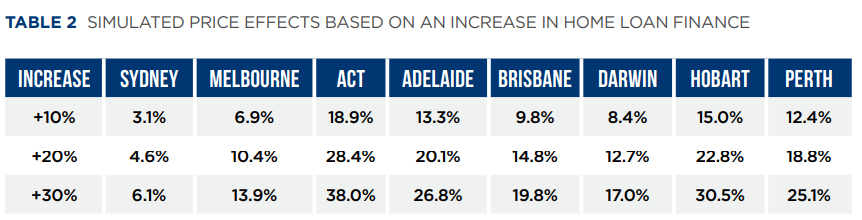

We assume that the effect of any policy to allow early super release would cause a one-off effect, by bringing forward the purchase decision of private renters who are already saving for a deposit. The model is estimated on quarterly data and therefore provides predictions on that basis. We assume that an increase in lending would cause prices to increase for 4 successive quarters, after which all private renters currently saving but able to buy earlier than planned will have done so.

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.