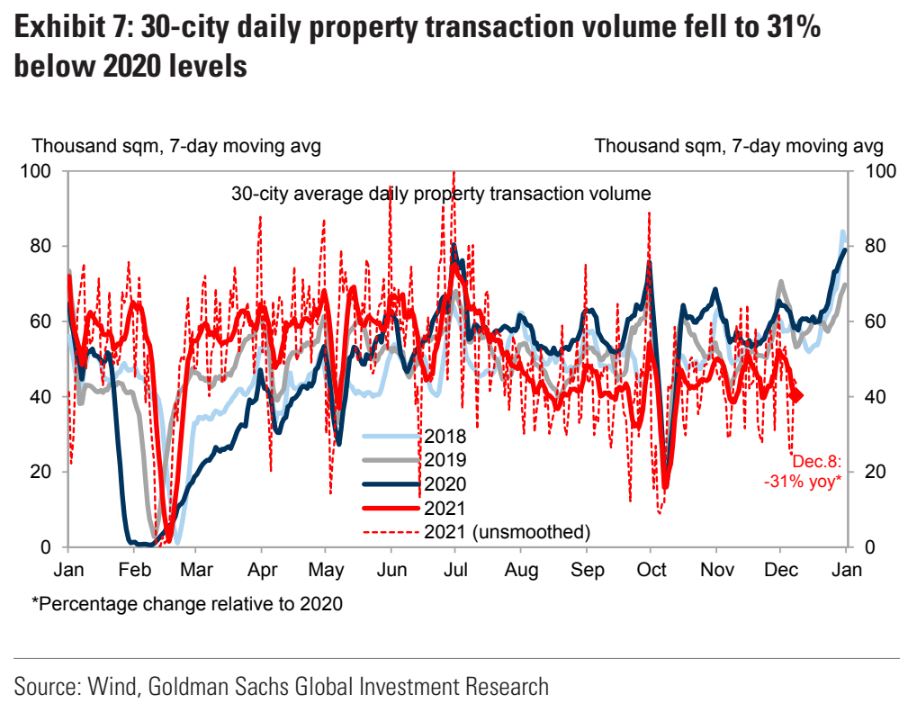

As markets celebrate the bankruptcy of Evergrande as a reason to buy all the things, under the bonnet the Chinese property bust is getting worse, not better.

Sales by floor area are as bad as at any time this year in the past week and the forthcoming holiday sales super-season is shaping as a writeoff:

Why wouldn’t it be as a bevy of household name developers go under in the full view of the public?

Advertisement