Welcome to the new post-iron ore Chinese stimulus pattern. There’ll be some stimulus for infrastructure but it is smaller than property and less steel-intensive plus the property adjustment will keep a lid on it via weak land sales. TSLombard with the note:

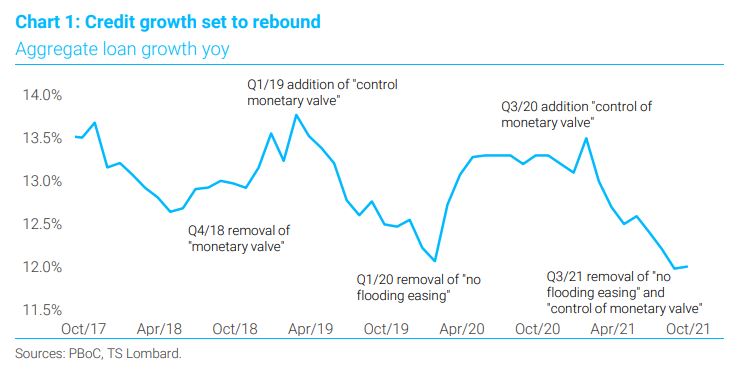

Beijing is shifting gears, moving from marginal easing to broader stimulus measures. As forecast, the Sixth Plenum has proved a turning point: after the elite political gathering, the PBoC signalled a dovish turn and announced a 50bps RRR reduction. Meanwhile, the Politburo yesterday confirmed easier property-sector policy and more expansive fiscal measures; we expect a recordhigh special-purpose bond quota for 2022 in the region of RMB 4trn. Our base case is playing out: China activity is stabilizing while credit and infrastructure growth are bottoming. We forecast GDP to reach 4.7% yoy in 2022. The Central Economic Work Conference at the end of December will give a clearer idea of the official GDP target – the number rumoured is 5-5.5% yoy. The broader easing signal marks a fresh stage in the first stimulus cycle of the “Common Prosperity” era. Under the new growth paradigm, China first ramped up support for government favoured green/tech/new infrastructure in an attempt to stabilize activity without using traditional credit levers. We think this policy pattern will repeat and open up a new type of defensive equity and credit play, when China slows policy–favoured-sectors are likely to outperform.

China growth has been decelerating rapidly since July but Beijing has turned more accommodative only gradually. A slower transition from neutral to stimulus is part of the new “cross cyclical” economic framework (details here). Politics was the other key driver of a delayed stimulus shift. Central authorities were not in panic mode and so chose to wait until the next scheduled central political gathering (Sixth Plenum) before signalling a shift to broader easing.