“By Gareth Aird, head of Australian economics at CBA:”

| ■ | The 2021/22 Mid‑Year Economic and Fiscal Outlook (MYEFO) is scheduled to be handed down on 16 December. |

| ■ | The MYEFO will show an improved Budget bottom line along with upgraded economic forecasts. |

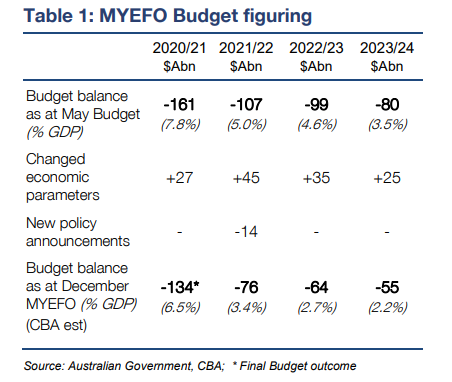

| ■ | Our point estimate for the revised underlying cash deficit in 2021/22 is $A76bn (3.4% of GDP). |

Overview

The 2021/22 Budget was handed down on 11 May. Since then the Australian economy has been through another large negative shock due to the Delta‑induced lockdowns. A shock of the magnitude experienced over the September quarter would normally lead to a budget downgrade. But in a quite extraordinary development the fiscal position looks better over that period relative to what was forecast in the Budget. Much stronger revenue than expected, particularly on the corporate tax front, underpins the improvement.

A brighter economic outlook compared to Budget time will also be reflected in the MYEFO next week. More specifically, we expect the Government to make decent upgrades to their economic forecasts and by extension the fiscal projections.

Our working assumption is that the MYEFO is not a “policy document” and we do not expect it to contain anything major in the way of policy announcements. Rather it should simply contain updated economic forecasts and fiscal projections including the operating statement, balance sheet and cash flow statement. Detailed commentary will accompany the updated figures, as is always the case.

Both revenue and expenditure up

On our estimates, changes to the economic parameters that drive budget forecasts will deliver an improvement of ~$A45bn in 2021/22. Parameter changes primarily relate to changes in economic forecasts, particularly nominal GDP which drives the revenue side of the equation, as well as the level of unemployment which underpins welfare payment forecasts. The news around both nominal GDP and the labour market outlook is better than expected since the May Budget despite the Delta‑induced lockdowns.

On revenue specifically, a stronger tax take due to both higher personal and corporate tax receipts means the money has been flowing into the Government’s coffers at a better rate than forecast.

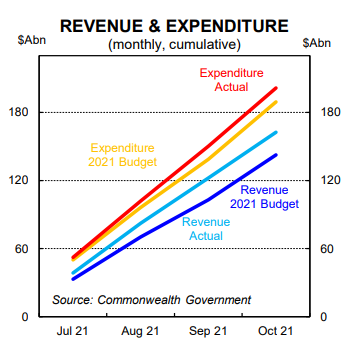

Total receipts to 31 October 2021 were $A20.2bn higher than the Budget profile (see facing chart). Our fiscal model suggests this figure will swell to $A50bn by 30 June 2022. Allowing for a more conservative approach taken in the MYEFO means that we expect a revenue upgrade of $A45bn in 2021/22 in the MYEFO.

Government payments will also be larger than expected in the Budget primarily because of the support payments due to the extended lockdowns in NSW and Victoria. These payments fall under the umbrella of ‘policy announcements’.

Total expenditure to 31 October 2021 was $A12.4bn higher than the Budget profile. Payments are likely to push a bit higher over the next two months relative to the Budget profile, but not by a lot. From there, notwithstanding any policy announcements, the expenditure profile is likely to improve a little given an anticipated sharper decline in unemployment relative to the Budget profile. As such, we pencil in an upward revision to expenditure of $A14bn in 2021/22 in the MYEFO.

Combining our forecasts for revenue and expenditure means that we look for the revised 2021/22 underlying cash deficit in the MYEFO to be $A31bn lower than forecast in the Budget. This means we forecast the 2021/22 underlying cash balance to be revised to $A76bn (3.4% of GDP) in the MYEFO.

Looking further ahead, we expect to see downward revisions to the size of the projected deficits over the forward estimates due to an upgraded economic outlook. These projections, however, should be taken with a pinch of salt. An election will be held in in H1 22 and this will no doubt mean more policy announcements that will result in higher expenditure in coming years than is currently baked into the Government’s fiscal projections.

In summary, the size of the projected budget deficits will remain large. But overall we can look forward to some good news in the MYEFO relative to what was presented in the May Budget.