Well…that escalated quickly. DXY was firm Friday night and EUR soft:

Despite muted major moves, the Australian dollar was slaughtered on the crosses, taking out key support levels for both a bearish descending triangle and head and shoulders top neckline:

Oil and gold were volatile but fine:

Base metals soft:

Big miners were murdered:

EM stocks have very ugly seventeen black crows pattern:

But junk did OK:

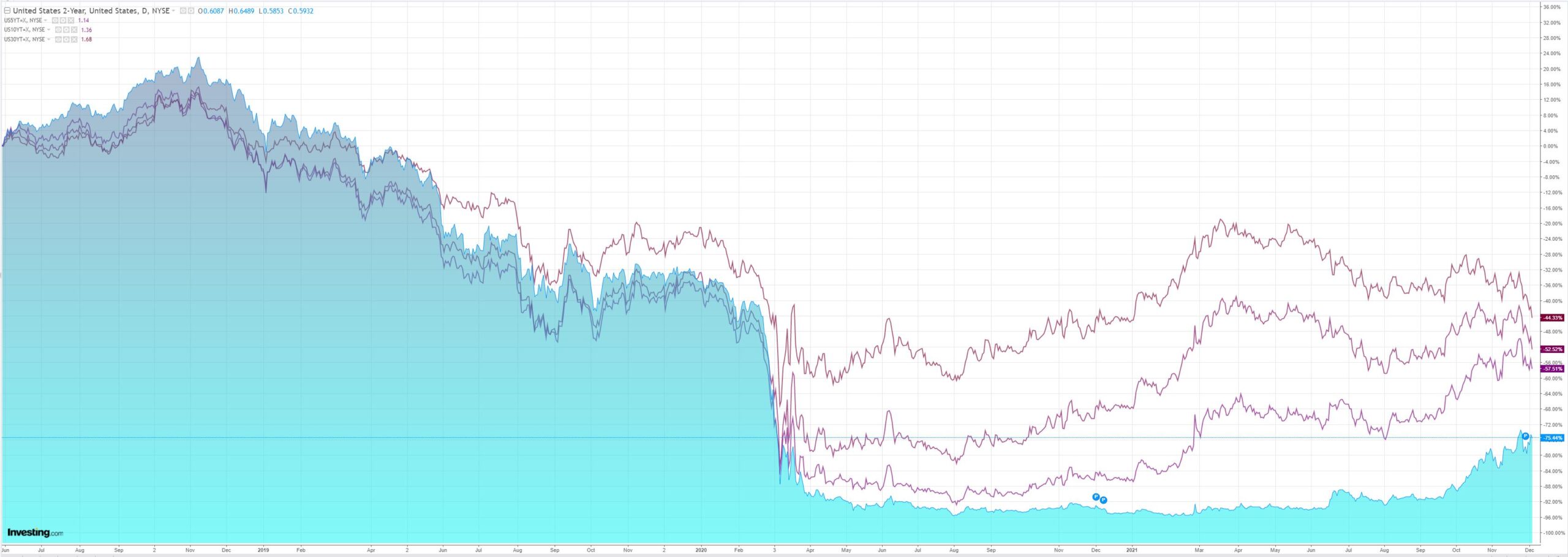

As US yields free fall towards curve inversion:

Which no stocks liked, besides Defensives:

The US jobs report under and overshot expectations:

Total nonfarm payroll employment rose by 210,000 in November, and the unemployment rate fell by 0.4 percentage point to 4.2 percent, the U.S. Bureau of Labor Statistics reported today. Notable job gains occurred in professional and business services, transportation and warehousing, construction, and manufacturing. Employment in retail trade declined over the month.

…The change in total nonfarm payroll employment for September was revised up by 67,000, from +312,000 to +379,000, and the change for October was revised up by 15,000, from +531,000 to +546,000. With these revisions, employment in September and October combined is 82,000 higher than previously reported.

The soft headline was largely owing to seasonally-adjusted numberwang. Revisions were good and unemployment plunged owing to a stubbornly low participation rate. That drove strong wage gains of 4.8%:

Credit Agricole has the analysis:

…greater uncertainty continues to surround the US participation rate, and whether or not it will return to its prepandemic levels. US policymakers are indeed still trying to assess whether the pandemic has ultimately left permanent structural changes across the US jobs market, which if true could mean that the Fed may be forced to raise rates earlier than thought initially. In any case, most of H122 may be needed for such an assessment, which could in turn see the USD flexing its muscles against the low yielding currencies whose central banks seem stuck in an ultra-accommodative stance forever, namely the JPY and CHF. Later in the day…only a surprising downturn may eventually take some shine off the USD.

DXY was only firm in response to the BLS so why did AUD get smashed? A few points:

- The US unemployment rate is now 1% lower than Australia’s. This is becoming embedded in an inverted yield spread at the short-end of the curve even if the long remains deluded on Australia.

- If the US participation rate does not lift soon then the Fed will be forced into earlier and steeper hikes. This is obviously growth negative and being priced in a pancaking yield curve. Indeed, the belly of the OIS curve has inverted.

- Then we have OMICRON which is spreading like wildfire in South Africa and does not look especially different in terms of health impacts so there’s a safe haven bid building into DXY and away from risk currencies like AUD.

- Europe is lurching towards virus lockdowns.

- Sure, China is stimulating, but only slowly, and the key commodity-intensive property sector is still reeling.

- The AUD technicals now look pretty close to disastrous as well, and markets are not so short that they can’t get more bearish yet.

It ain’t a pretty picture for the AUD as the global economy hurtles towards a mid-cycle slowdown that increasingly looks like it could take on the outlines of a mini-recession.