DXY firmed last night and EUR fell as OMICRON fears eased:

The Australian dollar is at new closing lows on all crosses this morning and appears to be grinding through the 0.71c support level:

Oil capitulated then found a bid as a desperate Goldman issues notes hourly:

Base metals were weak:

But big miners took off just because:

Despite struggling EM stocks:

And junk:

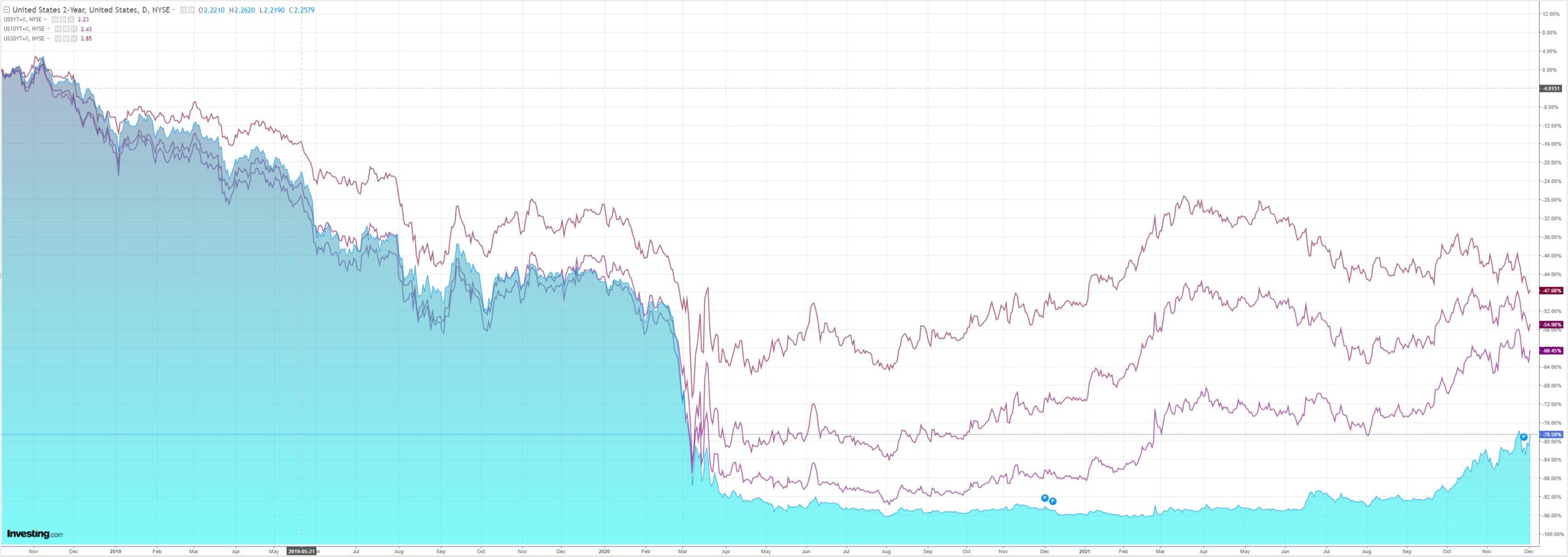

As the Treasury curve pancaking rolls on:

Value led growth for once despite that:

Westpac has the wrap:

Event Wrap

US weekly jobless claims were close to expectations. Initial claims of 222k were just below the consensus of 240k, with continuing claims at 1.956m (est. 2.003m). Challenger job cuts in November of 14,875 were the lowest since 1993, the report citing employees finding it difficult to hire and retain workers.

Fedspeak was hawkish overall, supporting the potential for a quicker pace of QE tapering and rate hikes. Bostic said it may be “appropriate for us to pull forward the lift-off,” and that the FOMC will need to have “optionality”, implying he would be supportive of accelerating tapering. He is concerned about inflation, adding if prices remained elevated in 2022, there would be a “good case to be made in pulling forward more interest rate increases.” Daly also said the Fed might have to taper at a faster pace, but doubted rate hikes will have to be aggressive. Barkin said the December decision will be hard, but agreed with the normalisation stance. Quarles said he supports tapering to start earlier than June. Mester said that “making the taper faster is definitely buying insurance and optionality so that if inflation doesn’t move back down significantly next year we are in a position to be able to hike if we have to”. Recent data “have come in supportive of that case, so I am very open to considering a faster pace of tapering”.

A growing number of companies and officials sought to reassure the public about vaccinations and omicron. Novavax said it’s developing an omicron-specific vaccine, while a Pfizer spokesperson expected its vaccine would have some efficacy.

Eurozone PPI in October was higher than expected. Headline PPI rose 5.4%m/m (est. +3.8%m/m) to an eye-popping +21.9%y/y (est. 19.0%y/y). Ex-energy and construction PPI rose 0.8%m/m to +8.9%y/y. Eurozone unemployment in October of 7.3% (down from 7.4% in Sept.) was in line with expectations.

Event Outlook

Japan: The final release of the November Nikkei services PMI should reflect the sector’s recent improvement as delta risks subside.

China: November’s Caixin services PMI is expected to report robust growth, although restrictions to halt delta present as downside risks.

Eur/UK: The final release of the November Markit services PMI is also due for Europe and the UK. Europe’s retail sales are set to lift in October as demand evens out between goods and services (market f/c: 0.3%).

US: November’s non-farm payrolls are expected to reflect the robust momentum in the economy (Westpac f/c (and market median): 550k) which should also see the unemployment rate edgelower (market f/c: 4.5%). Average hourly earnings growth is expected to remain strong given the limitations on labour supply (market f/c: 0.4%). November’s ISM and Markit services PMIs should continue to signal strong growth in the services sector despite delta. The FOMC’s Bullard is due to speak at the Missouri Bankers Association.

Some pretty whacky market action but, on the whole, an easing of OMICRON fears was good for the growth outlook and therefore a Fed tightening shaping rapidly as a policy error in the Treasury curve. Pfizer reassured:

Pfizer Inc. expects its Covid-19 vaccine to hold up against the omicron variant, an executive said, and data on how well it protects should be available within two to three weeks.

If the new strain proves to be benign or even useful then the base case is a falling AUD as the Fed puts a rocket under DXY and China struggles on.