DXY eased Friday night despite tearaway US inflation:

The Australian dollar was firm:

Oil and gold firmed:

Base metals were soft:

Advertisement

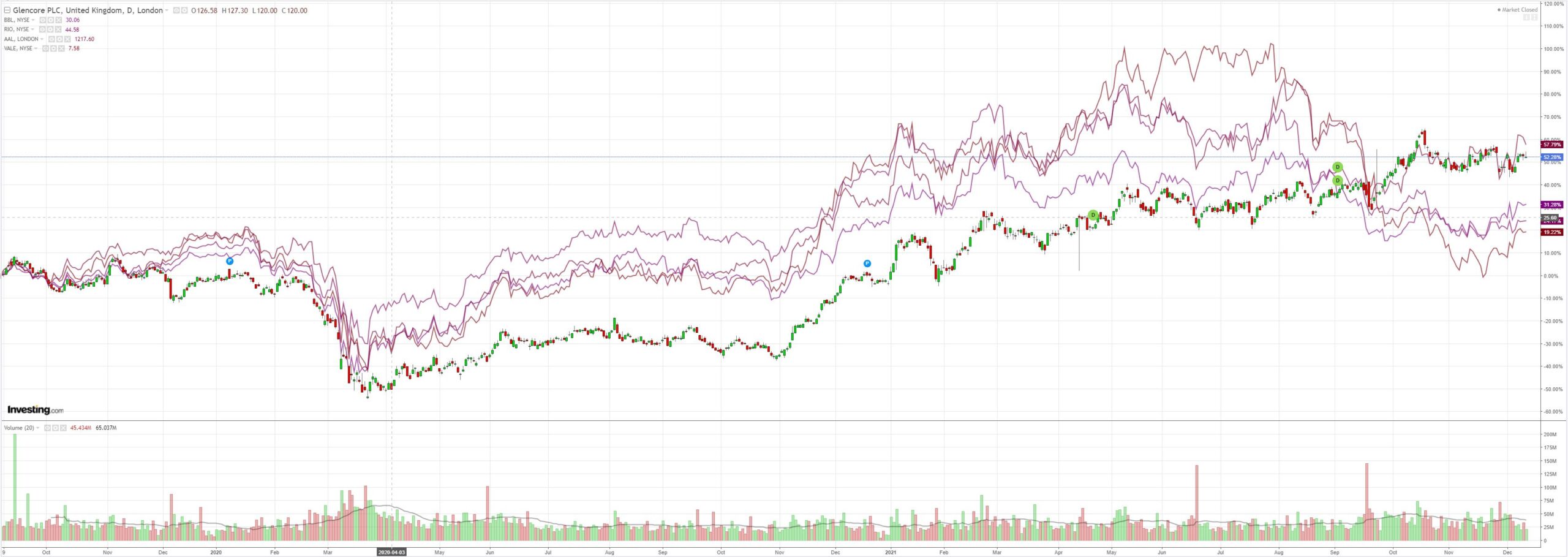

And big miners:

EM stocks faded:

Nut junk rallied:

Advertisement

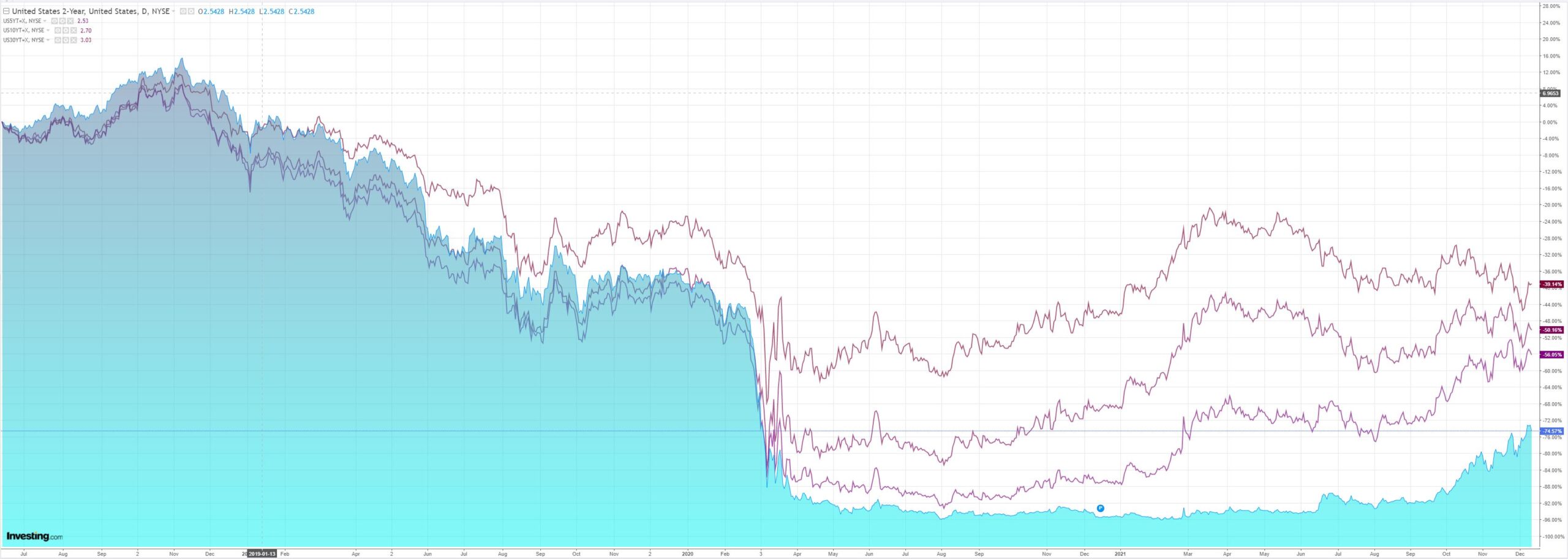

The Treasury curve steepened:

And stock lifted led by GAMMA:

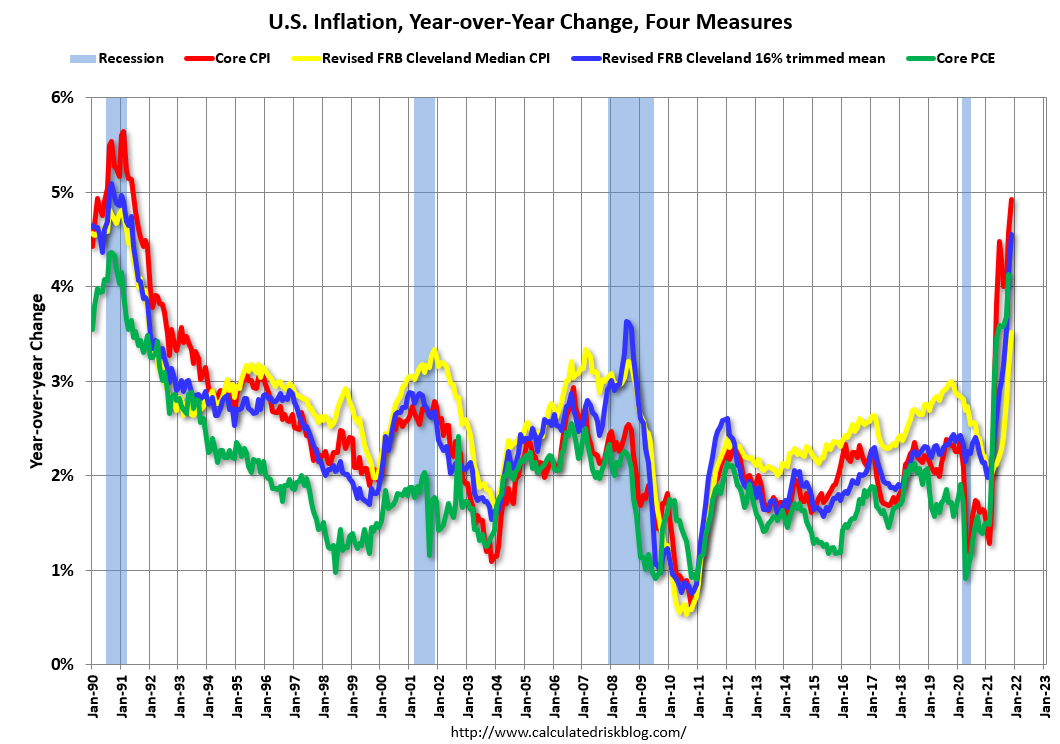

US inflation was very strong but it is going to fade ahead. BofA:

Advertisement

Consumer inflation stayed hot in November as core CPI rose a robust0.53% mom, which boosted the yoy rate to 4.93% from 4.56% yoy—the highest since 1991. Headline CPIjumped 0.78% mom as energy prices spiked 3.5% mom and food rose 0.7% mom. Headline % yoy similarly soared to 6.81% yoy from 6.22%,—the highest since 1982.

In core goods, new cars picked up1.1%mom and used cars surged 2.5% mom as the auto sector remains constrained. The move in used cars was actually lower than expected given that wholesale prices moved up 5.3% mom in September, but this move may have been spread out given that CPI used cars surprised to the upside in the last report, also rising 2.5% mom like in this report. Wholesale prices suggest further significant upside in used cars in the months ahead as the gauge is up 14.5% through November relative to the prior high in May. Outside of autos, core goods components broadly gained as apparel popped 1.3%, household furnishings/supplies rose 0.7% mom, and both recreation and other goods rose 0.3%mom. One exception was education/communication commodities which slipped 1% mom. The breadth of gains in goods likely reflects ongoing constraints in the supply chain as well as the pull forward in the holiday shopping season, which meant earlier discounting in October.

In core services, OER and rent of primary residence stayed hot, growing 0.4%+ mom for the third consecutive month. Travel components also surged as lodging popped 2.9%mom and airline fares soared 4.7% mom. Broader transportation services rose 0.7%mom as car/truck rental also jumped 1.1%, though MV insurance fell-0.8% mom. Outside of that, services components were mixed. Recreation fell-0.5% mom, education/communication and water/sewer/trash were both flat, other personal services inched up 0.1% mom, and household operations popped 1.1%mom. Medical care services grew 0.3% mom but this was below expectations as hospitalsfell-0.3% mom.

Overall, the continued strength in OER/rents indicates that persistent inflation pressures continue to heat up, although the mixed services components suggests we may not need to hit the panic button just yet. The breadth of gains across core goods supports ongoing pandemic-related pressures and the pull forward in the holiday shopping season. Travel components also rebounded as people went home for Thanksgiving, but we could see some softening in the near term given the rise of Omicron. The market response to this morning’s print reflects some disappointment on a headline level but affirmed expectations for the Fed to lean more hawkish. Inflation breakevens declined across the curve, but were concentrated in the front-end, suggesting that market may have been expecting a higher print than what was reflected in surveys. Expectations going in were probably bolstered after Biden’s comments yesterday that today’s print won’t reflect recent energy price declines. Real rates rose by 8 and 6 bps at the 3y and 5y point respectively. Strong persistent inflation pressures reflected in the reading support a continued Fed hawkish pivot and should continue to put flattening pressure on the nominal curve.

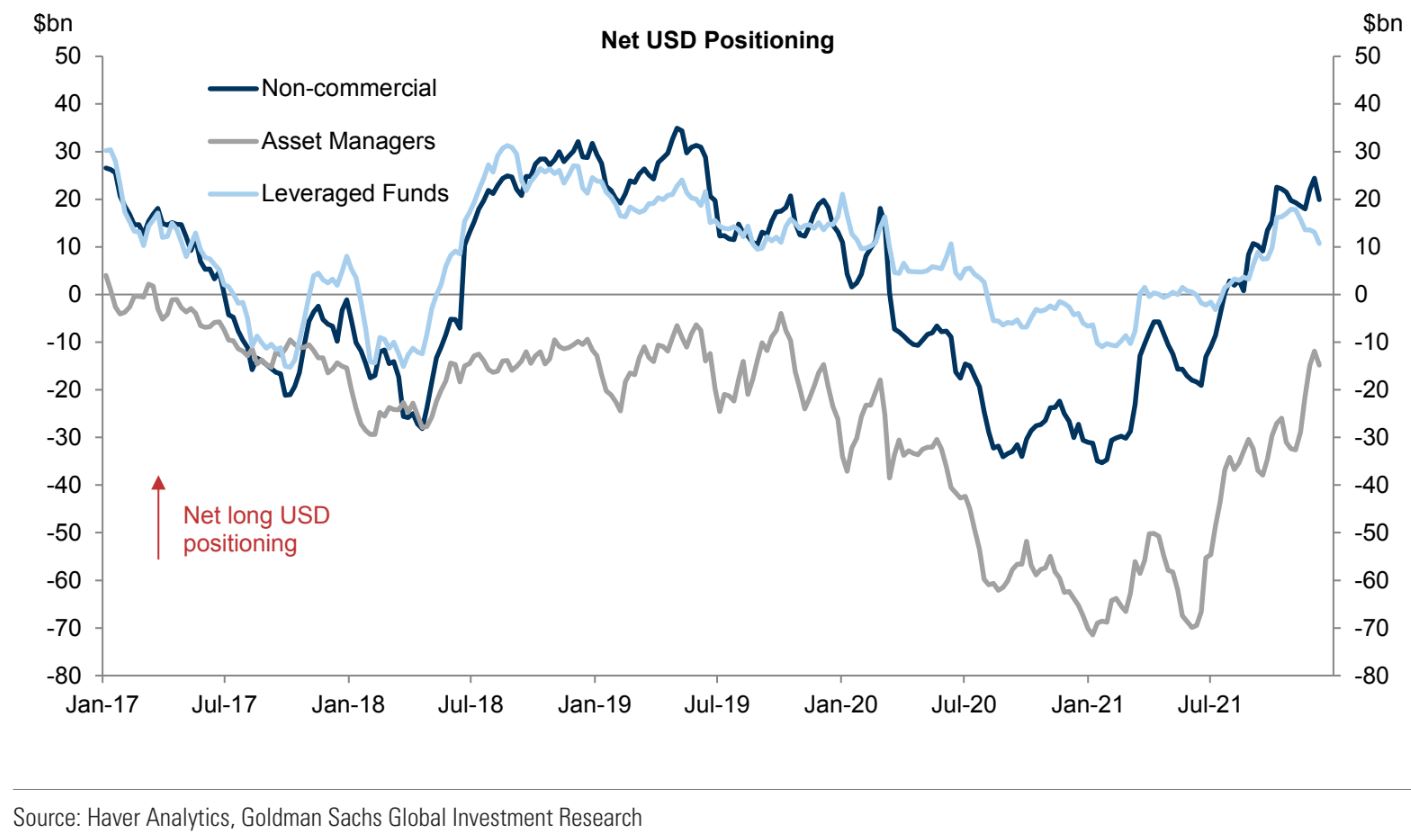

I remain bullish DXY. Markets have lifted positioning but there is more scope to fill:

Advertisement

With Europe and China struggling plus the latter clearly now working to sink CNY, King Dollar is still the only game in town.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.