The Australian dollar just cracked another 13 month low:

As yields are bid in:

For some bizarre reason, markets are still pricing a positive carry into Aussie yields versus the US, a patently absurd proposition. More from Coolabah Capital:

Financial markets are riddled with seemingly intractable inconsistencies right now. Arguably the best barometer of the global price of money, the US 10-year government bond yield, is still sitting at only 1.45 per cent, despite the fact that core inflation is running at more than double the Federal Reserve’s 2 per cent target for the first time in decades.

The Fed has revealed that it no longer believes this inflation shock is temporary, and it is not hard to understand why. Annual wages growth in the US has surged to over 4 per cent, its highest level since before the global financial crisis. This has been powered by the jobless rate plummeting from 14 per cent in early 2020 to just 4.6 per cent today.

At the same time, consumer inflation expectations have spiked in lock-step with elevated core inflation. The New York Fed’s survey of consumer inflation expectations over the next three-years is printing at close to 4 per cent compared to the 2.7 per cent average over the five years prior to the COVID-19 crisis. There is, therefore, some evidence of a nascent wage-price spiral that threatens the credibility of the Fed’s inflation targeting regime.

Yet this data is hard to reconcile with the level of long-term discount rates. The last time the US experienced wage growth north of 4 per cent, in 2007, the interest rate on 10-year government bonds was over 5 per cent. And we have to go back to the early 1990s to find a period in which US core inflation pierced 4 per cent. At that time, 10-year government bond yields were above 8 per cent.

There are two explanations for the disconnect between interest rates, on the one hand, and the inflation and wages data on the other, which both point to the Fed being behind the curve. The first is that the Fed’s cash rate remains around zero per cent. Accordingly, the Fed has yet to start normalising policy despite evidence that the economy is converging on full employment and substantially overshooting its inflation target. The second is that the Fed continues to buy US government bonds, artificially depressing their yields, and will not stop doing so until March next year when it completes its ‘taper’ of these purchases.

This also sheds light on another dichotomy, which is the never-ending appreciation in US equities notwithstanding the data implying that the discount rates used to value stocks need to mean-revert much higher. For the time being, equity and bond investors appear happy to bury their heads in the sand. This is exemplified by market pricing for the Fed’s terminal cash rate.

The Fed’s voting members have made it clear that they believe that the ‘neutral’ US cash rate is around 2.25-2.50 per cent, which is where the Fed’s target rate finished in its last hiking cycle in 2018. It is important to stress here that this neutral cash rate is much lower than the contractionary rate that would be required to wrest a genuine wage-price spiral back down to earth.

In 2018, US core inflation was 2.1 per cent, roughly half its current rate, and wages growth was 3.8 per cent, likewise less than its present pace. And yet financial market pricing for the Fed’s terminal cash rate has it peaking at only 1.45 per cent, which is also where the US 10-year government bond yield is trading. So despite the burgeoning inflation and wages shock, markets are gripped by the idea that the Fed will not get its cash rate back to neutral over the next few years (the terminal cash rate the market pricing is some 100 basis points below neutral). Of course, it is possible that the neutral rate is much lower than what the Fed thinks.

Interestingly, a similar dynamic played out in 2016 just before the Fed embarked on its last hiking cycle. In the second half of 2016, the market was pricing a terminal cash rate of only 1.25 per cent. Yet after a spate of hikes this had climbed to over 3 per cent in November 2018. And it was at this juncture that US equities finally started giving up the ghost, plunging 20 per cent in the final two months of 2018. Further damage to stocks was avoided by the Fed doing a 180 degree turn on its tightening cycle. (It actually started cutting rates in the second half of 2019 as core inflation decelerated to 1.5 per cent.)

In April 2021, our chief macro strategist, Kieran Davies, published research that quantified the impact of a modest 1 percentage point increase in US inflation expectations on asset prices. He found that the Fed’s cash rate typically rises by 250 basis points (in line with the Fed’s current estimate of its neutral cash rate). This is accompanied by a 150 basis point increase in the 10-year government bond yield, which would put US yields back where they peaked in 2018. Finally, equities decline by 15 per cent in real, or inflation-adjusted terms, which is what happened in 2018. Naturally, if the inflation shock is worse, the drawdowns will be larger.

With all of this in mind, market pricing for Aussie interest rates is difficult to fathom. After the Reserve Bank of Australia suddenly discarded both its 2024 forward guidance and its 3-year yield curve targeting policy in November, domestic interest rates spiked, forcing banks to relentlessly lift their 1-year to 5-year borrowing rates. (CBA and NAB have increased their fixed home loan rates three times in the last six weeks.)

Two months ago, the 3-year ‘swap’ rate was only 0.4 per cent. (Banks, companies, and households borrow at a margin above this benchmark when taking out fixed-rate loans.) Since the RBA dumped its policies, the 3-year swap rate has leapt 100 basis points to 1.4 per cent, imposing de facto rate hikes on fixed-rate borrowers in what has been a multi-sigma, value-at-risk event for interest rate markets. (The Aussie Composite Bond Index lost 3.6 per cent in October alone.)

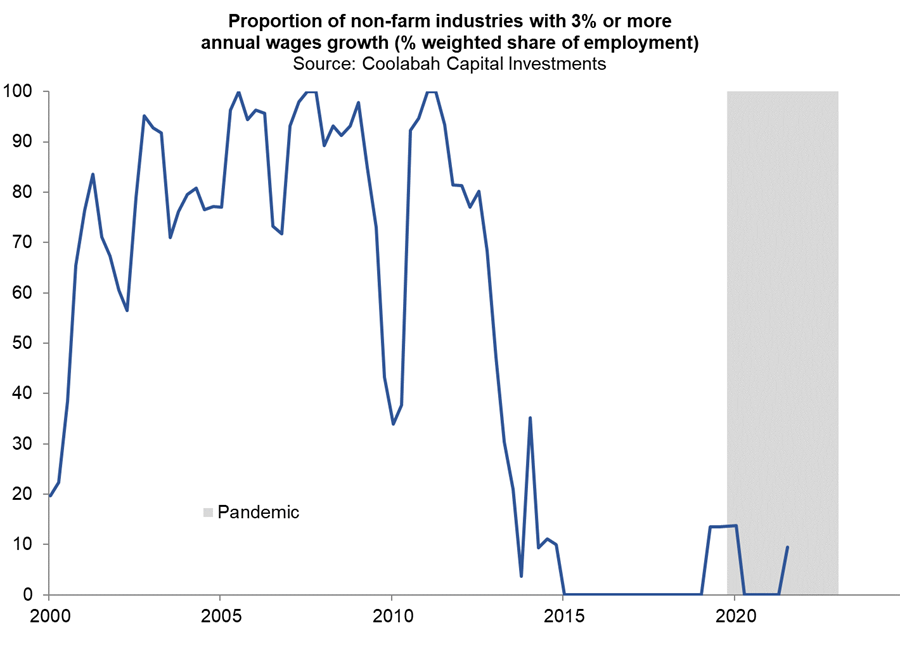

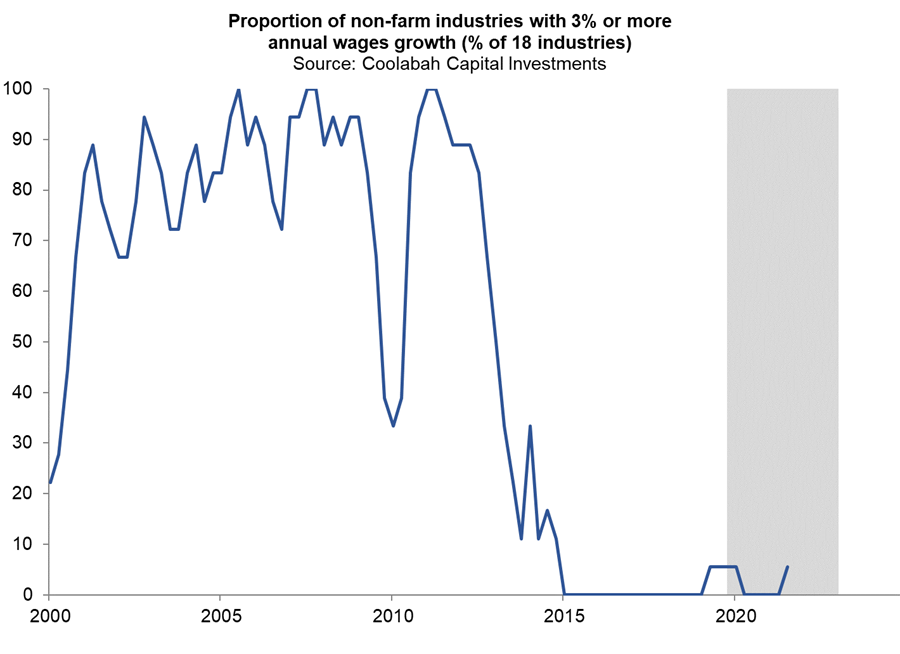

Yet in contrast to the US, Australia has neither a wages nor inflation outbreak. In fact, just one of our 18 different industry sectors (professional services) is recording annual wages growth above the 3 per cent threshold the RBA says is necessary to get core inflation sustainably back into its target 2-3 per cent band (and only two others—construction and hospitality—have reported wages growth above 2.5 per cent).

Wages and core inflation in Australia have been expanding at a benign pace a touch above 2 per cent, about half the rate observed in the US. The incongruity is that the market is pricing a terminal RBA cash rate around 2 per cent, some 50 basis points above where investors think the Fed’s cash rate will finish. By the end of 2022, markets are handicapping a Fed cash rate of only 75 basis points, which is bizarrely below the 90 basis point expectation for the RBA’s cash rate next year. It is as if markets have switched-around the wages and inflation data in Australia and the US. This is also supported by the fact that the Aussie 10-year government bond yield has been trading 20-30 basis points above its US equivalent.

Many interest rate strategists claim the RBA is to blame for suddenly jettisoning both its forward guidance and the yield curve targeting policy, which blew-up investors who had allocated capital on the presumption Governor Lowe would stick to his forecast that the cash rate would not increase until after 2024.

The irony here is that the event that precipitated this shock—one decent quarterly core inflation print sliding into the RBA’s target band—was quickly superseded a few weeks later by wages data that was much weaker than the market expected. If the wages data had preceded the inflation numbers, the RBA would probably have persisted with its prevailing policy.

Despite the turmoil in interest rate markets, sluggish domestic price pressures reinforced by the reopenining of borders (and a skilled migration boom) lend a lot of weight to Lowe’s incrementalist, and stubbornly dovish, disposition, which has him moving very slowly along the road to one day possibly normalising monetary policy. This will conspicuously lag the Federal Reserve and could be further delayed by the recent spike in swap rates, artificially tightening financial conditions years ahead of the RBA’s central case.

And this is before the terms of trade and immigration shocks return.

The only thing that could shift this view is closed borders from OMICRON and even then it would be by increments.

Otherwise the carry trade is going to reverse and add even more pressure to the AUD.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.