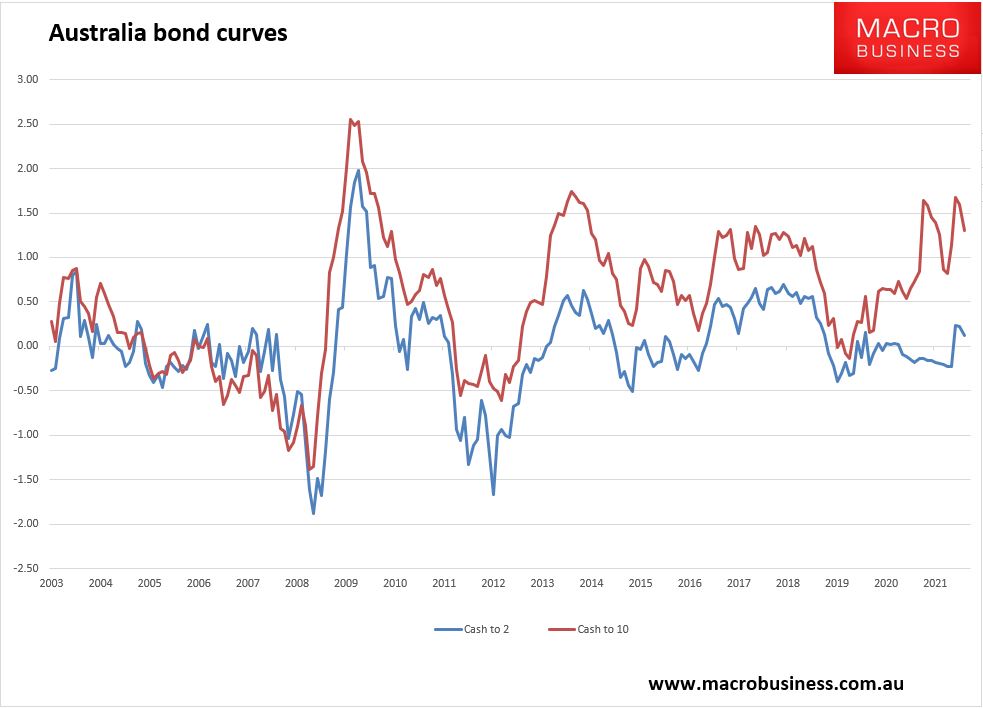

And just like that, Aussie bonds are back with big gains last week and yields looking decidedly toppy:

The curve is flattening fast as growth and inflation prospects fade globally on OMICRON and Fed tightening:

Advertisement

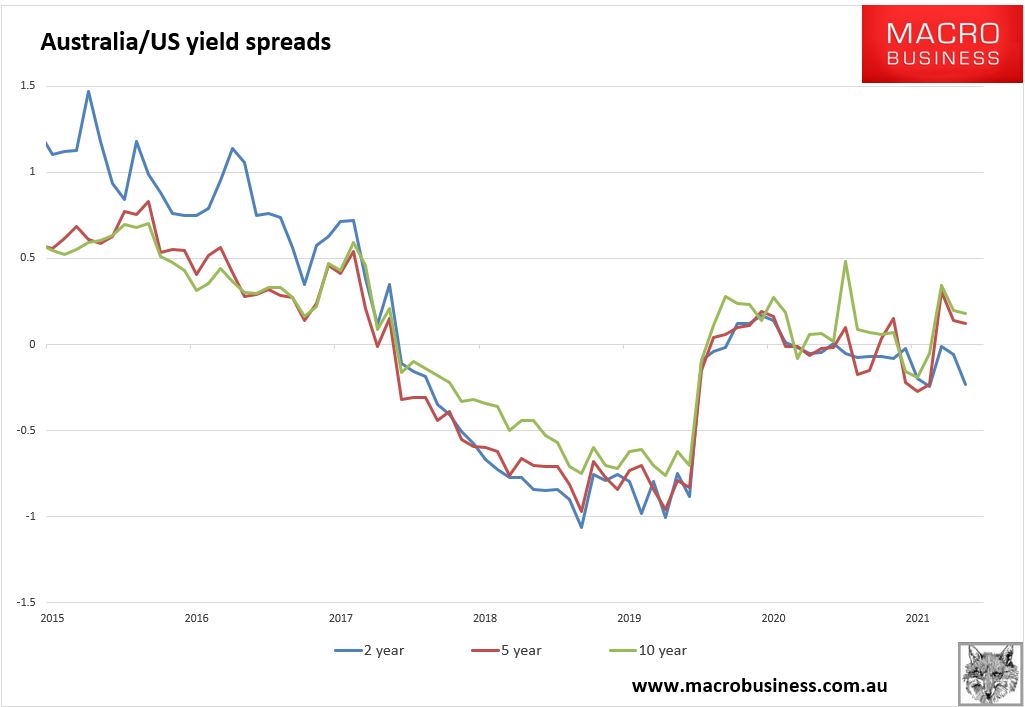

The short-end of the curve has flipped to a negative carry with the US: