Last week, Dr Cameron Murray – author of the Book Game of Mates – gave testimony to the parliamentary inquiry into housing affordability whereby he completely demolished the Coalition’s supply-side thesis.

Dr Murray was asked via a question on notice to provide evidence to the inquiry that developers manipulate the land market to ration supply and maximise their profits, which he has provided below:

What developers say and do

I was asked on notice to provide sources of evidence where developers had explained publicly that they choose not to flood the market with housing even if they can.

A first puzzle is that in their annual reports, listed companies like Stockland and Lendlease do not report that planning is inhibiting their ability to produce housing. In fact, in their 2021 annual report, Lendlease blamed themselves for not meeting the surge in market demand:

“The Australian Communities business has not been positioned to take full advantage of the favourable market environment over the last year. We expect sales to accelerate in FY22, boosted by the commencement of new projects. However, with the typical lag between sales and subsequent settlements, volumes are expected to remain below the annual settlement target of 3,000-4,000 lots. (p 16) It is interesting to see them note that their own choices about positioning their projects were to blame for them not meeting their own conservative sales/settlement targets”.

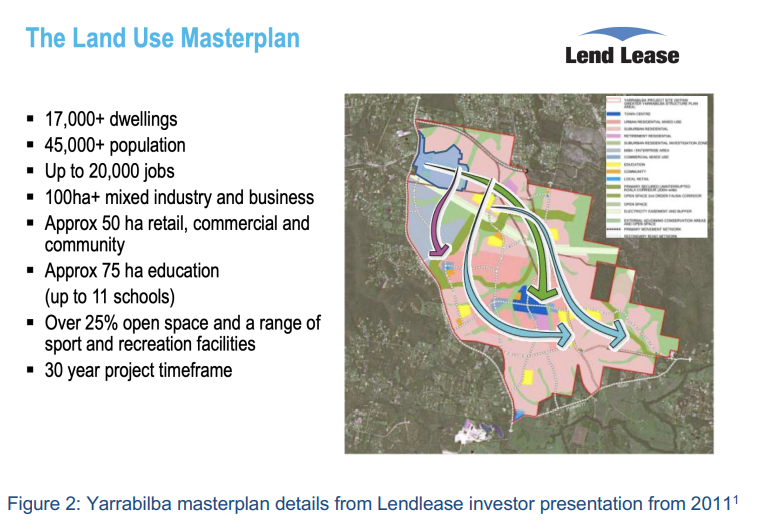

In 2011 Lendlease gained approval for a major master-planned subdivision at Yarrabilba in South East Queensland. At the time of approval there was much public discussion about a housing shortage and how this approval would help.

Now, ten years later, the project remains in the first stage only. Lendlease has held the bulk of the land vacant for a decade when these other stages could have been developed in parallel (by themselves of sold to another developer) rather than in sequence. Indeed, as they explain in Figure 2, they expect the project to last 30 years. Why not 20 years? Or 10 years?

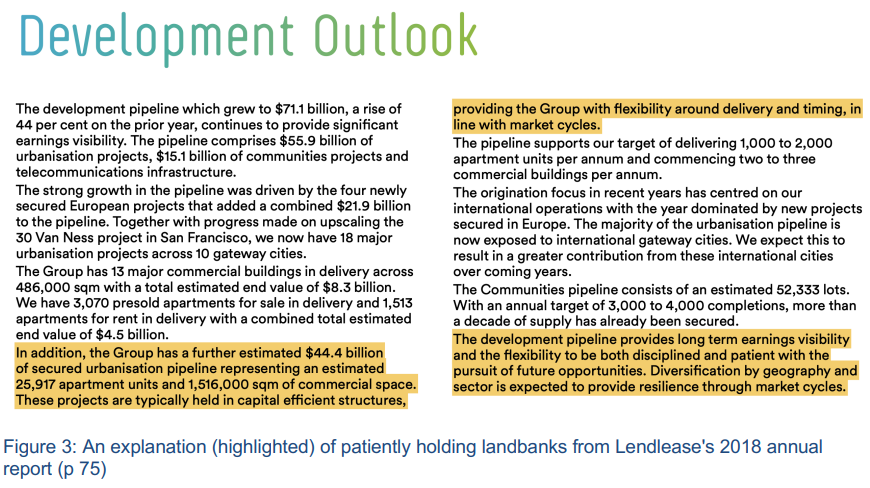

Lendlease in their 2018 annual report noted that they are holding plenty of developable assets in “capital efficient structures” so that have “flexibility around delivery and timing, in line with market cycles”. They said they could be “disciplined and patient with the pursuit of future opportunities”. This does not sound a business that is developing as fast as possible within planning constraints.

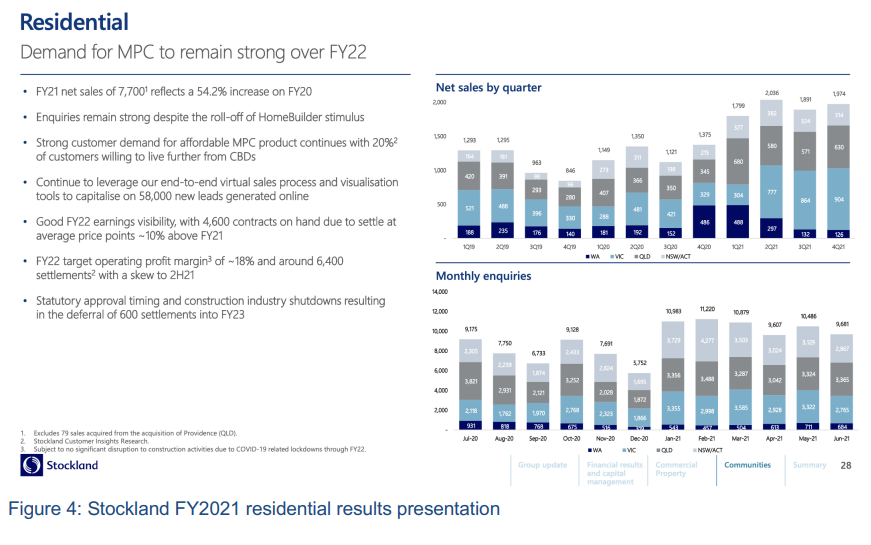

Stockland reported that their sales increased 54.2% in FY2021 (up 75% since 2019). How is that possible if planning is constraining housing supply? If the demand was there in 2019, could they have matched their 2020 sales? Or could they have increased sales by reducing prices?

They also note that they raised prices by 10% on average for their residential lots. Why? Are prices not cost-driven, as they claim? Why not increase the rate of sales rather than increase the prices? Doesn’t it make more money to do that?

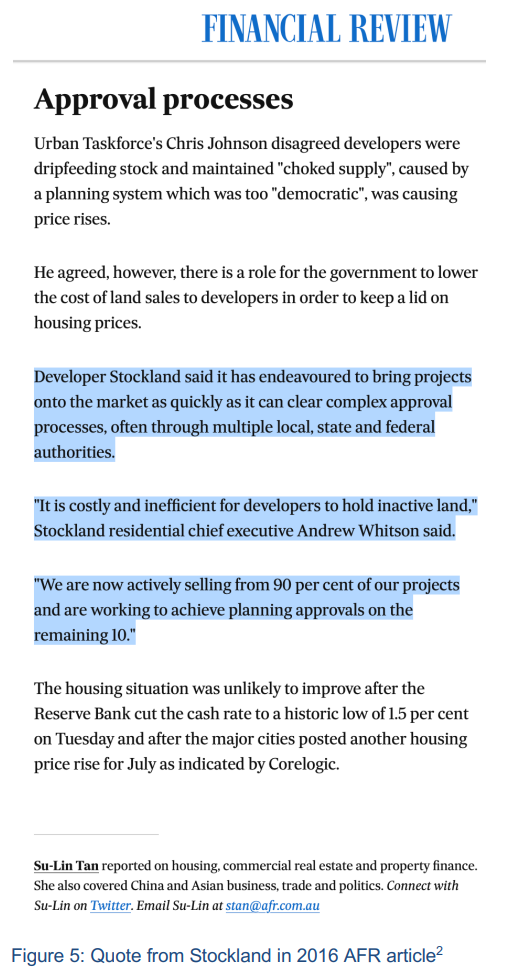

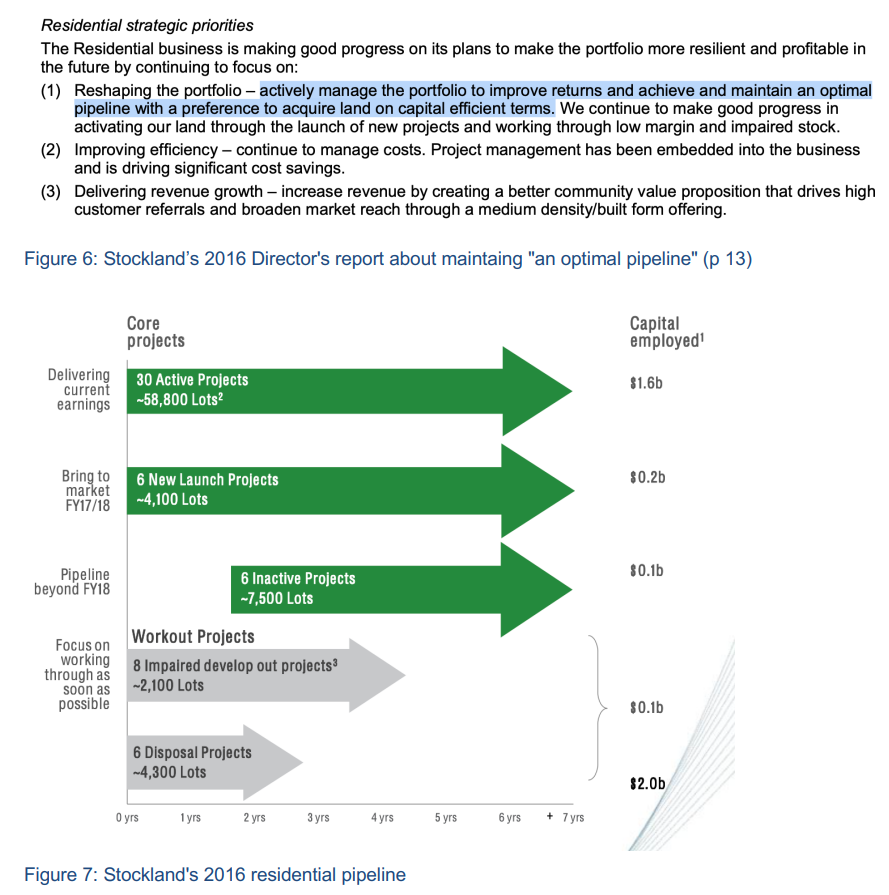

In 2016 Andrew Whitson, CEO of Stockland Communities, told journalist Su-Lin Tan that is it “costly and inefficient to hold inactive land”. In that same year, the Director’s report noted that they would “maintain an optimal pipeline” and “actively manage the portfolio to improve returns” (see Figure 6) This sounds like their landbank is actually not costly to hold, but a key part of their asset portfolio. Indeed, though it was noted that 90% of projects were “active”, these projects are estimated to produce 58,800 housing lots, yet they were selling only 6,000 per year at the time (see Figure 7). That would take 10 years to sell. If it were truly costly to hold so much land, they could sell faster or sell parts of projects to other developers and reduce this massive landbank.

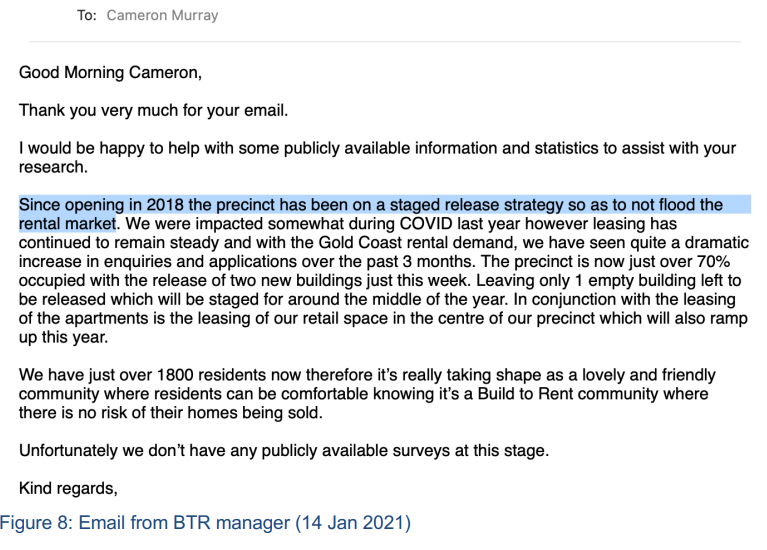

I also gave evidence to the inquiry that build-to-rent (BTR) property managers also have the same incentives to regulate the rate at which they rent out dwellings. The Smith Collective on the Gold Coast is Australia’s first major BTR project and was the former Commonwealth games athlete’s village. The project has 1,251 one-, two- and three-bedroom dwellings, all of which were completed prior to the 2018 Commonwealth Games.

When I enquired about the project progress in January 2021, I was provided the following response (Figure 8), which noted how the project was on a staged releases to avoid flooding the rental market.

During the 2019-20 period when this project had hundreds of completed dwellings sitting unoccupied, the rental vacancy rate3 in the regions was between 2 % and 3% and has since fallen to below 1%.

Questions for developers

I was also asked on notice to suggest developers to bring as witnesses before the inquiry and what questions to ask to determine whether they limit the rate they develop based on market conditions or planning regulations.

People who have insights into the question of market limits to developer would include the heads of the communities or residential divisions of major listed Australian housing developers like Stockland, Lendlease, PEET, Mirvac, Frasers, and private developers like Meriton. Key personnel from JLL who manage the Smith Collective BTR project would be useful.

Questions to put to them would centre on:

1. If a new competitor established themselves besides your major residential projects and sold similar dwellings for 25% less than what you sell them for, would that be good or bad for your business financially? Good, or bad?

2. Yet is it not your argument, or at least that of many property lobby groups, is that rezoning will lead to lower housing prices, and the mechanism will be through more competition from cheaper competitors?

3. Why do you target such small rates of housing completion?

4. Would you sell faster if you had an inactive project rezoned?

5. Do you think that rezoning in Australia will lead to dwellings prices more than 20% lower than they are now?

6. If holding big landbanks is costly, when demand falls, why don’t you reduce prices sufficiently to keep the sales rate up to its previous level?

7. How much are your landbanks worth as undeveloped assets?

8. If dwelling prices fell 20%, how much would that affect the value of you balance sheet?

9. Are prices set by input costs, or by the market? I.e. Do you increase prices when the market rises, regardless of whether you had additional costs? (prices seem unrelated to costs?)

The hilarious thing is that the Morrison Government’s fake housing affordability inquiry was designed as a sop to its developer mates as well as to shift blame to state governments, which control planning processes.

Advertisement

The upside is that it will likely end up exposing the supply-side and restrictive planning argument as being bullshit, in part thanks to Dr Cameron Murray’s testimony.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.