Credit Suisse again today:

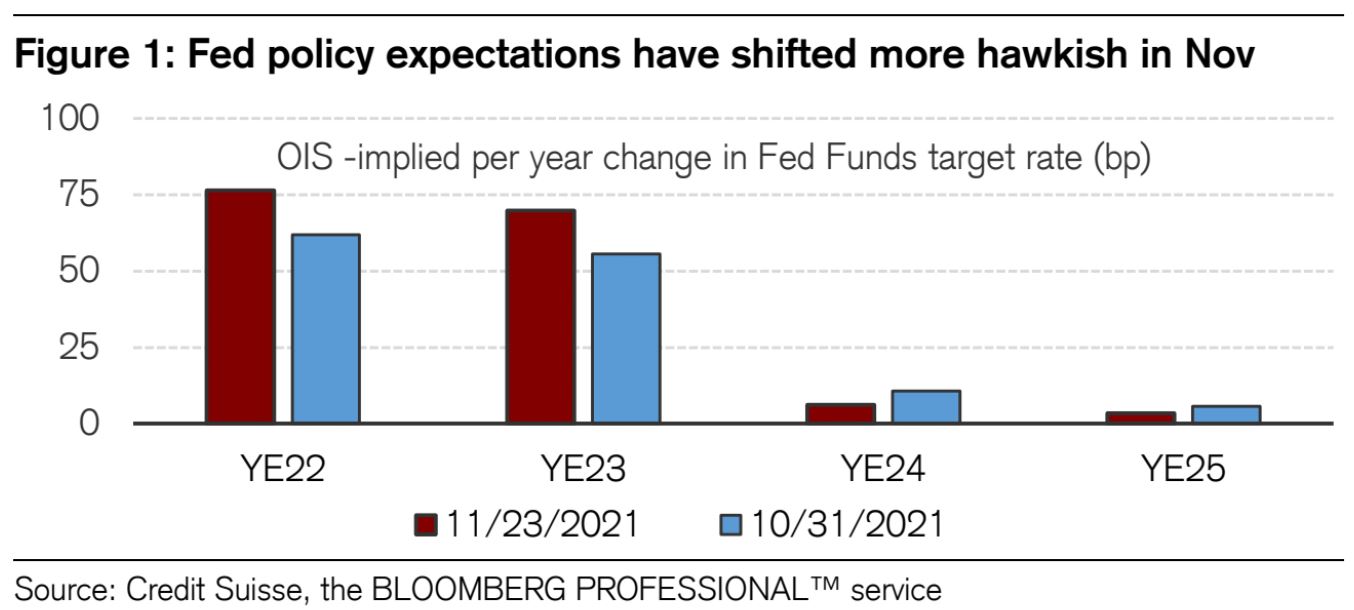

Our expectation for ongoing USD gains remains intact, and becoming broader based. Last week, several Fed officials suggested that the Fed could potentially speed up the pace of asset purchase tapering beyond what is currently planned. On top of this, President Biden’s decision to re-nominate Jerome Powell as Fed Chair removed the most likely source of near-term correction risk for the greenback. In this context, by yesterday morning the US rates complex had re-priced yet again to factor in 75bp of rate hikes in 2022 starting in Q2, and a further 75bp over the course of 2023. But with “terminal rate” rate expectations still subdued around1.75%, there is arguably still more work to be done.

For this reason, we have had bullish USD targets against EUR (where we target EURUSD 1.1150) and JPY (where we target USDJPY 118) for some time already. But the outlook for the pro-cyclical and especially EM space is still darkening further too. The spectacular rise of USDTRY continues unabated: from a general top-down perspective, the fact that one of the larger countries in the EM space is exhibiting this type of price action is a reminder that the space always poses hard-to-manage political risk and the possibility of economic unorthodoxy.