Credit Suisse with the note:

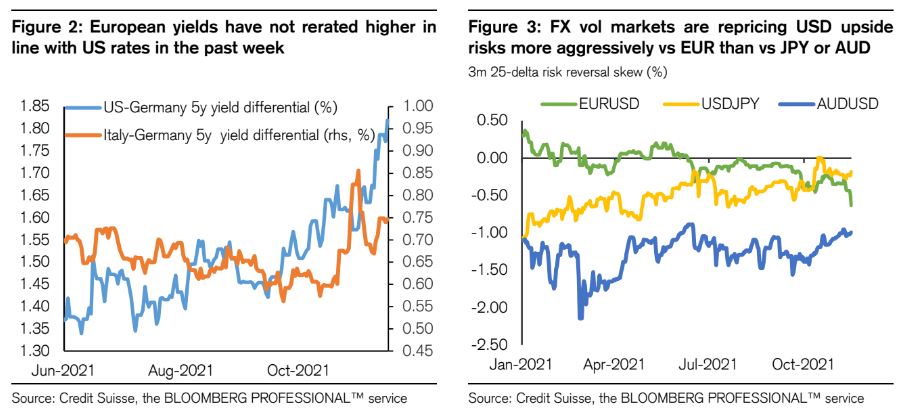

The euro area story is different enough to present challenges for EUR. A simple look at European equities would suggest that there isn’t much to worry about, with SX5E pushing ever upwards to new 2021 highs. Despite this, it seems markets feel that if inflation is truly likely to be transitory anywhere, the euro area is near the top of the global list of contenders. Add to this the ECB’s unflinching dovishness and explicit preference for EUR weakness, and the single currency is left with little to recommend for it–even if the same reasons are pushing European equities higher. Indeed the weak EUR becomes itself an ingredient supporting European asset prices in this context. The market has already done much to unwind the jump higher in euro area short-term rates seen at the start of November, with ERZ2 well above its recent lows even as L Z2 and EDZ2 are near or through previous lows. But arguably still more can be undone on this front. And asFigure3shows, the market is busy marking up the risks of a sharper EUR decline against the USD much more actively than it is doing for other G10 counterparts, whether they be defensive currencies like JPY or pro-cyclical ones like AUD.

It’s also the case that the marginal negative risk factors that are brewing seem concentrated on the European front. These include: