Pantheon Economics with the not:

Chinese Industry Avoids Calamity, but Q4 Looks Set for Weakness

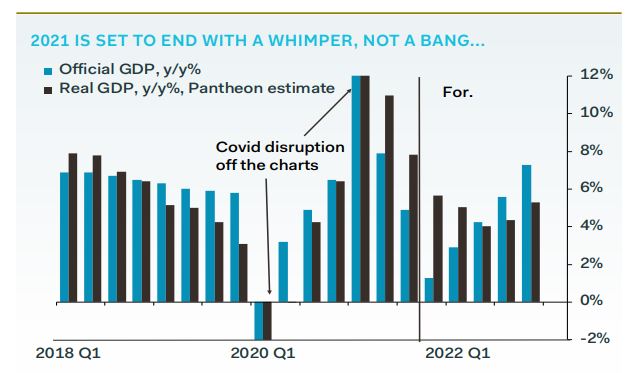

China’s economy is still in the doldrums, but a faint breeze is tugging at the sail. The horizon remains stormy and dark, however, and the currents are treacherous. Fixed asset investment slowed further in October, to 6.1% year-over-year, from 7.3%, driven by the ongoing calamity in the property sector. But industrial production offered better news, accelerating to 3.5% year-over-year growth in October, from 3.1% in September, shrugging off factory closures and energy shortages. Still, industrial activity growth remains well below its typical run rate. Retail sales also seem to offer hope, climbing to 4.9% growth year-over-year, from 4.4% in September, but we think the data flatter to deceive. All told, we are a bit more optimistic about the outlook, but the bar was low.