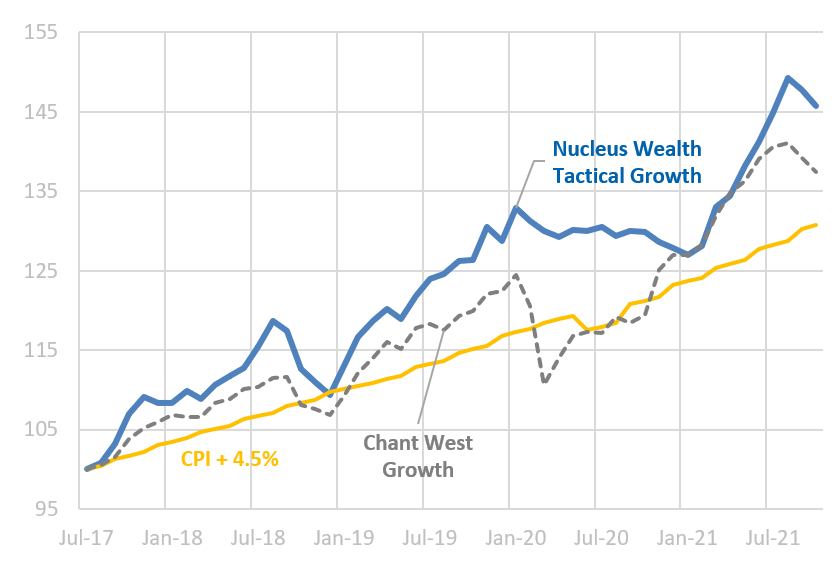

October was not our month. Stock markets pulled back but rebounded mid-month to end in the black on the back of encouraging corporate earnings and an easing of fears around China’s property sector. Our core portfolios underperformed as the market took a wait-and-see approach on our over-weight travel stocks that were due to report in early November, and who subsequently produced strong positive earnings surprises. Bond yields rose. We took advantage of these price movements to increase our weights, and most of these trends have reversed in November.

We expect international equities to provide some protection from a growth slowdown. While the Aussie dollar is likely to rise if the energy crisis worsens, it is more likely to fall over the medium term. This will hedge the downside under the worst scenarios while still providing some upside in the better ones.

Inflation scenarios

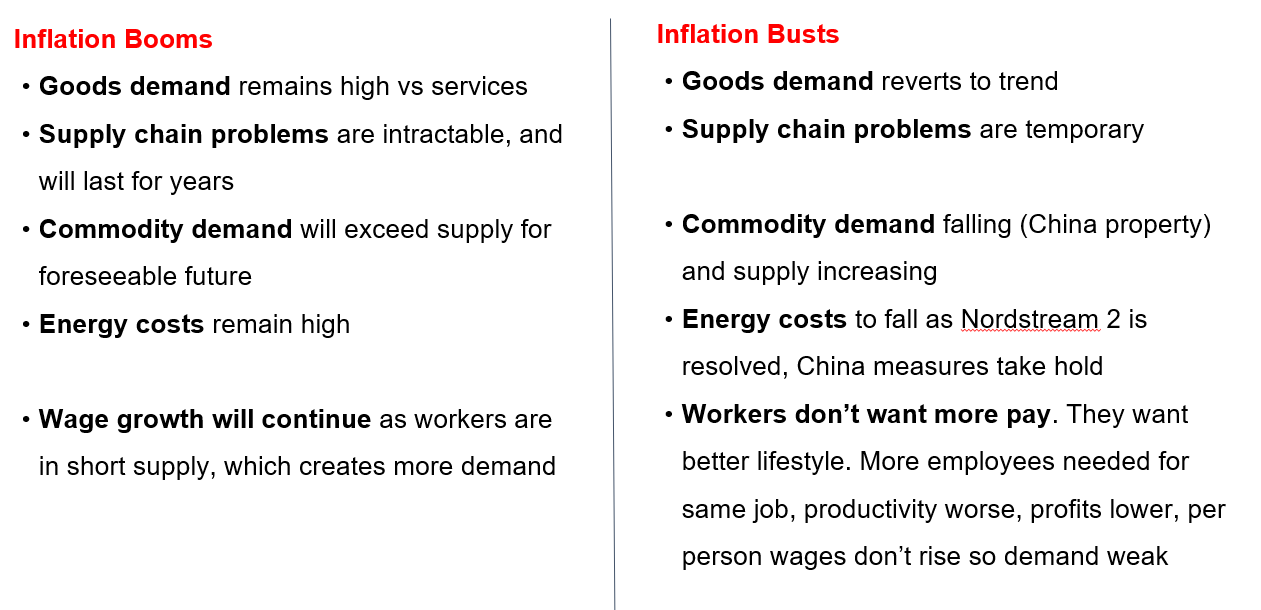

Our view is that inflation has been driven by

- changes in demand due to direct government stimulus and lose monetary policy

- changes in demand patterns (more goods, fewer services)

- supply chain disruptions/capacity issues

- Commodity price inflation hedges

The first driver, stimulus, has largely run its course. There may be further stimulus through infrastructure, but this is still some time away. The Federal Reserve has begun a tightening cycle.

This leaves the following as the key determinants to growth:

Goods demand

The first inflation question comes down to demand. Will it return to a more normal pattern, or are we in a new paradigm:

It would seem that as economies reopen that old spending patterns will return: more services, fewer goods. However, it does remain a possibility that this trend will take some time to revert to a more normal level. Particularly as COVID flares up in the Northern Hemisphere winter.

In my view, demand for goods is unlikely to grow faster than the trend from here. It is more likely to fall or, at best, rise modestly while services demand catches up.

For inflation, what matters is about the change in demand.

Supply Chains

The supply chain issues have certainly grown to higher levels than expected. Some now have the view that supply chain issues are intractable and will last for years. Others are of the view that the problems are temporary, and more like a traffic jam. I’m still in the second camp, but I do note that the next few weeks will be an important test of this view.

Shipping costs are one of the main indicators of supply chain problems. If we are right in our assessment, part of the reason for the shipping jam is the combination of elevated goods demand meeting typical Christmas demand. The Christmas demand will lessen over the next few weeks and so we should continue to see shipping costs declining, perhaps even precipitously:

In our view, transport prices have spiked higher as high-value goods try to pay to get to the front. But it isn’t a “forever” rise in prices. Major international transport providers reported 3Q earnings last month with a general theme that volumes were down while prices skyrocketed. Inflation needs prices to keep rising year after year. The current set-up is for high prices until the “traffic jam” clears. At which stage prices will quickly revert – and potentially go lower through productivity improvements spurred on by the current high prices.

What could clear the traffic jam? Reopening economies will lead consumers back to services, reducing demand for goods. Power-induced shutdowns in China will unblock the other end. The end of the Christmas rush will also help. Beyond that it is difficult to tell – traffic jams are notoriously difficult to predict the duration of.

Commodity Demand

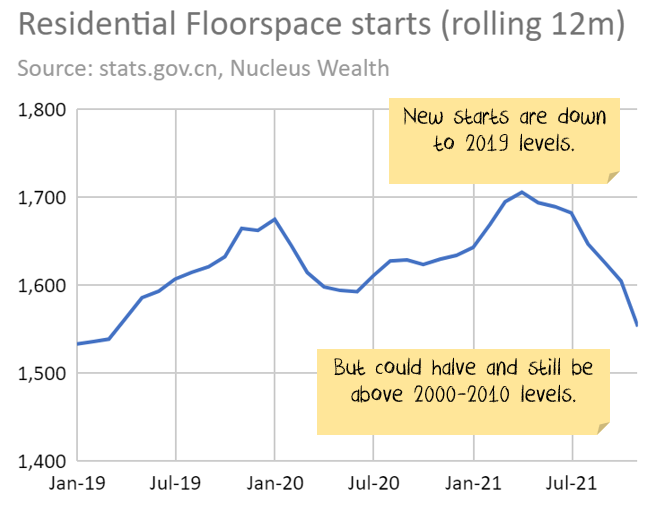

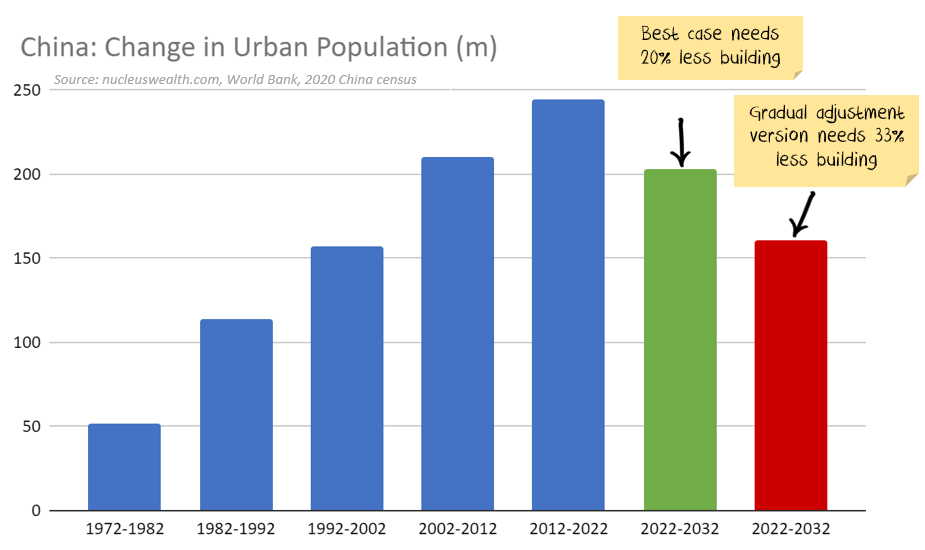

China is the world’s largest consumer of commodities. The housing market in China is the largest consumer in China. And it is slowing rapidly.

Chinese developers, which are still larger than the rest of the world combined, have run into trouble. Evergrande gets most of the headings, but there are dozens of smaller developers in a similar predicament.

Headlines over the last few days, and a jump in iron ore prices, suggest that the crackdown has ended. The detail says the opposite. The Financial Times sums it up well:

Chinese regulators have eased pressure on property developers by loosening credit controls and allowing more bond issuance in recent weeks in an effort to prevent the sector from collapsing. But analysts and government advisers say the measures do not represent a retreat from President Xi Jinping’s crackdown on the sector.

…“There are still systemic risks posed by a real estate meltdown to the broader economy,” said Deng Haozhi, a Guangzhou-based property analyst. “It is up to regulators to avoid that scenario.”

A Beijing-based policy adviser said: “All of our previous attempts to regulate the real estate market have failed because we exited halfway through overhauls. This time the central government is determined to stick to the plan.”

Metals are the last places to be invested if Chinese property construction slows.

Energy Costs

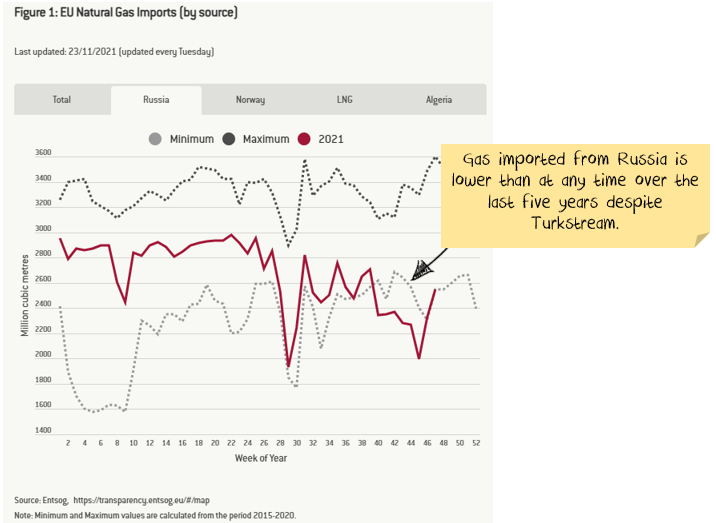

European energy costs are still really high. Low wind output didn’t help, but a more important factor has been the plunge in Russian gas:

Maybe there are perfectly innocent explanations. Maybe the lower volumes are there to “incentivise” Germany to sign off on the recently build Nord Stream 2 pipeline.

Basically, there are four major pipelines from Russia to Europe and a fifth has been built but not yet approved. One of those pipelines (Turkstream) only started 18 months ago.

To put it another way, gas imports from Russia are lower than at any other time over the last five years, despite there being more capacity now than ever.

Which suggests the situation is cyclical, not structural. Having said that, weather could make the situation worse. A cold winter, disruptions to major coal suppliers in Indonesia or Australia and energy prices could rocket even higher. Predicting lower energy prices is easy. Predicting the timing is the difficult part.

Net effect

Wall St brokers are largely pitching investors the inflation story. You make much better commissions convincing investors to blow the bubble bigger. They will seamlessly and shamelessly switch to the second story when the currently predicted five years of inflation morphs into five months of inflation.

I’m more comfortable with a lower inflation story. Braver traders might want to surf the price waves driven by narrative. But iron ore and lumber have recently shown us that prices can halve in a matter of weeks. I prefer to bet on a lower tide.

We are reaching an inflection point. Our portfolios are conservatively positioned, risks are high. Unfortunately, once again we are waiting for government responses to determine our investment outlook. Our expectation is that China will try to smooth the property slowdown, but won’t reverse course in the short term.

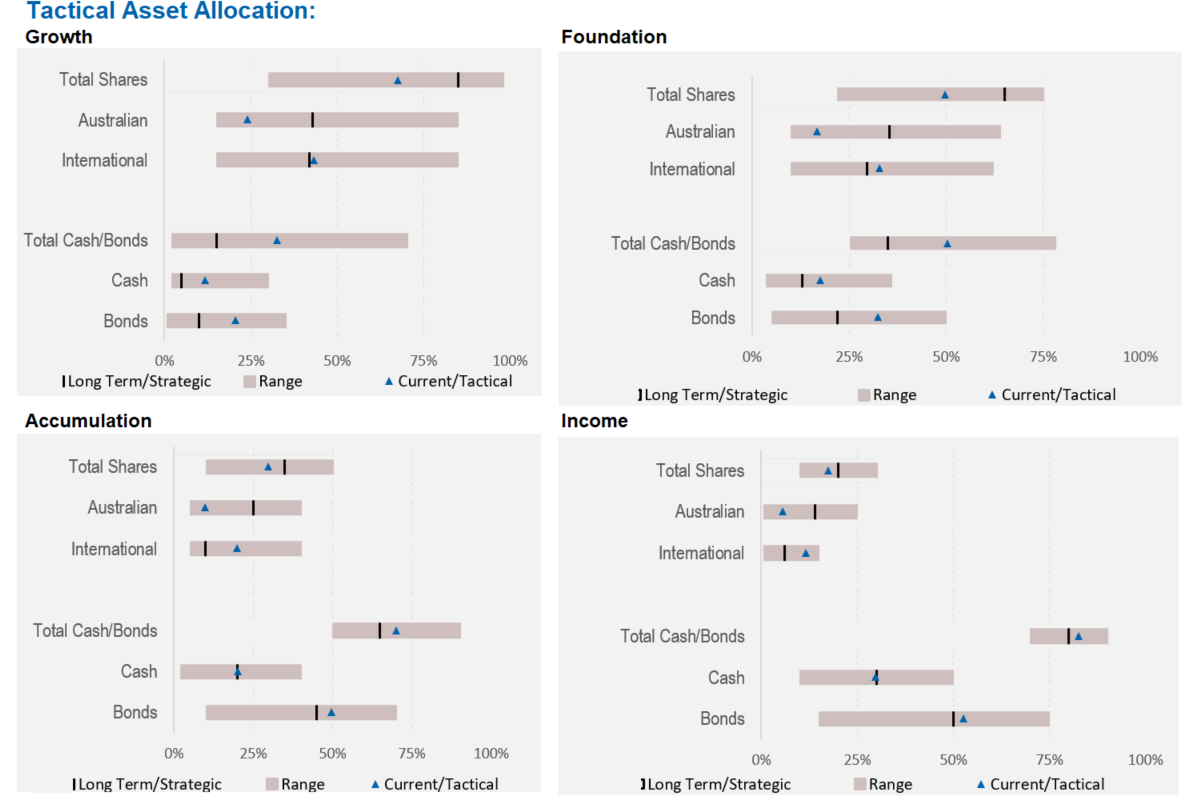

Asset allocation

Stock markets are expensive. Debt levels are extremely high. Government/central bank support continues but is slowing. Earnings growth had been really strong but has come to a halt.

Markets are supported to a great degree by central banks and governments. Policy error is every investor’s number one risk.

But, any number of other factors could force this off course and see unexpected inflation. Mutations could disrupt supply chains again. Chinese/developed world tensions might rise further, leading to more tariffs. Or, China might reverse its tightening on property sectors. Biden may get through additional stimulus, driving increases to minimum wages.

We are significantly underweight Australian shares, with the view that the Australian market will be the one most affected by a slowdown in China:

Australian equities have been a good source of investment performance in recent months. We switched out of them and into international equities and cash. For the last few months, the timing has been good. Not so during October where markets have shrugged off the China issues. We have largely built the defensive side of the portfolio up, changing out of value winners like resources, banks and cyclical industrials.

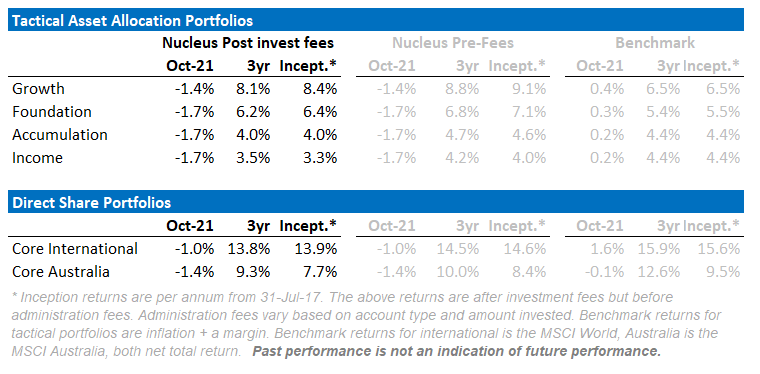

Performance Detail

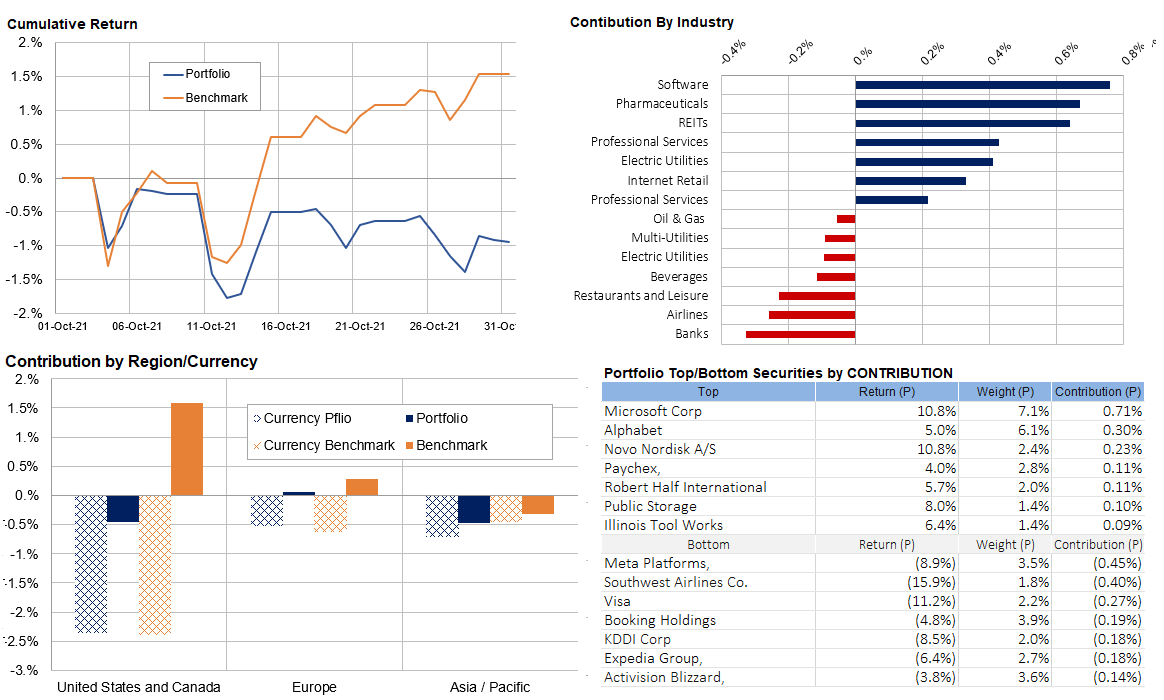

Core International Performance

October was a down month for us as our travel stocks were sold off on earnings worries which proved unfounded in their November reports. Over the month there was a turnaround with Risk-on and technology and pharmaceuticals clawing back September pullbacks. Regionally our US stocks underperformed with Europe the only positive contributor.

Currency headwinds harmed the portfolio as the AUD had a strong month rising 3.7% vs USD at one point. Over the month we lightened our Meta Platform (Facebook) and took on some Energy exposure to hedge any crisis. Both positioned reverse in November after price movements.

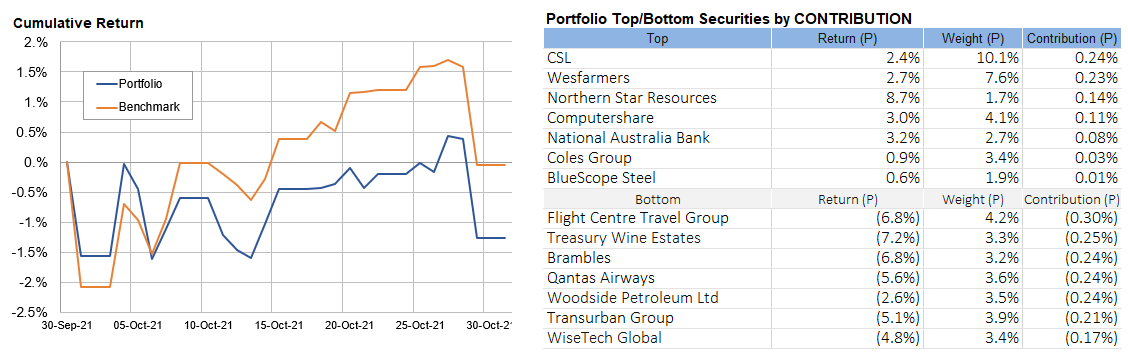

Core Australia Performance

The Core Australian portfolio underperformed the index in October as the market rotated away from travel names and took profits on growth stocks. In October we exited and took profits on our BlueScope Steel holding.

We are still of the view that the global economy is entering a mid-cycle slowdown with the US leading and China lagging which makes us cautious on highly valued risk assets.

But, as I have said many times, and will no doubt continue to say:

We are not in a normal market. We are reliant on government and central bank support. So policy error remains the number one risk.

Both upside and down.

Damien Klassen is Head of Investments at Nucleus Wealth.

Follow @DamienKlassen on Twitter or Linked In

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd – AFSL 515796.