Is Chinese property turning Japanese? The answer is “yes”. But there will be differences. Goldman with the note:

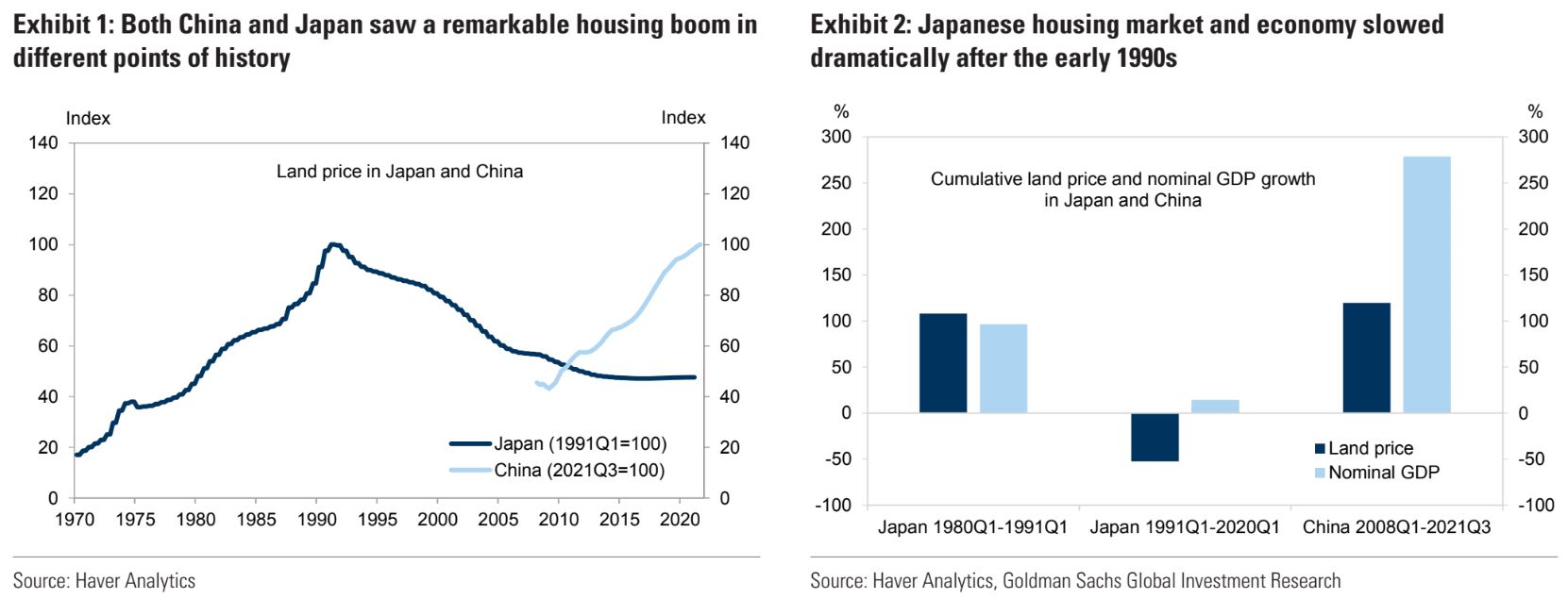

The Chinese property market experienced a dramatic boom during the 2010s, similar to the housing boom in Japan in the second half of 1980s. In Japan, land prices halved and economic growth ground to a halt during the three decades after the 1991 peak. Given the recent deleveraging policies and significant slowdown in the Chinese property market, we compare the two countries 30 years apart and draw lessons from Japan’s experience for China.

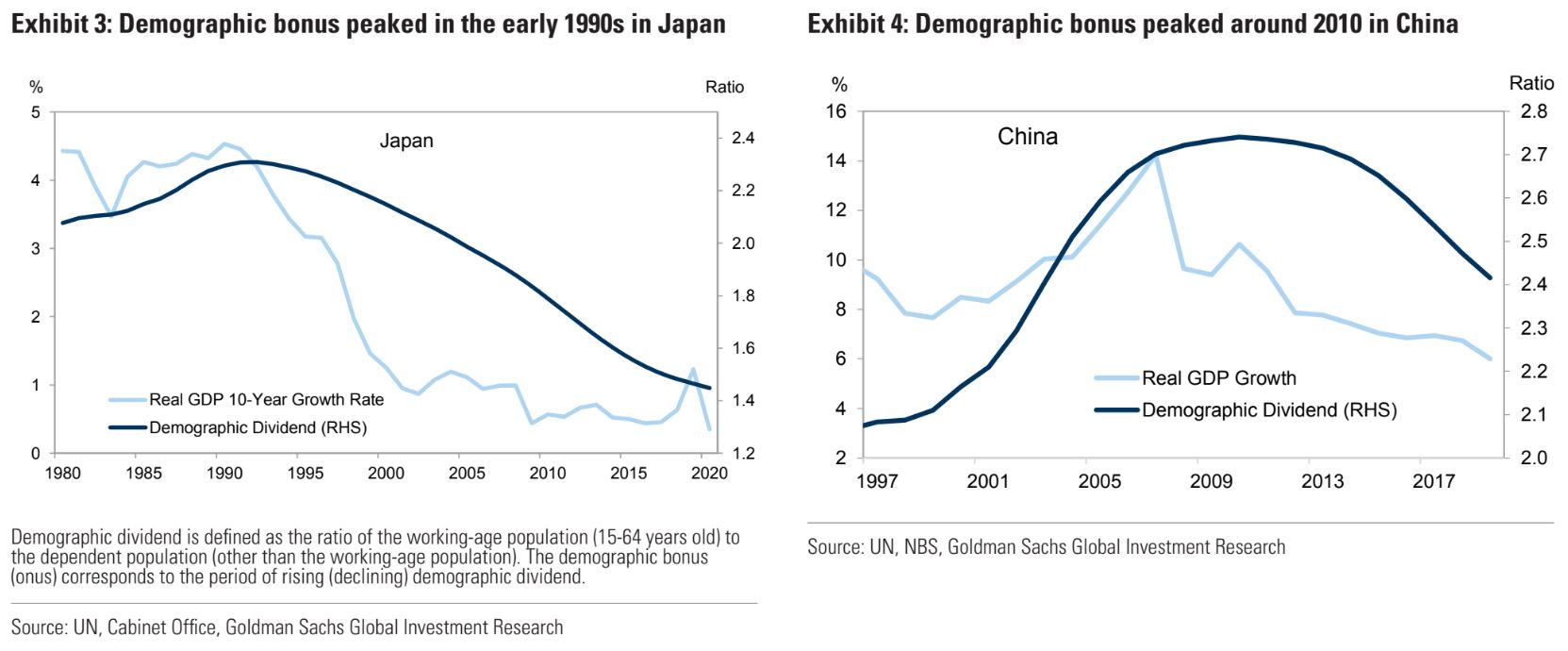

We highlight two major similarities between China and Japan. The first is demographics. Demographic “bonus” turned into demographic “onus” in the early 1990s for Japan, and the working-age to non-working age population ratio similarly peaked in China around 2010. Slower population growth not only means less demand for residential property but also could exacerbate the downturn after significant negative shocks. Second, a series of tightening policies were implemented in the property market around 1990 in Japan and over the past year in China. Multiple policies reinforce each other, amply the effects on the market, and can generate unintended overtightening.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.