TS Lombard with the note:

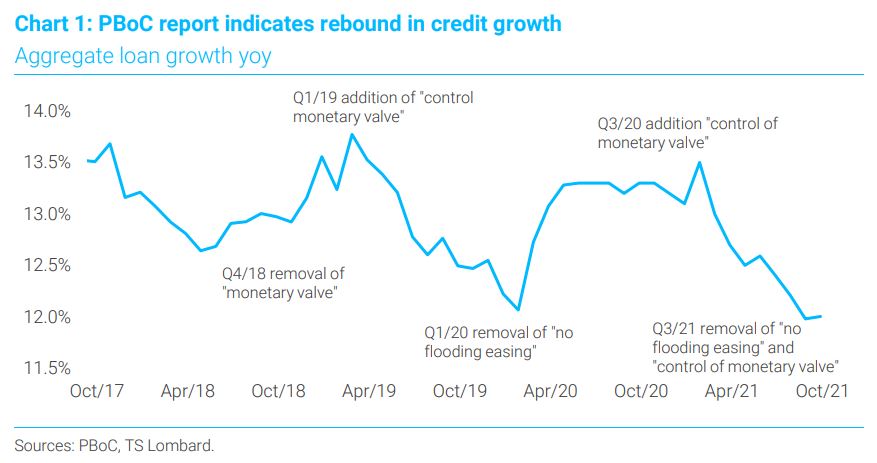

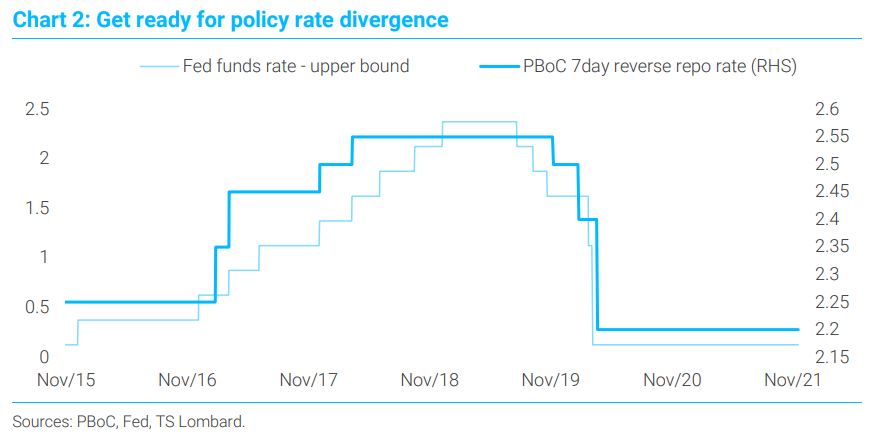

For the PBoC, growth and financial stability concerns trump inflation and worries about monetary policy divergence. The bank’s recently released Q3 monetary policy report indicates a dovish shift and confirms our expectations of sustained policy support for the economy, particularly for the property sector. A 50 bps RRR cut is likely in the next six months. Easier credit for real estate will continue to roll out and the nadir in developer funding is likely passing, but the sector will remain a large drag on activity in 2022 and for years to come. The dovish turn has surprised markets: CGB 10-year yields have dropped sharply in the past week to nudge closer towards our yearend target of 2.9. Expected growth (China activity will bottom out in Q1/22 but rebound to just 4.7% yoy in 2022 as a whole) and monetary policy divergence (PBoC stays dovish even as the Fed tapers and hikes once next year) add conviction to our H2/22 RMB depreciation call.

In each quarterly monetary policy report the PBoC includes special-interest sections, which give us an idea of policymakers’ focus areas. The Q3/21 report devoted three pages to “Monetary Policy Adjustments in Developed Economies”. The bank’s analysis is as follows: “A prudent monetary stance should be the mainstay of policy, with a focus on China and greater autonomy (from the Fed/DM central banks), and the strength and pace of the policy should be managed in accordance with the domestic economic situation and price trends.”