There are five reasons why the Chinese economy is going to crash over 2022.

China Crash 2022 point one: developer credit crunch

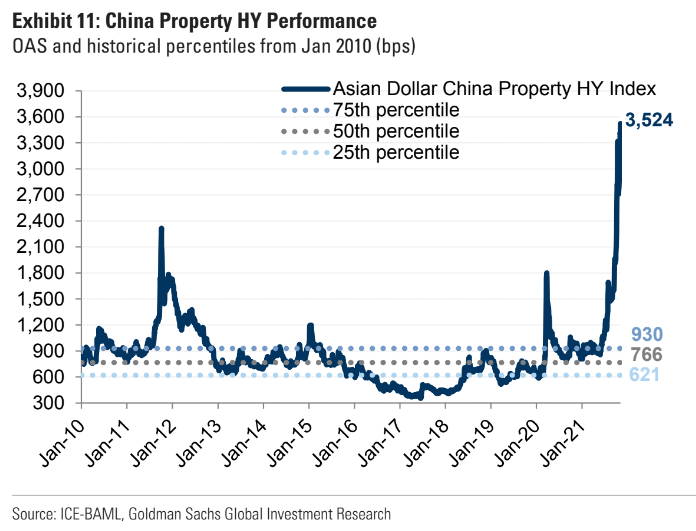

China’s “three red lines” policy aimed at deleveraging property developers has frozen the dollar-bond funding market and it continues to get colder. Goldman:

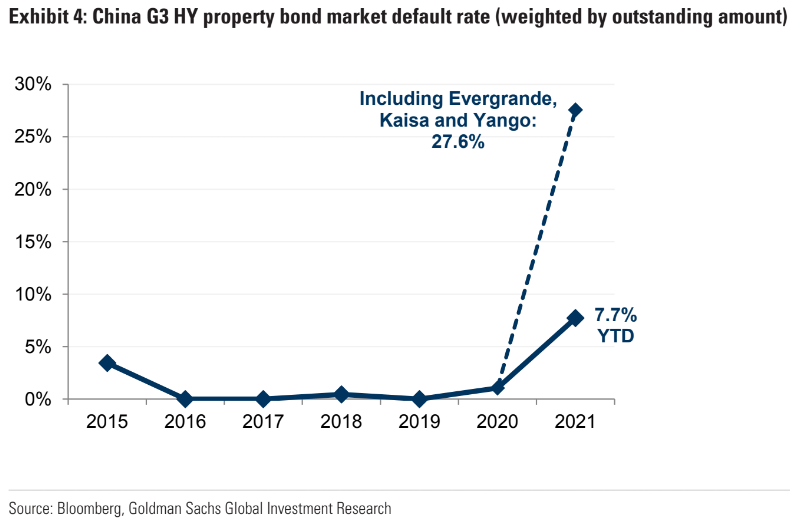

Concerns regarding the China property sector continued to mount, as the lack of meaningful policy easing measures meant focus was on idiosyncratic events. To us, unless we see clearer evidence of improved operating environment in the physical property market and noticeably easier credit conditions, the market will likely continue to worry about tail risk, especially with heavy RMB bond maturities in December this year and heavy USD bond maturities in January next year. Whilst policy stance has eased since late September, it is unclear whether the pace of relaxation is sufficient to avert a large pick-up in credit stresses in the next few months. Therefore, volatility will likely stay elevated, reinforcing our view that investors should concentrate on low beta China property credits. A number of China properties companies presented at the Goldman Sachs China Conference over the past week. They indicated that, whilst policy stance has relaxed, any improvement in the property market is likely to be gradual. To us, this gradual pace of easing means that default rates could pick up substantially. We estimate that, so far this year, the China property HY default rate has reached 7.7%, and how “fat” the tail risk is will depend on a combination of idiosyncratic factors and policy stance, meaning that the range of outcomes can be large. For example, Evergrande, Kaisa and Yango have not defaulted on their offshore bonds, but are showing clear signs of stress. In aggregate, these three issuers have USD 34.5bn of offshore bonds outstanding.

Advertisement

Precisely what constitutes “default” is getting awfully fuzzy amid delays and swaps and other dodgy deals.

Anyway, the point is that the Chinese developer dollar-bond market is frozen solid and as such there is a lot of liquidity stress for the ponziteers. This means that they are having to shrink their balance sheets any way that they can, from selling assets to discounting new project sales to reduced land banking.

China Crash 2022 point two: falling property

Advertisement

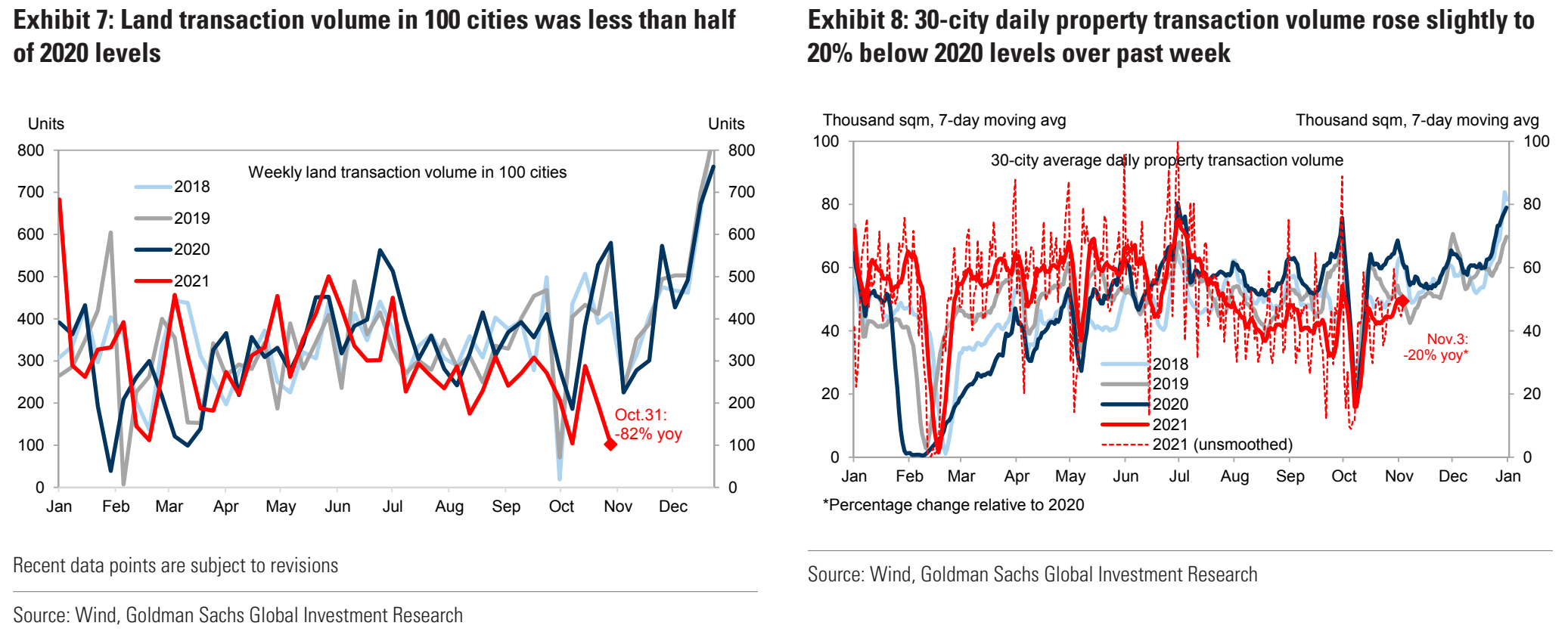

Frozen developer financing brings us to a correcting property market as both volumes and prices tumble. This week saw some improvement in new property sales but the land market remains shot to pieces:

Whether new project sales have bottomed is dubious:

Advertisement

There are signs that mortgage loans to second-hand home buyers are picking up in some cities, including tier-one cities, offering a relief to cash-strapped property developers. But industry insiders say that the overall credit environment remains tight and the policy stance for the real estate sector hasn’t changed.

“I applied for mortgage loans in mid-August and the bank told me back then that I would have to wait until January next year. Surprisingly, I recently received the loans,” said a second-hand home buyer in Shanghai.

A staff of a large real state broker in the city said that “waiting time for second-hand home mortgage loan approvals has been shortened recently. In the past few months, waiting time was about 4 – 6 months and now it’s only half of that, although not every bank is accelerating the loans.”

A smaller broker in the city said that”our second-hand home mortgage business volume is small in Shanghai and we haven’t seen notable pick-up in loan approvals at banks that we work with.”

“We now have mortgage quota for second-hand home buyers. After they submit all required documents, it takes only a couple of days for them to get approvals,” said a staff at Shenzhen branch of a state-owned bank.

Separately, a staff at a joint-stock bank in the capital city of Beijing said “we’ve got mortgage quota for November. There is no limit on one single loan for qualified buyers. Loan approval can take less than a month, but I’m not sure about the situation next month.”

A person at another Shanghai-based bank said that it now takes 3 – 4 months for second-hand home buyers to get mortgage loans, faster than in July and August, adding that “mortgage loans increased slightly but not much.”

“Currently, loans being delivered are mostly those applied in August and September, even in June and July. Restrictions remain and mortgage loan quota is still being controlled,” he said.

In the meantime, some banks remain cautious in the business, with a loan manager at a state-owned bank’s Guangzhou branch saying that “home buyers still need to wait and there may not be any quota until early next year.”

In October, banks granted some 150 billion yuan to 200 billion yuan ($31 billion) more property loans than in September, according to a Thursday report from state-backed media outlet Cailianshe, citing unidentified sources.

Chinese regulators including the People’s Bank of China (PBOC) and the China Banking and Insurance Regulatory Commission (CBIRC) have repeatedly pledged to “safeguard healthy development of the real estate market and protect home buyers’ rights.”

Authorities do not want genuine buyers to be shut out of the market or developers to face delays in receiving payments.

The PBOC and the CBIRC held a special meeting about real estate financing at the end of September, asking banks to correctly understand and implement policies on real estate financing, maintain steady and orderly loans to the sector and promote healthy development of the housing market.

“Previously, bank lending to the real estate sector had been strictly restricted, but after recent adjustments, banks can offers loans to the sector normally,” said Dong Ximiao, chief analyst at chief analyst at Merchants Union Consumer Finance.

Beike Research Institute said that the PBOC has sent several positive signals since the end of September and real estate lending is expected to return to a “steady and orderly” situation in the fourth quarter.

The improvement in credit environment will help improve market expectation and encourage potential home buyers to make purchase decisions, said Beike.

Meanwhile, loan approval had also been faster due to fewer home buyers waiting in the queue, said Zhang Dawei, chief analyst with property agency Centaline.

According to data from China Rea Estate Information Corporation (CRIC), second-hand home transactions in the country’s 10 major cities declined 48% year over year in October, down 40% from the same period in 2019.

Data from the Guangzhou Real Estate Intermediary Association, second-hand home transactions in the city fell 15.25% in October from a month earlier, slumping 50.9% from a year earlier. In Shanghai, second-hand home transactions fell 33.235 month on months in September.

Analysts also noted an acceleration in the issue of residential mortgage-backed securities (RMBS) by banks, implying banks are given another capital-raising route as they use up funds to lend to home buyers.

“The issuance of local RMBS reached 77 billion yuan in September,” said Huatai Securities.

“Issuance resumed after a two-month halt and rose by a significant amount, which we see as a gesture of (regulatory) guidance.”

As of end-September, outstanding mortgage loans reached 37.37 trillion yuan ($5.84 trillion), central bank data showed.

So, as developer liquidity slumps and property markets fall, we need to consider the broader spillovers.

China Crash 2022 point three: construction spillovers

Advertisement

Sadly for China, it has waited far too long to bring its developer ponzi scheme to heal and it has become embedded in very significant areas of the economy.

The most important is the infrastructure sector which relied heavily upon land sales for revenues to invest. As developer balance sheets shrink, this revenue has collapsed.

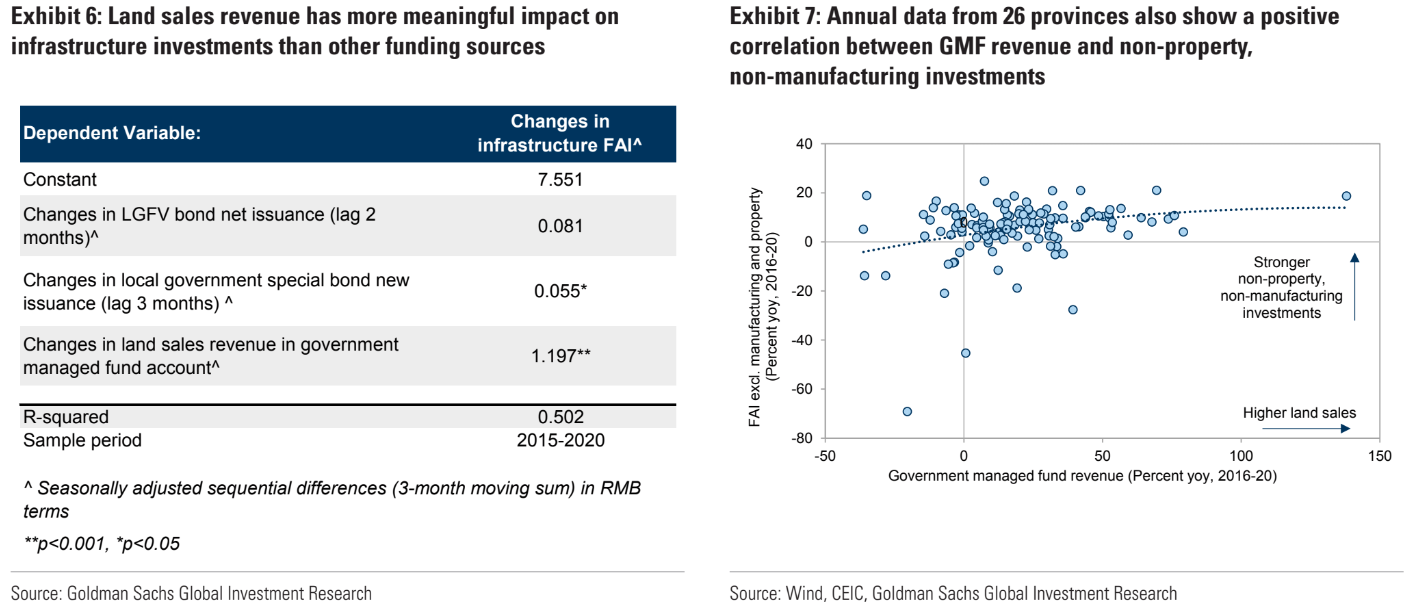

Roughly one-third of local government revenues are land sales and the rate of change is this financing matches the change in infrastructure investment. Goldman:

Advertisement

Revenue from sales of land use rights has been an important source of revenue for local governments in China, accounting for nearly 30% of local level fiscal revenue. Fiscal spending such as land development, urban and rural construction, education and other infrastructure related expenditure in theGovernment Managed Fund (GMF) account are highly dependent on land sales revenue. Therefore, the potential shortfall of fiscal revenue due to waning land sales suggests lower fiscal spending by local governments going forward.

Our historical analysis suggests changes in land sales revenue in the GMFaccount translate into the same magnitude of changes in infrastructure investments in RMB terms, while the impact of changes in net LGFV bond issuance and changes in local government bond issuance are well below one for one. This points to headwinds for infrastructure investments next year.

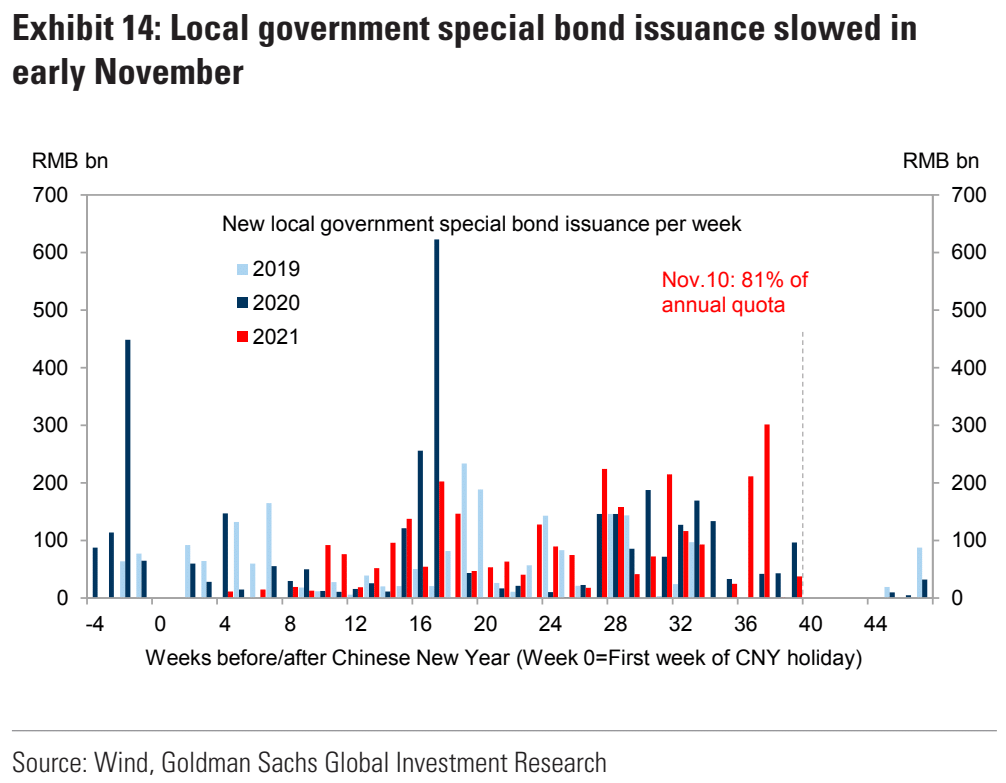

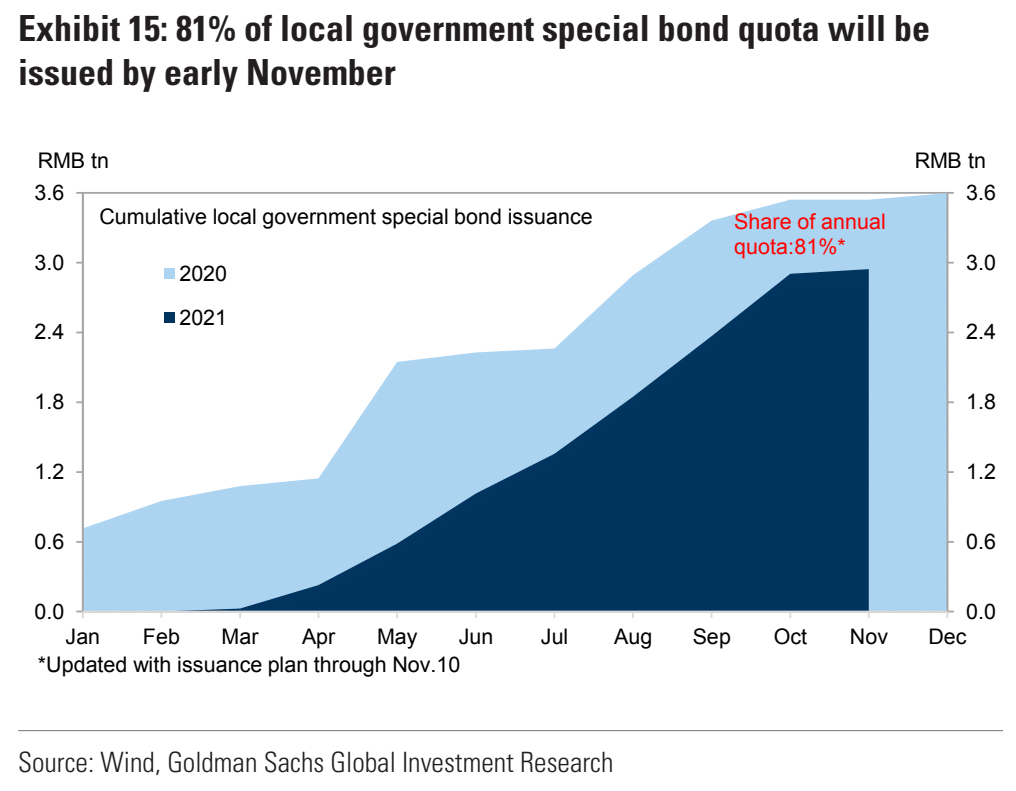

Looking ahead, higher new local government special bond quota and more flexibility in local government financing are necessary to offset the drag on infrastructure investments from declines in land sales revenue in 2022.

We are seeing precisely this outcome now as LGFV issuance sags despite everybody claiming that it is going to save construction. The opposite is the truth:

Advertisement

In short, lifting quotas won’t do jack when demand is the problem.

China Crash 2022 point four: other spillovers

Advertisement

Once construction goes in China the spillovers to the real economy multiply dramatically. The first channel of contagion is supply and daisy chains:

The key to managing the crisis is not just to contain the risk of the financial loans, but also the other two-thirds of the liabilities owed by the distressed real estate developer to a vast network of enterprises in its supply chain, including providers of construction services and material as well as contractors and subcontractors. Even though the PBOC has powerful tools to mitigate an Evergrande shock to the financial system, the fallout could still cause indirect yet long-lasting damage to much of the economy. If not properly managed, this could affect the entire value chain of the property market in China and beyond.

China boasts the world’s most complete supply chain because of its vast range of manufacturing. This strength comes with a lurking risk: the sudden collapse of a big non-financial company can cause cascading effects for the real economy at a scale unseen in any other part of the world.

…Amid this crisis, many of these suppliers have had no choice but to accept longer payment terms. When these payments finally come due, the companies are then often asked to accept commercial bills instead of cash. This is effectively a further extension of payment terms, unless suppliers sell the bills to brokers at a discount. And the trouble can just continue from there. Recently, a broker sued a supplier of Evergrande in a Chinese court for an outstanding commercial bill. The fallout from a collapse by the developer will cause a vast group of suppliers to not only lose business, but also experience immediate financial distress, possibly resulting in a chain of bankruptcies upstream.

Never fear, developers are paying with empty apartments:

Advertisement

1/4

“On Monday, a furnishings supplier said that it had received property from Evergrande to offset about 39 million yuan overdue IOUs from the company. A property broker also said that it had received flats worth 253 million yuan in lieu of payment.”https://t.co/dWLTif69bN

Will employers pass them onto employees as pay? Needles to say, this only adds downside momentum to the lost currency of Chinese realty.

The second channel of contagion is via the wealth effect for households. Chinese consumption is already struggling mightily to grow at anything like the rates needed to rebalance the economy. There are no substantial policies in place to fix this in structural terms, so we can expect the Chinese consumer to continue to fade away through 2022.

Advertisement

China Crash 2022 point five: Emperor Xi

We have seen China try to do this before. In 2012, 2015 and 2019 it aimed to deleverage property and shift its economy to a greater consumption share. Each time it got spooked along the way and reverted to construction stimulus.

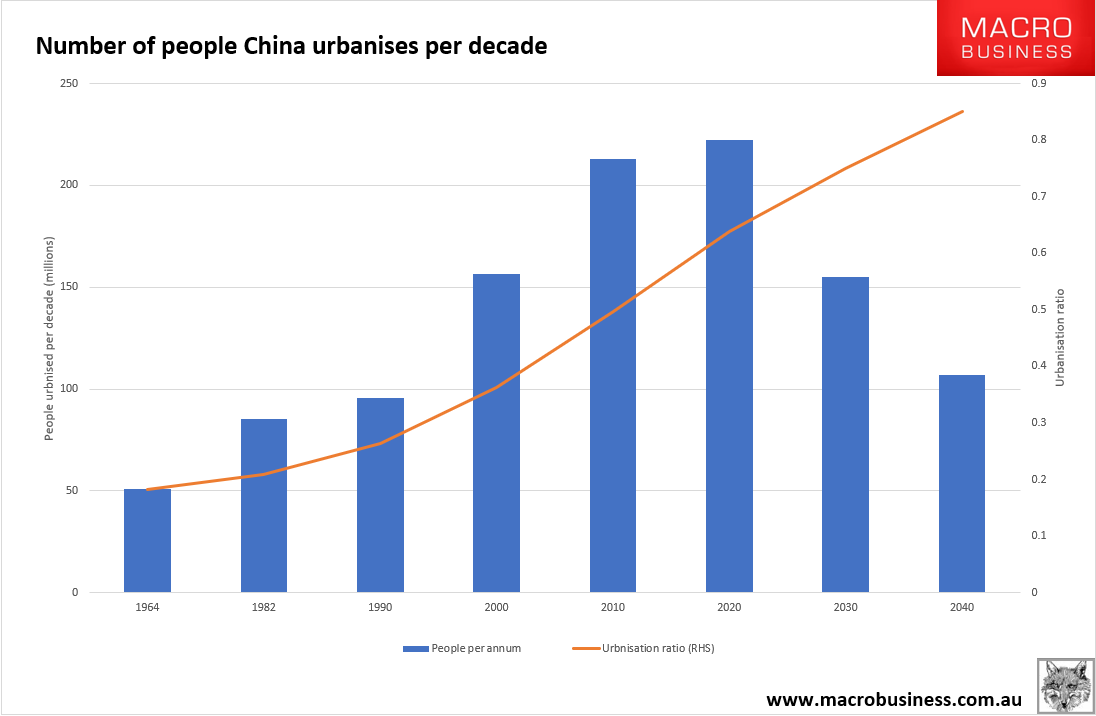

Why should this time be any different? For two reasons. First, the underlying drivers of urbanisation have topped out. What has been wasted capital in overbuilding to this point will become an outright economic millstone if it is allowed to continue as real demand falls away:

Advertisement

Chinese policymakers know this. The PBoC this week was instructive:

According to the reporter’s understanding, the People’s Bank of China has recently communicated in various localities on accurately grasping the requirements of the prudential management of real estate finance, steadily carrying out real estate loan business, and maintaining the stable and orderly distribution of real estate credit. In some regions, the branches of the People’s Bank of China have begun to carry out actions based on local conditions. Window guidance. Judging from the current situation, the real estate credit adjustments of more institutions are being adjusted across regions under total control. Li Mingdong, general manager of the risk management department of China Merchants Bank, said at the bank’s third-quarter performance exchange meeting that the bank emphasized the self-repayment of projects and strictly closed management of real estate development loans in terms of investment in real estate development loans; In terms of project selection, the bank focuses on rigid-need and improved housing in first- and second-tier cities, and while actively meeting the financing needs of rigid-need housing, it maintains a stable self-compensated cash flow for the entire project. The relevant person in charge of Ping An Bank stated that the bank will focus on selecting cities with net population inflows and strong industrial support, and projects with geographical advantages, especially projects with good sales prospects and short planning periods.

Advertisement

In short, no more ghost cities.

Armed with this understanding, the CCP has launched a much more comprehensive political framework for the real estate adjustment this time around than previous attempts. The rhetorical and regulatory umbrella of “common prosperity” gives Emperor Xi the political cover to persist far longer in his push to squash property developers than previous attmepts. Indeed, he is putting this at the heart of his bid to become Emperor for Life.

Nonetheless, it remains my view that the good Emperor will ultimately panic. There are too many pro-cyclical features and linkages from Chinese property to the broader economy. As one falls so will the other, even allowing for the offset of booming exports and rising services plus value-added manufacturing spending. Chen Long of Plenum is worth a listen on this:

Yeah. I tend to believe that this time is not that much different from previous episodes. I mean, I know there’s the argument there, saying, “Xi really wants to reduce the share of the real estate in the economy, and wants to curb housing prices.” But I don’t think this is new. We have this episode, like you just mentioned, multiple times in the last 15 years. Basically every three years, we have a property cycle, from trough to peak to trough. Right? And the Chinese government, in both central and local, that will change policies very, very quickly.

And this time is no different, right? Because you talk about the three red lines, the three red lines really were just introduced a year ago, last August. Right? And, well, the background of that was the PBOC, along with other policy makers, the property market recovered too quickly, and think they’re doing too well. And housing prices in cities, especially big cities like Shenzhen or Shanghai, were rising too fast. And that was a little bit unanticipated. So they said, “No, we have to restrict the area, this kind of bull run.”

And now a year after Beijing and many local governments introduced restrictive policies, finally, we had three months in a row of property sales volume falling by double digits, on a year on year basis. But this is just three months, right? If you look at the previous cycles, especially 2015, 16, we could have the down cycle for 15 months. But this is just three, right? So Beijing has not blinked yet, because it’s only three months. Right?

Advertisement

So, I expect the China Crash of 2022 to eventually break the Emperor’s will and lead to more credit stimulus. Just not before the economy is effectively in recession and we see a shock so large that he has no choice.

But, even then, I do not expect any kind of new boom. Just less pain for a while as China continues down the path of ex-growth.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.