By Gareth Aird, head of Australian economics at CBA:

Key Points:

- The RBA stated in the November 2021 Statement on Monetary Policy that their updated central scenario for the Australian economy is consistent with the first increase in the cash rate being in 2024.

- But the RBA’s updated central scenario is conditioned on a path for the cash rate broadly in line with recent market pricing (i.e. ~100bps of hikes to the cash rate in 2022 and ~60bps of hikes in 2023).

- If the RBA kept the cash rate assumption unchanged at 0.10% over their forecast horizon they would need to mechanically upwardly revise their GDP and inflation profile in 2023 which would mean their central scenario is consistent with a rate hike before 2024.

- We believe the RBA’s central scenario for the economy should have the underpinning assumption of no change to the cash rate, consistent with their forward guidance, given the RBA is using their central scenario as the basis for their forward guidance on the cash rate. That is, the central scenario and assumption about the cash rate should be consistent.

- We expect the RBA to commence raising the cash rate in November 2022.

Let’s revisit the RBA’s latest forecasts and assumptions:

The RBA presented their updated central scenario for the Australian economy in the November Statement on Monetary Policy (SMP).

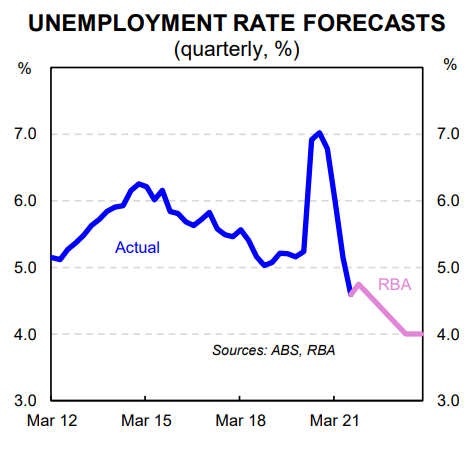

In the RBA’s central scenario underlying inflation sits at 2¼%/yr until mid-2023 and only reaches the middle of the 2-3% target band by the end-2023. At that point wages growth is forecast to be 3%/yr.

According to the RBA, “depending on the trajectory of the economy at that time (i.e. end-2023), the Board judges that this outcome could be consistent with the first increase in the cash rate being in 2024.”

In other words, based on the RBA’s central scenario for the economy presented in the November SMP they do not expect to raise the cash rate before 2024.

However, the RBA stated that their forecasts in the central scenario are conditioned on a path for the cash rate broadly in line with recent market pricing.

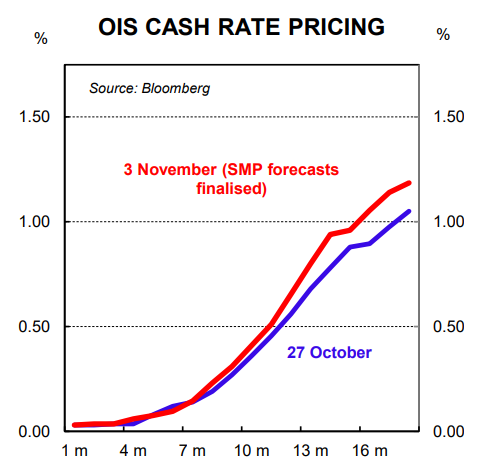

The forecasts were finalised on 3 November 2021. At the time the money markets had priced ~100bps of hikes to the cash rate in 2022 and another 60bps of hikes in 2023. For context, a week earlier on 27 October 2021 markets had priced ~100bps of hikes to the cash rate in 2022 and another 65bps of hikes in 2023.

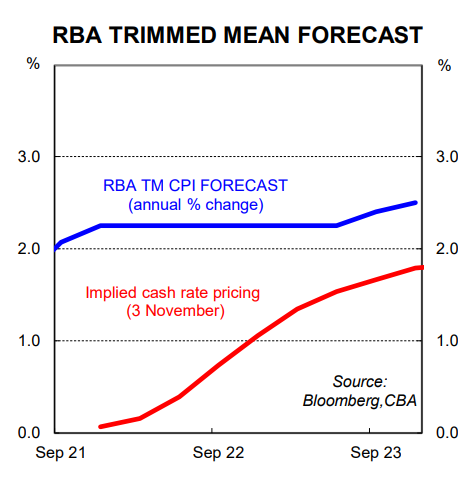

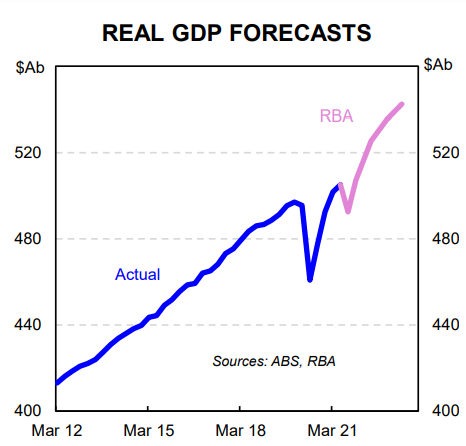

Taken together, the RBA’s central scenario and underpinning assumption on the cash rate mean at end-2023 the RBA sees inflation at 2.5%/yr and wages growth at 3.0%/yr with a cash rate of 1.75% (see facing chart). This seems completely inconsistent with the line that the Board sees the first increase in the cash rate being in 2024.

Changes to the cash rate impact economic outcomes

Changes to the cash rate impact other interest rates in the economy. And this in turn influences economic activity and the level of prices in the economy. Lower interest rates stimulate spending which boosts demand in the economy. This has an impact on employment and can also influence prices in the economy (i.e. inflation).

According to the RBA, lowering the cash rate by 100bps leads to GDP being 0.5 to 0.75ppts higher than it otherwise would be over the course of two years. Inflation typically rises by a bit less than 0.25ppts per year over two to three years.

The reverse is also true. Raising the cash rate by 100bps should lead to GDP being 0.5 to 0.75ppts lower than it otherwise would be over the course of two years. And inflation should be lower by a bit less than 0.25ppts per year over two to three years.

More generally, the RBA have said that estimates suggest that it takes between one and two years for changes in the cash rate to have their maximum effect on economic activity and inflation. This means that rate hikes in 2022, as implied by market pricing which underpinned their central scenario, would have had a material influence on the RBA’s forecasts for GDP and inflation in 2023 (see below).

There’s a better way to forecast and provide guidance

On the one hand the RBA has said that inflation and wages outcomes in their central scenario are consistent with the first increase in the cash rate being in 2024. But on the other hand they have effectively said their central scenario has been constructed on the basis that they deliver ~100bps of rate hikes in 2022 and ~60bps in 2023.

In our view the RBA should construct their central scenario for the economy using the assumption that the cash rate is unchanged if the Board is going to use the outcomes of the central scenario as the basis for their forward guidance on the cash rate.

This is particularly important when the market has priced a tightening cycle that should have a non-trivial impact on the RBA’s forecasts for GDP, unemployment, inflation and wages, which therefore influences the forward guidance.

We expect inflation to rise earlier than the RBA anticipates. Our forecast is for underlying inflation to be 2.5% by mid-2022 and the risk lies with a higher outcome. So whilst we don’t agree with the RBA’s profile for inflation and their forward guidance on the cash rate, it is still worth asking the question as to what the RBA’s central scenario would look like using the assumption that the cash rate is unchanged at 0.10% over their forecast period.

At a minimum we would expect the shift in assumption to an unchanged cash rate over the RBA’s forecast horizon to lift their profile for GDP by 0.5ppts in 2023. And both underlying inflation and wages growth in 2023 should be increased by 0.25ppts. By end-2023 it could be argued that the RBA should lift their profile for underlying inflation by 0.5ppts given the extent of tightening priced in at the time they constructed their central scenario.

An upward revision to the RBA’s inflation profile in the central scenario based on an unchanged cash rate assumption would almost certainly see the RBA’s conditional forward based guidance on the cash rate shift from a rate hike in 2024 to a rate hike in H2 2023.

Such a change may not matter a lot for financial market participants or economic forecasters such as ourselves. Our call for the RBA to commence normalising the cash rate in November 2022 is based on what we think will happen to the economy rather than what the RBA has forecast.

But making this change would improve the link and transparency between the RBA’s economic forecasts and their forward based guidance on the cash rate which is very important for a lot of Australian households and businesses.