By Gareth Aird, head of Australian economics at CBA:

Key Points:

- Australian dwelling price growth is forecast to moderate over the first half of 2022 on higher fixed mortgage rates, affordability constraints and natural fatigue after a period of extraordinary price gains.

- A further tightening in macro-prudential policy looks unlikely in our view given higher fixed mortgage rates will deliver APRA the desired cooling in the market.

- Our expectation for the RBA to commence normalising the cash rate in November 2022 means that we expect national dwelling prices to peak in late 2022 around 7% higher than end-2021 levels.

- We expect an orderly correction in home prices of around 10% in 2023 as the RBA takes the cash rate to 1.25% by Q3 2023.

Summary

The Australian housing market is in the twilight of an incredible boom that has been fuelled by record low mortgage rates. The phenomenal lift in prices is not over yet given dwelling prices are still rising briskly in most capital cities. But near term indicators of momentum coupled with the recent move higher in fixed rate mortgages suggest that conditions will moderate from here.

In many respects it’s a simple story. The price that someone is willing and able to pay for a home is predominantly influenced by two things – income and borrowing rates. As home prices move higher, affordability becomes stretched. That can be improved via a reduction in mortgage rates or higher income. But at some point the tailwind of lower mortgage rates on prices wanes unless there are further cuts in interest rates.

Of course the story is not all one way. Interest rates become a headwind on property prices if they are rising. That is the place we believe we are moving towards over the next two years given our expectation for the RBA to commence normalising the cash rate in late 2022.

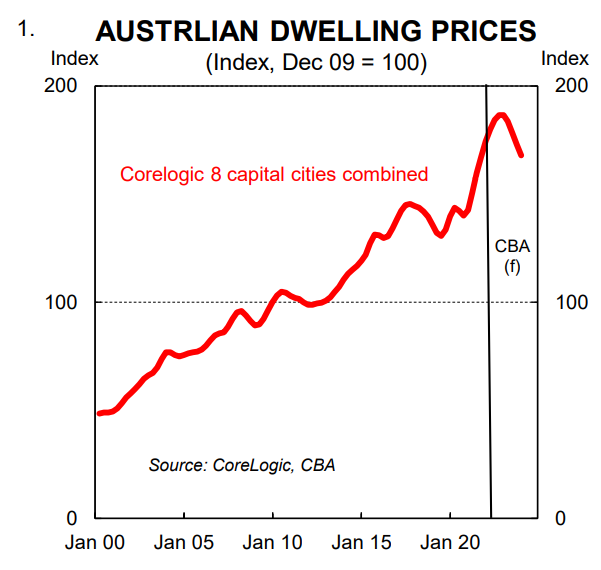

In this note we update our central scenario for home prices and extend our forecast profile to end-2023. Dwelling prices nationally will end 2021 up by ~22% and very much in line with our call for a 20% increase in early August. From there we expect prices to continue to rise through the first half of 2022, but at a more modest pace.

We look for prices to peak in late 2022 around 7% higher than end-2021 levels. We then expect an orderly correction in dwelling prices of 10% in 2023 (chart 1).

A gradual and shallow RBA tightening cycle that takes the cash rate to 1.25% by Q3 2023 lies at the heart of our expectation that home prices will contract over 2023.

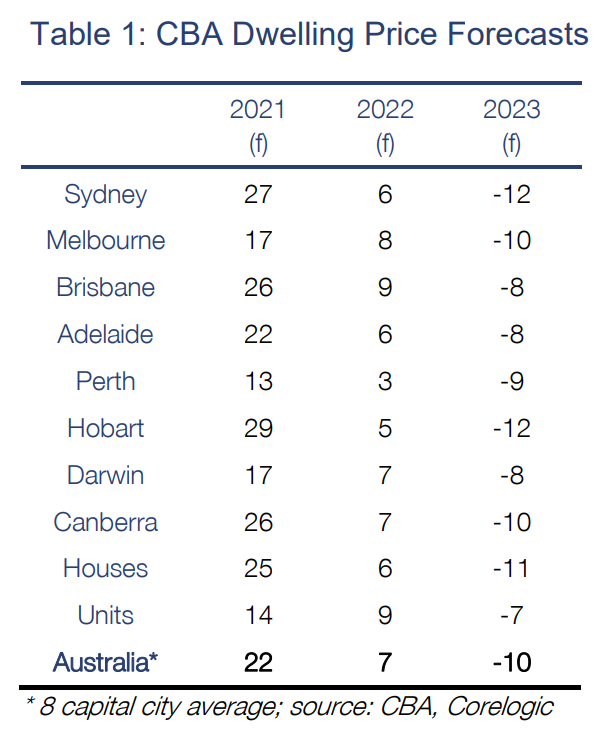

The cash rate is forecast to lift because the economy will be at full employment and annual wages growth will have pushed to the desired level of 3%. Stronger wages growth will provide a partial offset to rising interest rates on the property market. In addition, a lift in population growth as the international border reopens will boost the underlying demand for bricks and mortar, particularly inner city apartments. As such, we expect house prices to decline by a little more than apartment prices over 2023 (Table 1).

Recent story

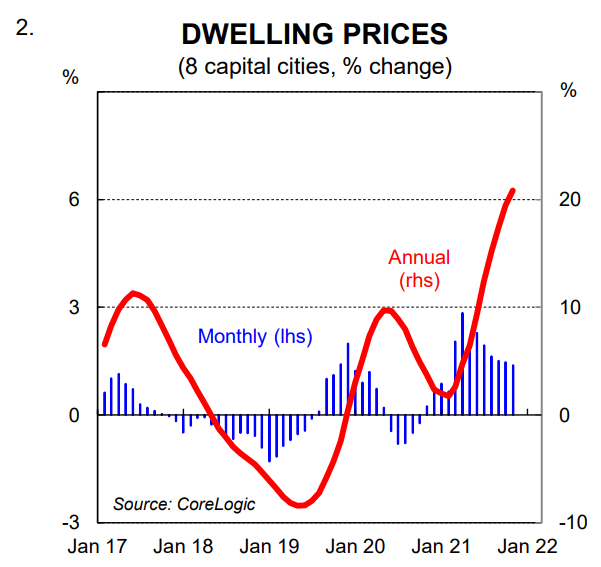

Lockdowns in large parts of the country from July to October 2021 had no discernible impact on the demand for housing. The upshot is that Australian home prices have risen at an extraordinary pace over 2021. According to CoreLogic, property prices rose by a robust 1.4% across the eight capital cities in October (latest available). That builds on similar increases from July to September, although there has been a clear moderation in the monthly pace of price gains (chart 2). Annual growth accelerated to 20.8% in October due to base effects.

The housing market has without a doubt been red hot. But the recent price outcomes pre-date two key developments that will exert a cooling influence on the property market.

First, APRA announced in early October an increase in the minimum interest rate buffer it expects banks to use when assessing the serviceability of home loan applications. More specifically, the minimum interest rate buffer was increased to 3.0% from 2.5%. The policy change came into effect on 1 November 2021.

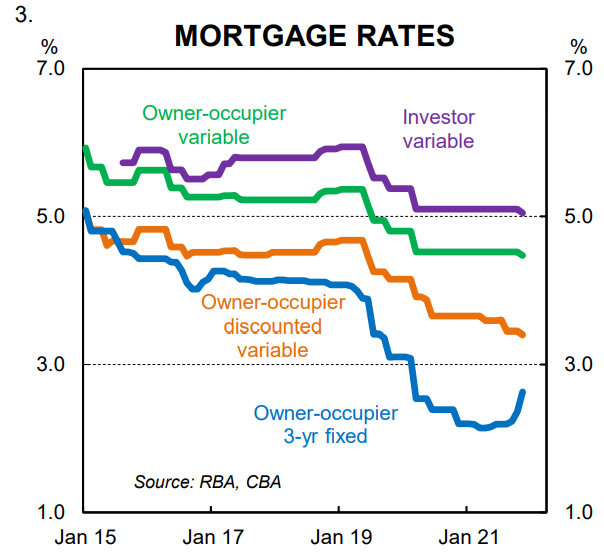

Second, a number of lenders have in recent weeks lifted interest rates on fixed rate mortgages in line with higher funding costs and the RBA’s abandonment of its yield curve target. This will have a dampening impact on the demand for credit.

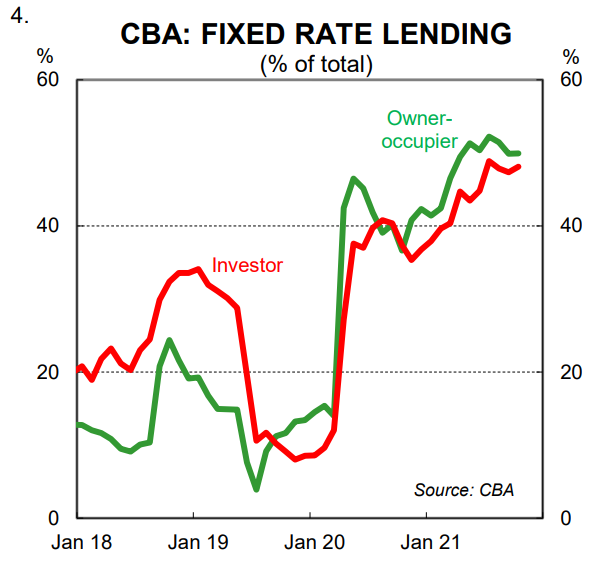

The share of new lending that has been fixed over the pandemic as opposed to floating has been a lot larger than usual because fixed rates have generally been lower than the standard variable rate (charts 3 and 4). The increase therefore in the interest rates on fixed rate mortgages will have a larger than usual cooling influence on the demand for credit. In addition, the lift in the fixed rates is a reminder to would-be borrowers that interest rates can move higher.

We believe that APRA will welcome a lift in fixed mortgage rates to the extent that it makes it less likely that they will need to employ further macro-prudential policies to cool the market. Indeed it is now our central scenario that the housing market will moderate sufficiently over the early part of 2022 and that there will be no further macro-prudential policy changes.

Prices will keep rising before they correct lower

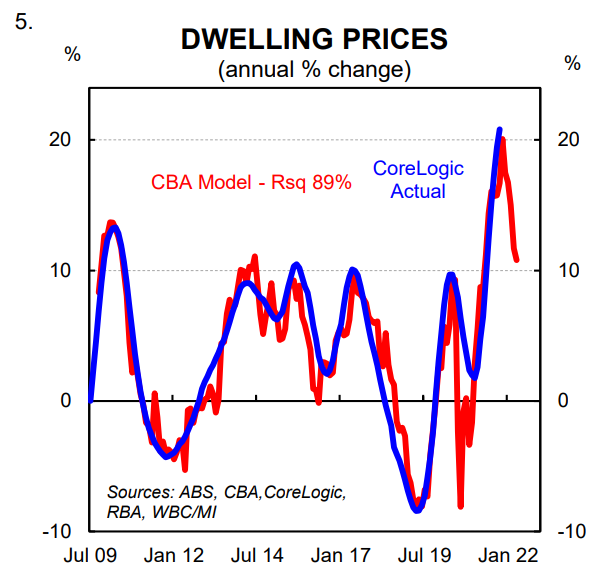

A cooling market is not the same thing as a falling market. Prices are still rising at a reasonable pace. And near term momentum indicators like auction clearance rates and the house price expectations index from the WBC/MI Consumer Sentiment survey, which feed into our proprietary dwelling price model, point to home prices continuing to rise at a softening pace which now sits at around 1% per month (chart 5).

We expect the pace of monthly gains to moderate quite significantly by mid-2022 due primarily to higher fixed mortgage rates. As this happens we expect a cooling feedback loop to intensify whereby subduing buyer expectations coupled with general fatigue and a growing anticipation of RBA rate hikes sees prices peak in Q3 2022 (at this point we forecast prices will be around 7% higher from end-2022 levels). Whilst in some respects point forecasts are false precision, they provide guidance on what sort of a lift in prices we are looking for in 2022 before the peak is reached, which we believe will be on the eve of the RBA’s tightening cycle.

How far will prices correct lower

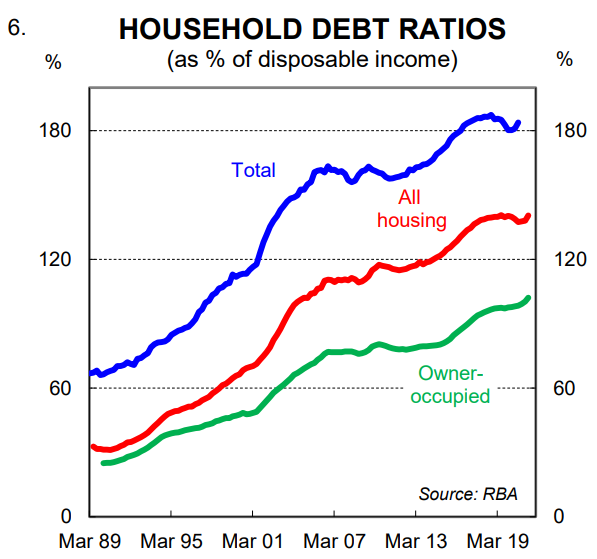

The extent to which prices correct lower will depend in large part on the speed and magnitude to which the RBA lifts the cash rate. On that score we expect a shallow and gradual tightening cycle given the elevated level of household

indebtedness (chart 6).

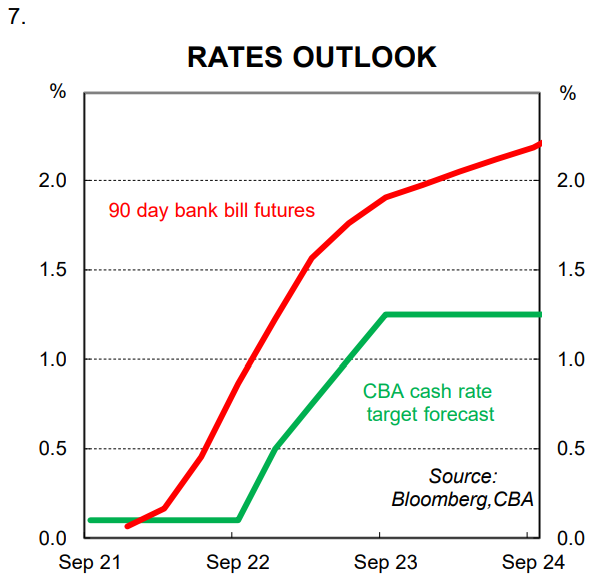

Our base case is that the RBA starts normalising the cash rate in November 2022 (chart 7). We have pencilled in a first increase of 15bp in November 2022, which would take the cash rate to 0.25%. We expect that to be followed by an increase of 25bp in December 2022. We have three further 25bp hikes in Q1 23, Q2 23 and Q3 23 that take the cash rate to 1.25% (our estimate of neutral which is a lot lower than the RBA’s estimate of “at least” 2.5%).

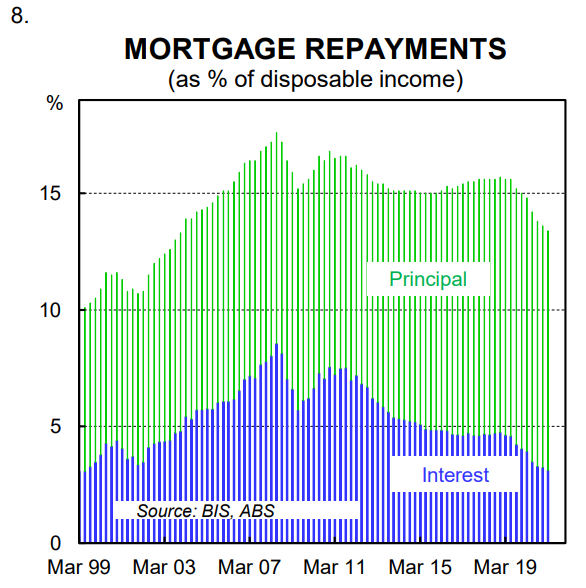

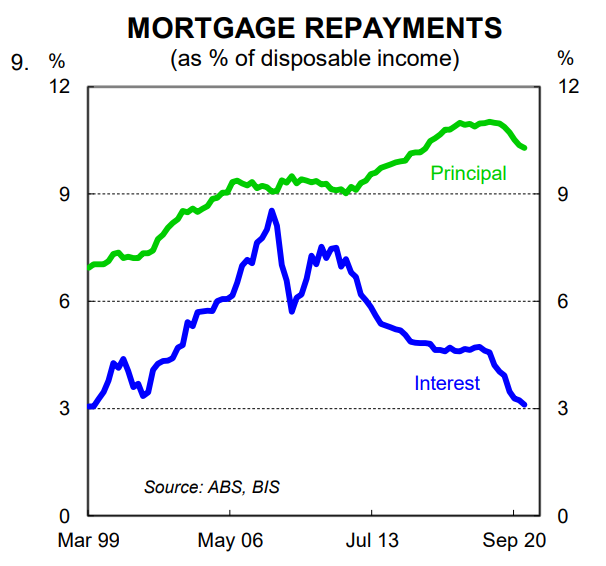

The standard variable rate could be expected to move higher in a broadly similar fashion to the path of the cash rate. As such, a lift in the cash rate to 1.25% would take mortgage repayments as a share of household disposable income to around 15.0%. This is the level we asses to be ‘normal’ based on the experience of the past two decades (charts 8 and 9).

Rising rates will put downward pressure on the demand for credit which will result in dwelling prices correcting lower. Indeed rising rates work in much the same way falling interest rates generate an increase in demand for credit and higher home prices.

The impact of rising interest rates will be quite significant on borrowing capacity and credit demand given the percentage change will be large (the lower the starting interest rate the bigger the percentage change for a given percentage point change in rates). However, it is important to consider why we expect the RBA to raise the cash rate in late-2022 – the economy will be at full employment and annual wages growth will have pushed to the desired level of around 3%.

Stronger wages growth will provide a partial offset to rising interest rates on the property market. In addition, a lift in population growth through 2023 due to higher net overseas immigration will boost the underlying demand for bricks and mortar.

As a result, we forecast dwelling prices to fall by around 10% in 2023. This may on the surface sound like a large fall. But context is key. Price rises have been exceptional over 2021 and further gains are forecast in 2022. A decline in national dwelling prices of 10% in 2023 on our figuring simply take prices back to where they were in Q3 2021 (of course the decline would be larger in real terms).

The backdrop of an economy running at full capacity, which is why the RBA will normalise the cash rate, means we believe the economy will be well positioned to absorb a decline in home prices of around 10% over a year. It won’t be the first time home prices have corrected lower. Recall that national home prices declined by 10% from September 2017 to June 2019.

Risks

The key risk to our forecast for home prices, both upside and downside, is the path of interest rates. If the RBA tightens policy more aggressively and/or earlier than our forecast profile for the cash rate we would expect dwelling prices to fall by more than our central scenario. Equally, if the RBA tightens policy later than we anticipate or delivers a more shallow tightening cycle we would expect a smaller decline in home prices in 2023.

In the near term the main risk to our forecast profile is around macro-prudential policies. If APRA was to bring in additional policies to cool the housing market or further lift the serviceability buffer we would expect smaller price rises in 2022.