DXY held its recent gains as EUR bounced a touch:

The Australian dollar hit new lows for the move:

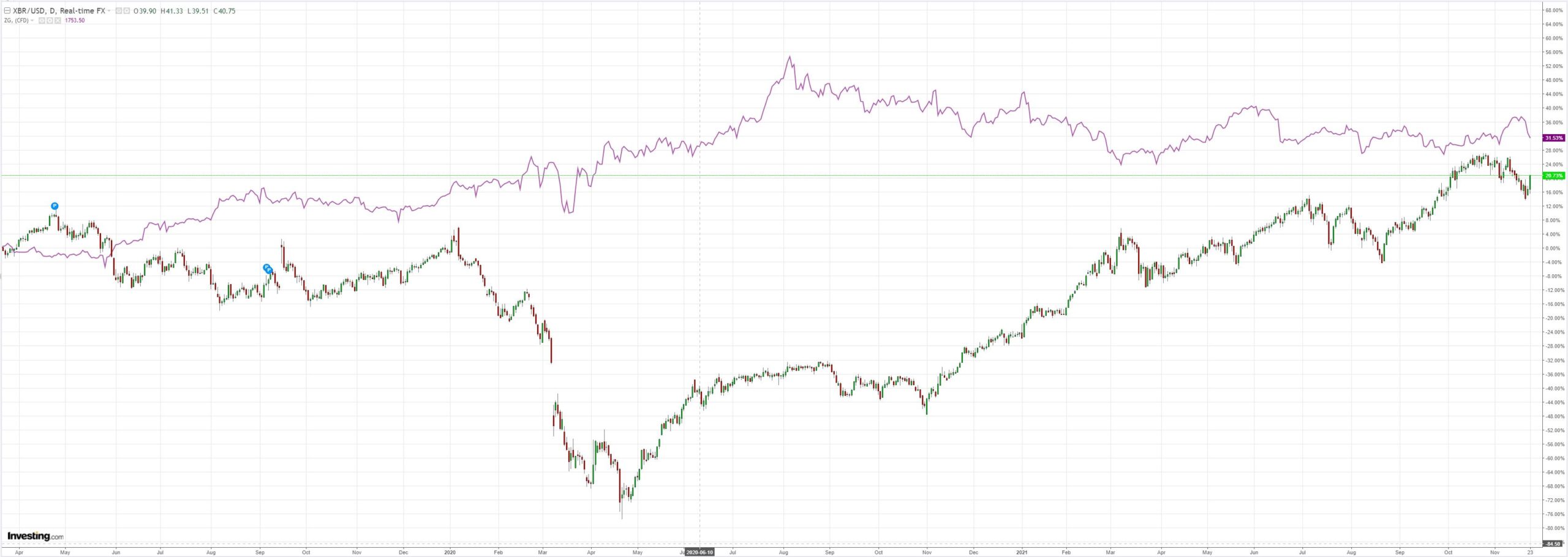

Gold fell, oil rallied:

Base metals were mixed:

Big miners bear market rallied:

EM stocks are rapidly heading back to the cliff’s edge:

As junk folds:

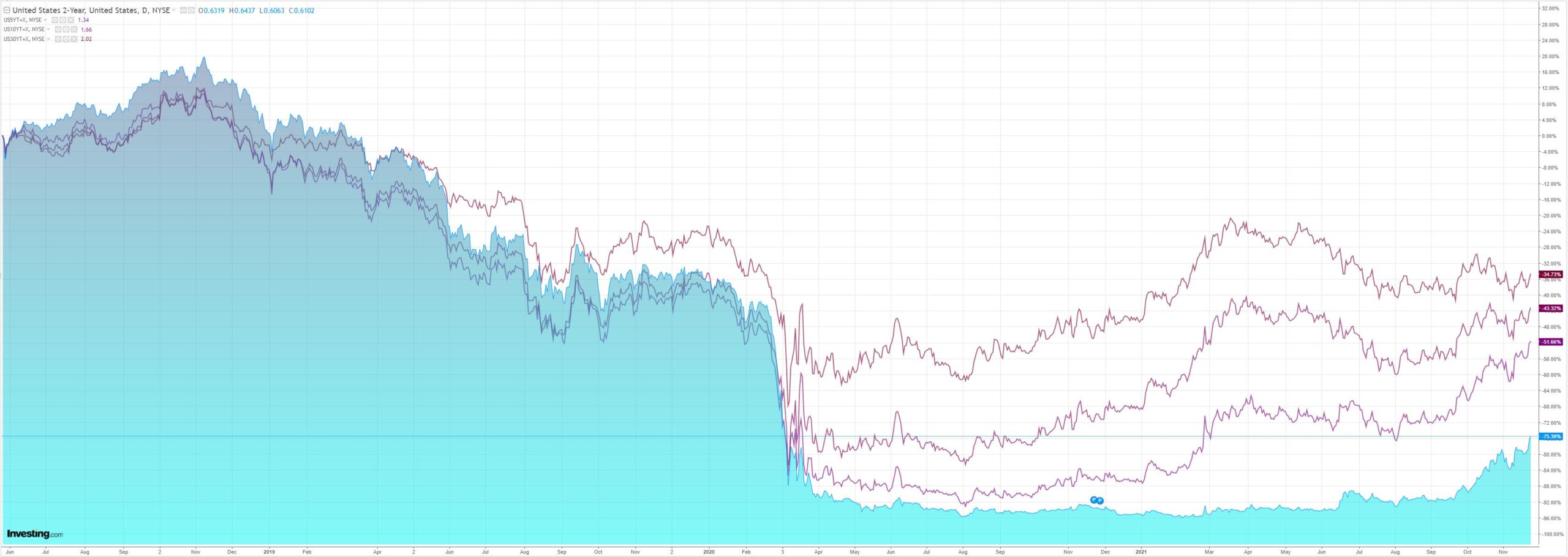

Long yields rose but the curve is unmistakeably flattening:

GAMMA finally had a bad day bit not as bad virus-afflicted Europe:

Westpac has the wrap:

Event Wrap

US PMIs were firm. Manufacturing was in line with expectations at 59.1 (prior 58.4), while services were softer at 57.0 (est. 59.0, prior 58.7), for a composite reading of 56.5 (from 57.6). The Richmond Fed manufacturing survey was in line with estimates at 11 (prior 12), although new orders were lower at 5, from 10 in October.

FOMC member Bostic said they may need to speed up removal of monetary stimulus in response to strong employment gains and surging inflation, allowing for an earlier-than-planned increase in interest rates: “A faster taper would certainly give us more optionality as we move into 2022 and see sort of where the data takes us… I definitely think it is appropriate for us to be talking about the pace of tapering and being open to a faster one.”

Eurozone PMIs surprised with moderate gains, despite increased pricing pressures and Covid case rises weighing on optimism. Manufacturing rose to 58.6 (prior 58.3, est. 57.4), services beat to 56.6 (prior 54.6, est. 53.5).

The ECB’s Knot (a known hawk) said there was little chance of a rate move in 2022 and that PEPP would cease in March, but raised concerns over the risks of persistent inflation feeding into secondary price rises and therefore a need for ECB to react. Makhlouf said there were no signs of secondary inflation pressures, but that the ECB cannot afford to be complacent and needs policy tool optionality.

UK PMIs were solid. Headline manufacturing edged up to 58.2 (est. 57.3, prior 57.8), while services dipped to 58.6 (est. 57.2, prior 59.1).

US, UK, Japan, India and S. Korea announced a coordinated tapping of strategic oil reserves to stem oil price gains, and challenged OPEC+ to lift their conservative production targets. However, the amount tapped (50m barrels from US) was less than the market expected.

Event Outlook

Australia: Stringent restrictions during the NSW and Vic delta lockdowns weighed heavily on construction work in Q3 (Westpac f/c: -3.2%). The RBA’s Assistant Governor (Financial System) will appear on two panels: one on central bank digital currencies at 9:15am; then another on the future of payments in Australia at 11:40am.

NZ: Westpac anticipates a follow-up 25bp increase in the RBNZ’s official cash rate to 0.75% at the November meeting; a 50bp hike is a clear risk.

Japan: The Nikkei manufacturing PMI should remain expansionary in November as a much reduced delta case count builds support for the services PMI.

Germany: The November IFO business climate survey should reflect the underlying strength of the recovery despite supply disruptions and energy uncertainty.

US: The downtrend in initial jobless claims will likely remain in place (market f/c: 261k) while wholesale inventories for October should report modest growth (market f/c: 1.0%). A small revision in the second estimate for Q3 GDP is also anticipated (market f/c: 2.2%), and October’s durable goods orders are expected to point to solid investment growth at the start of Q4 (market f/c: 0.2%). Cost shocks from energy and supply disruptions will likely lift core PCE inflation to a new 30-year high in October (market f/c: 0.4%mth; 4.1%yr). Personal spending should see robust gains across goods and services (market f/c: 1.0%) as personal income stabilises after the conclusion of fiscal support (market f/c: 0.2%). The final release for November’s University of Michigan sentiment will again reflect the disparity between weak sentiment and strengthening activity (market f/c: 66.9) while new home sales are expected to hold steady in October with supply issues hindering construction (market f/c: 800k). The FOMC’s November meeting minutes will subsequently be scrutinised for any details regarding the Committee’s views on inflation and how they plan to pivot to rate hikes after tapering.

Nothing new to add today. Still see AUD going lower over the next year as the US tightens, China slows and EMs plus commodity prices keep falling.