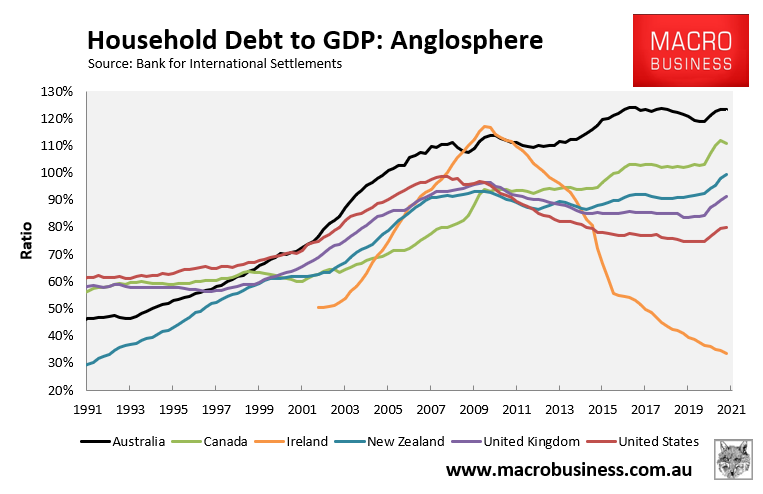

One of the inevitable ramifications of Australia having the second highest household debt load in the world (see next chart) is that Aussies are extremely sensitive to changes in mortgage rates.

Therefore, it should come as no surprise that new research from Canstar suggests that many Australian borrowers could be thrown into mortgage stress as rates rise:

Experts believe the inevitable rate rise will push many households into mortgage stress and signal the “beginning of the end” of the great COVID-19 house price boom.

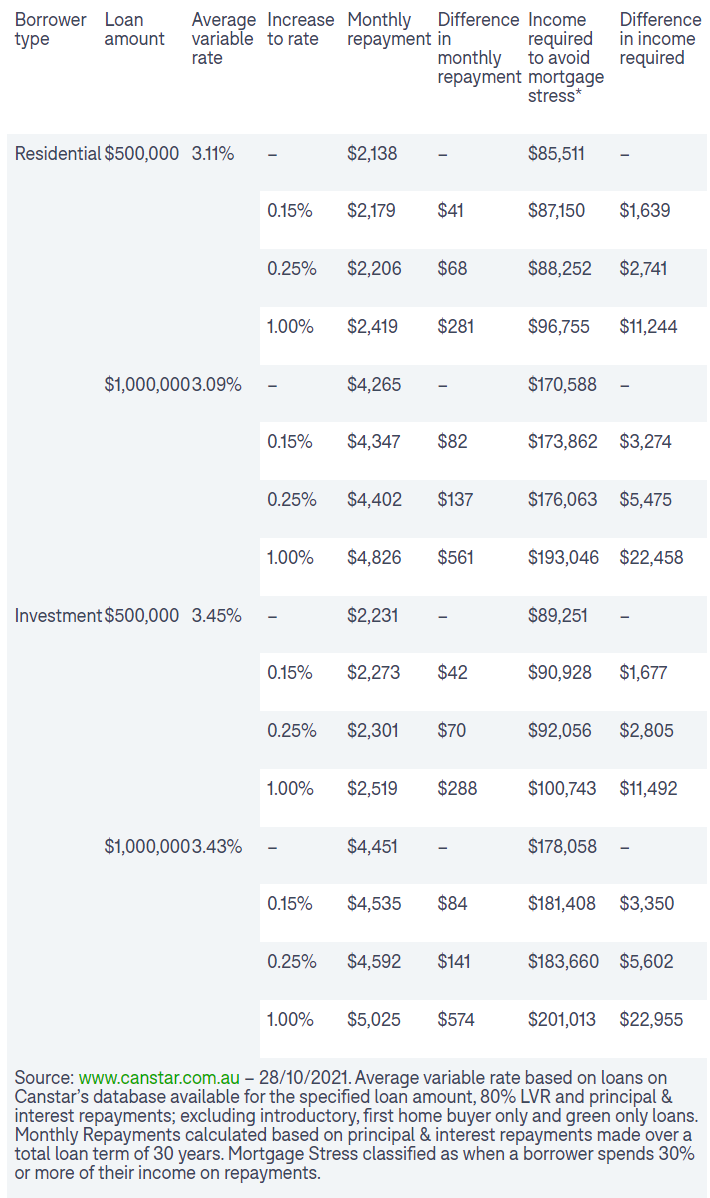

New analysis by Canstar shows that a 1 percentage point rise in the average variable interest rate of 3.09 per cent on a $1 million mortgage will see monthly repayments reach $4826 – or an extra $561 a month.

That means households will need $193,045 in income – or an extra $22,458 a year – to avoid mortgage stress, which is when a borrower spends 30 per cent or more of their income on repayments.

It is a similar story for investors, who would need $201,013 in income – or an extra $22,955 a year – to meet the monthly repayments on a $1 million mortgage without mortgage stress.

An increase of 1 percentage point on their average variable interest rate of 3.43 per cent would see the monthly repayment rise to $5025 – or an extra $574…

Canstar finance expert Steve Mickenbecker said borrowers should prepare for multiple interest rate increases in the next few years…

Talks of earlier-than-expected rate rises signal “the beginning of the end” of the boom, according to Shane Oliver, AMP Capital’s chief economist…

EY Oceania chief economist Jo Masters said the days of rock-bottom rates were over.

Advertisement

I am still not convinced that mortgage holders are facing a near-term rise in rates.

The RBA has explicitly stated that interest rates will not rise until inflation is sustainably within its 2% to 3% target range. It has less explicitly explained than it does not expect this to occur until there is wages growth of at least 3% across the economy. Thus, the trigger for the RBA to lift interest rates will likely hinge on wage growth.

We know that policy makers are itching to reboot the mass immigration program at the earliest opportunity, which would crush wage growth (and therefore inflation). We also can expect commodity prices to tank next year (crimping national income and the federal budget), and for dwelling construction to decline sharply (offset by strong infrastructure spending).

Advertisement

Thus, rather than be alarmist on inflation and interest rates, I am far more cautious and believe in a ‘wait and see’ approach.

Sure, we sill likely see some imported (cost-push) inflation from supply chain bottlenecks and energy. But the RBA will likely look through these impacts when determining rates, since they are likely to be transitory. There is also little point in raising rates (a demand management tool) to solve an imported supply-side shock.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.