ANZ-CoreLogic has released its 2021 housing affordability report, which shows that the barriers to buying a home in Australia has worsened materially following rapacious price growth and a sharp rise in the time taken to save a deposit:

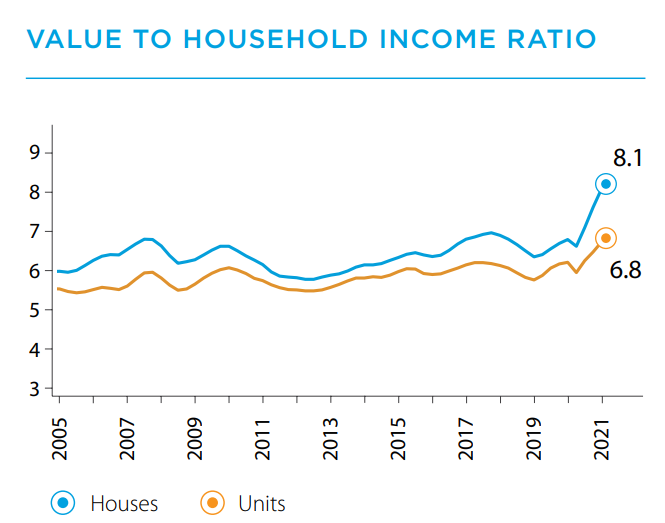

The national dwelling value to income ratio reached a record high 7.7 in the June quarter 2021. The ratio is sitting above the decade average of 6.3, and is up from 6.4 in the September 2020 quarter, when housing values had been mildly dampened by national stage 2 restrictions in response to COVID-19.

Growth in the value to income ratio has been sharper across houses than units, leading to the widest gap in the ratio on record between houses and units. Between March 2020 and June 2021, the value to income ratio for Australian houses has increased from 6.7 to 8.1, while the ratio for units nationally has increased from 6.2 to 6.8…

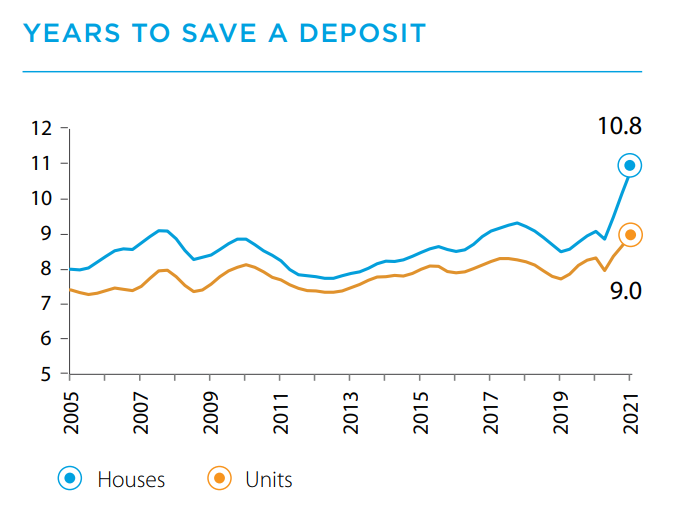

Based on households saving 15% of their gross annual income, it would take the typical household a record high 10.2 years to save a 20% deposit for an Australian dwelling at the end of June quarter 2021. Record high savings periods are required across both Australian houses (10.8) and units (9.0).

The time taken to accumulate a deposit is a particularly important component of housing affordability for first home buyers…

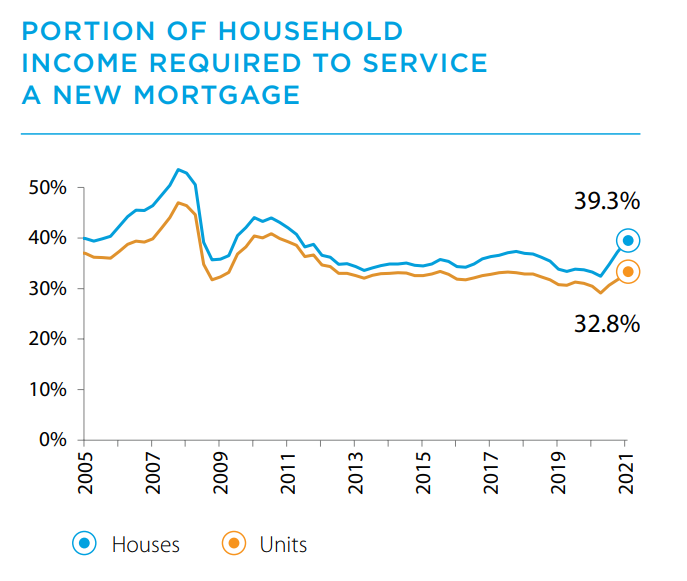

Unlike indicators of barriers to enter the housing market, mortgage serviceability has not blown out to record highs through the current upswing. This is due to the very low mortgage rate environment.

While not at record highs, the portion of income required to service a mortgage nationally has increased since the housing market bottomed out through the September 2020 quarter…

The portion of income needed to service a new mortgage on Australian units was 32.8%, up from a recent low of 29.1% at the end of the September 2020 quarter…

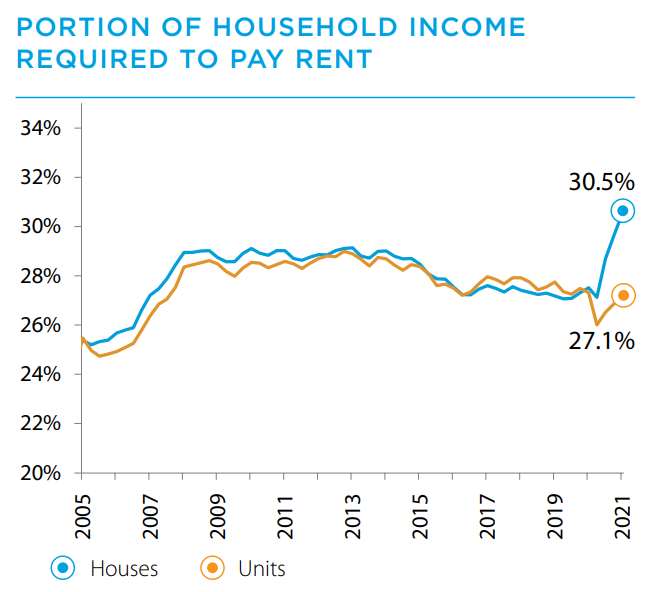

Through the June 2021 quarter, median dwelling rents remained lower than the portion of income required to service a mortgage at 29.4%, despite this being the highest percentage on record. Over the past decade, median rent costs have averaged 28.1% of median income, and the latest reading has risen from a recent low of 26.8% in the September 2020 quarter…

The report also shows how home ownership has fallen over the years. Basically, the younger you are, the less likely you are to own a home:

Home ownership rates fell across all age groups over the past three decades. Whether you were born in the mid-to-late 50s and you’re now heading into retirement, or are a potential first home buyer born in the late 1980s, the likelihood that you own your own home is lower than for those just 5-10 years older and significantly lower than if you were born three decades earlier. But the declines have been the largest for younger people in the typical first home buyer ages between 25 and 34 years. The 2016 census showed that 50% of 30-34 year olds owned their own home, down14pptfrom 64% in 1971. A similar drop was evident for 25-29 year olds, where home ownership dropped from 51%to 37%over the same period.

Advertisement

When we talk about ‘housing affordability’, the focus should really be on the ability of first home buyers to enter the housing market and pay-off their homes. Their situation has gotten objectively worse, as evident by:

The long-term decline in home ownership among under 35s;

The huge deposit required to obtain a mortgage;

The big rise in the ‘bank of mum & dad’; and

The casualisation of the work force, rising labour underutilisation, and low wage growth.

While it has never been cheaper in aggregate to service a mortgage, it has also never been more expensive to save for a deposit or pay off the loan.

Advertisement

Because inflation and wage growth are low, and house prices are high, mortgage debts will not be ‘inflated away’, and it will take the typical home buyer many decades to repay their loans.

This means that many Australians will now carry mortgages deep into their retirement.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.