Westpac with the note:

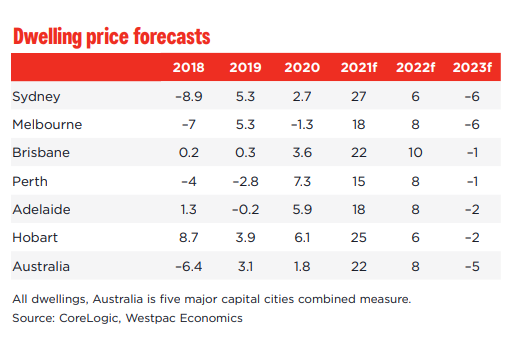

We have upgraded our forecasts for Australian dwelling prices. Markets continue to show very strong momentum with only a slight dampening effect from the latest COVID lockdowns. We now expect a 22% gain for the full 2021 calendar year (up from our previous forecast of 18%).

We still expect momentum to slow considerably through 2022 as stretched affordability combines with macro-prudential tightening measures and, later in the year, the anticipation that the Reserve Bank will begin a tightening cycle in early 2023 begins to weigh on confidence. The combination of high levels of new building and slow population-driven demand may also weigh on some sub-markets.

Overall, price growth is expected to slow to 8% in 2022 (up from our previous forecast of 5%), with most of that increase loaded into the first half of the year.

We confirm our previous views that markets will move into the first year of a correction phase in 2023 as official interest rates rise, with prices forecast to retrace by 5%.

Prices tracking towards a big gain for 2022

Australia’s housing markets are again outperforming expectations. Prices have continued to post strong gains despite recent extended lockdowns in NSW, Victoria and the ACT. Even in the most heavily affected markets of Sydney, Melbourne and Canberra, price growth has sustained a strong double-digit annual pace. With reopening in sight, dampening effects of lock downs will now drop out of the picture.

That points to a very strong 22% gain for the full calendar year. Prices across the major capital cities are already up 17% over the year to September and are tracking for a 1.5% gain in October. We expect reopening boosts to more than offset any initial drags from recently announced macro-prudential measures. As such a further 3% gain over the last two months of the year is likely, bringing the cumulative rise to 22% for the full year.

This strong momentum will carry into 2022. However, the pace of gains is expected to slow, levelling out over the course of next year before moving into a correction phase in 2023.

As always there are many moving parts to the price outlook. The main ones relate to affordability and policy tightening by both the Australian Prudential Regulatory Authority (APRA) and the RBA.

The wild cards are around investor activity and potential impacts from an extended period of slow population growth.

Affordability deteriorating quickly

On affordability, prices are now moving into stretched territory. The Sydney and Melbourne markets are, respectively, 18% and 10% above their previous price peaks in 2017-18, a time when both encountered major affordability problems. The Brisbane and Perth markets are also well above their 2017-18 levels although these markets were not stretched during this earlier period – for Perth, current pricing still looks benign, particularly when compared to the extremes reached during the mining boom.

Many other capital city and regional markets are also recording high prices by historical standards.

Of course, price alone does not determine affordability. Our preferred measure looks at the proportion of income required to purchase a median-priced dwelling, including accumulating a deposit over a five year pre-purchase period and making mortgage repayments over the first five years of the loan. This shows that even with the sustained move lower in mortgage interest rates affordability is becoming very stretched at current price levels with the three major eastern capital city markets back near the extremes seen in 2017, 2018, 2004 and 1989.

Macro-prudential policy tightening coming into frame

This clearly cautions against further upside to prices. However, as we have noted previously, stretched affordability driven by prices alone is not usually sufficient to drive a meaningful market slowdown. This instead almost always comes from a combination of stretched affordability and policy tightening.

That ‘policy trigger’ for a slowdown is now coming into play. Last week’s move by APRA – lifting the buffer rate applied to loan serviceability assessments from 2.5% to 3% – marks the first step in what we expect to be an incremental tightening in ‘macro-prudential’ policy (MPP) aimed at restraining credit growth and housing market activity.

The shift on MPP has come a little earlier than expected – before the full scale of the ‘delta’ shock has been confirmed and ahead of reopening, signalling a degree of urgency.

That said, the initial measure does not look to be particularly heavy handed. The RBAs own Financial Stability Review (FSR) released on October 8, assesses that “the direct effect on the flow of new credit is likely to be moderate.” The move is estimated to reduce maximum loan sizes by around 5% but the flow on effect is likely to be a lot smaller given that there will be smaller changes to serviceability assessment rates where ‘floor’ rates have been used and given that over 80% of borrowers are not borrowing at the maximum amount available.

Note that the rate used in serviceability tests is the higher of: 1) the loan rate plus buffer; or 2) the minimum floor rate, and is applied to all of the borrowers’ debt not just the loan being considered.

The FSR also makes it clear that we can expect more measures down the track. It notes that “over time, if the extent of systemic risk changes, then the MPP settings may need to be adjusted, as has frequently been the case internationally.” While that could be read as an easing in systemic risk and a relaxation of MPP settings, the more likely implication – informed by experiences abroad – is that further tightening measures are likely to be required.

On this, the Bank appears to favour restrictions on a combination of high debt-to-income (>6x) and high loan-tovalue (LVR>80%) loans, possibly with less stringent criteria applied for first home buyers. One clear implication is that MPP tightening is likely to lead to a more complex landscape for borrowers and lenders, meaning impacts will also become more difficult to assess. The risk of ‘unintended consequences’ is also high – tighter restrictions for example are likely to drive more borrowers to more lightly regulated non-bank lenders and could see an increase in riskier lending.

The timing of any further moves is uncertain but is likely to be from early 2022. The RBA’s FSR acknowledges that it could take several months for the full impact of the serviceability adjustment to become apparent. It may also take time for concerns about the lending mix to come to a head, with APRA’s figures on loans by debt-to-income and loan-to-value band only published quarterly. With the Christmas-New Year hiatus putting markets largely on hold over December-January, that suggests the next window for action is from February next year.

With opinions firming towards a March Federal election, the timing of the next stage of controls is further complicated.

MPP tightening was reintroduced in New Zealand by the Reserve Bank of New Zealand (RBNZ) in March 2021 the share of owner-occupier loans with LVRs above 80% capped at 20% and the share of investor loans with LVRs above 70% capped at 5%. These were tightened again in May – the investor LVR cut-off lowered to 60% – and in September with the cap on owner-occupier loans above 80% LVR lowered to 10% (to come into effect from November). These policies are assessed to have taken 2-5ppts off price growth while also impacting

turnover. Readers will be aware that the RBNZ has also started its tightening cycle with a 0.25% increase in the overnight cash rate in October.

On balance we expect MPP measures to have a similar impact on the Australian market, taking some of the heat out but lowering price growth by a few percentage points rather than driving a sudden stop.

Timing of RBA’s next tightening cycle remains key

The more meaningful policy-related headwinds centre on the next interest rate tightening cycle and are likely to emerge over the second half of next year.

As we have noted elsewhere, Westpac expects the RBA to achieve its key policy objectives – full employment, a lift in wages growth and inflation back at the middle of the 2-3% target band – by the end of next year, setting the scene for the beginning of an official interest rate tightening cycle in 2023. This is earlier than the Bank itself currently expects, with the RBA Governor indicating that the preconditions for interest rate increases are unlikely to be in place before 2024.

The RBA’s view will help sustain housing market gains near term. However, that will shift as it becomes clearer that rate rises are coming onto the agenda much earlier. Some of this will come in the form of an actual tightening in financial conditions as anticipated moves lift term rates and fixed mortgage rates through the second half of the year.

Markets have recently moved to reassess the outlook for interest rates significantly in response to increases in rates globally with 3-4 rate hikes now priced in for 2023 – slightly ahead of Westpac’s forecasts.

The combined effect is expected to see prices flatten out completely towards the end of 2022, albeit with solid momentum at the start of the year still seeing a decent 8% gain for the year as a whole.

As we move into 2023, the impact of the RBA’s tightening cycle will weigh more heavily on housing markets as borrowing capacity is impacted directly and as sentiment turns, with a tightening cycle seen as offering little scope for further price gains.

That is expected to see markets move into a price correction phase with prices retracing 5% in 2023. While that might seem mild in the context of the preceding run-up, it usually takes a bigger convergence of negatives to drive more material price declines – typically a contraction in the availability of credit and/or a recession event that results in a wave of urgent sellers discounting prices into a market with weak demand. Nation-wide annual price declines of over 5% are quite rare – seen during the 2018-19 correction, the GFC and briefly in the early 1980s.

Risks centre on investors and supply-demand balance

Within this narrative, there are two other areas that bear particularly close watching: investors and the physical supply demand balance.

Investors have remained cautious through the housing market cycle to date, accounting for just 25% of the value of loans over the last 12mths. That compares to the previous cycle when this segment accounted for close to 40% of loans over 2015-17. That has shown signs of shifting in 2021, with the segment share lifting towards 30% – a shift that is to be expected when prices are rising, with investors less sensitive to deteriorating affordability.

Affordability drivers will see investors become more prominent over the next year. If we were to see a more meaningful pick-up in investor activity, that could drive stronger and more persistent price gains near term but may also result in a more material correction from 2023. The effectiveness of MPP measures on investors will be important. APRA imposed speed limits on investor credit growth in 2014 and a cap on the share of interest only loans in 2017 while more recently we have seen the RBNZ put tighter caps on the share of high LVR investor loans.

Expectations of capital gains and rental yields will also be important factors for investors. The Westpac Melbourne Institute Index of House Price Expectations remains very bullish, near eight year highs despite some softening in recent months.

On the physical supply-demand balance, the extended period of closed borders has dramatically reduced population growth. That is coinciding with a surge in new building, supported by both low interest rates and the Federal government’s highly effective HomeBuilder scheme. There are likely to be around 200k new dwelling completions in 2021. That is more than double the annual increase in physical requirements we are seeing with slow population growth.

The prolonged period of underbuilding that preceded the latest building cycle means markets are coming into this with an accumulated deficiency of dwelling stock. And so far, the combination of strong building and slow population growth has not resulted in significant overhangs of stock except in a few specific sub-markets –rental vacancy rates for example remain tight in most markets, Melbourne, with vacancy rates at 5.7%, the one notable exception. However, that may shift as new completions come through, particularly if, as we expect, a return to significant net migration inflows is slow to come through.

Conclusion

While the market upturn has weathered the latest COVID disruptions very well and is clearly carrying strong momentum, the boom is entering trickier territory. Affordability is becoming stretched and policy tightening is now in play. Price momentum has held up near term prompting us to revise up the near-term outlook for prices.

However, we still expect the market to slow over the course of 2022 as MPP; prospects of increased rates; and affordability reaching record lows triggers a correction phase that will begin in 2023 and is likely to extend into 2024.