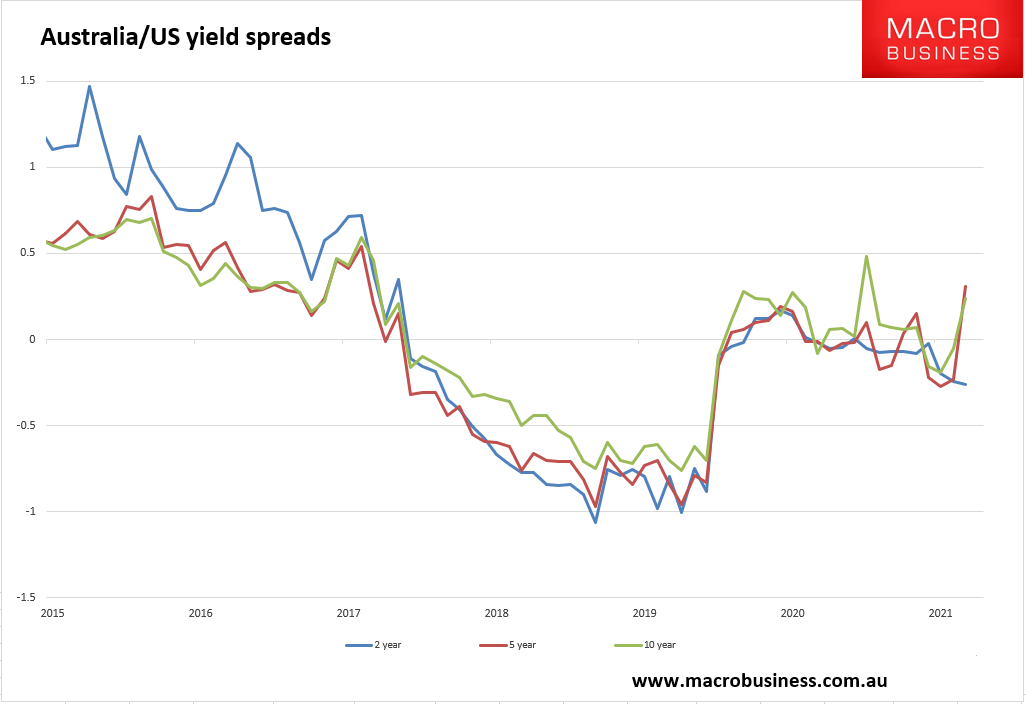

Yesterday’s Aussie bond action was borderline hysterical as the belly of the course threatens to jackknife into inversion with the long and the RBA’s yield curve control has been obliterated:

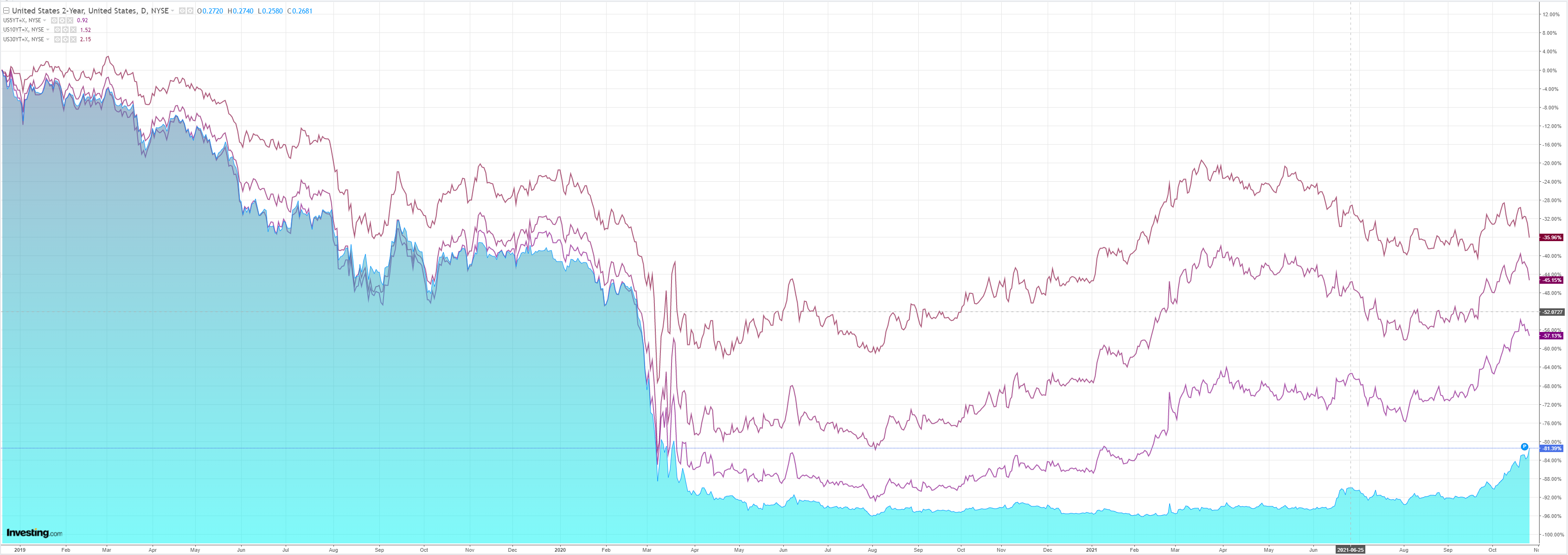

The US curve was also crushed though its long-end was bid impressively:

Advertisement

Spreads to the US blew out at the longer end putting upwards pressure on the AUD: