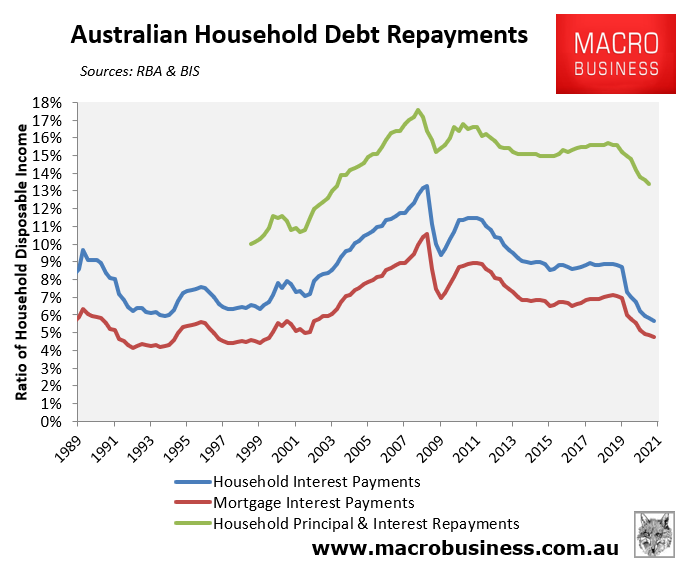

The latest quarterly data from the Reserve Bank of Australia (RBA) and the Bank for International Settlements (BIS) showed that household and mortgage debt repayments as a ratio of incomes fell to their lowest level in decades, brought about by the collapse in mortgage rates:

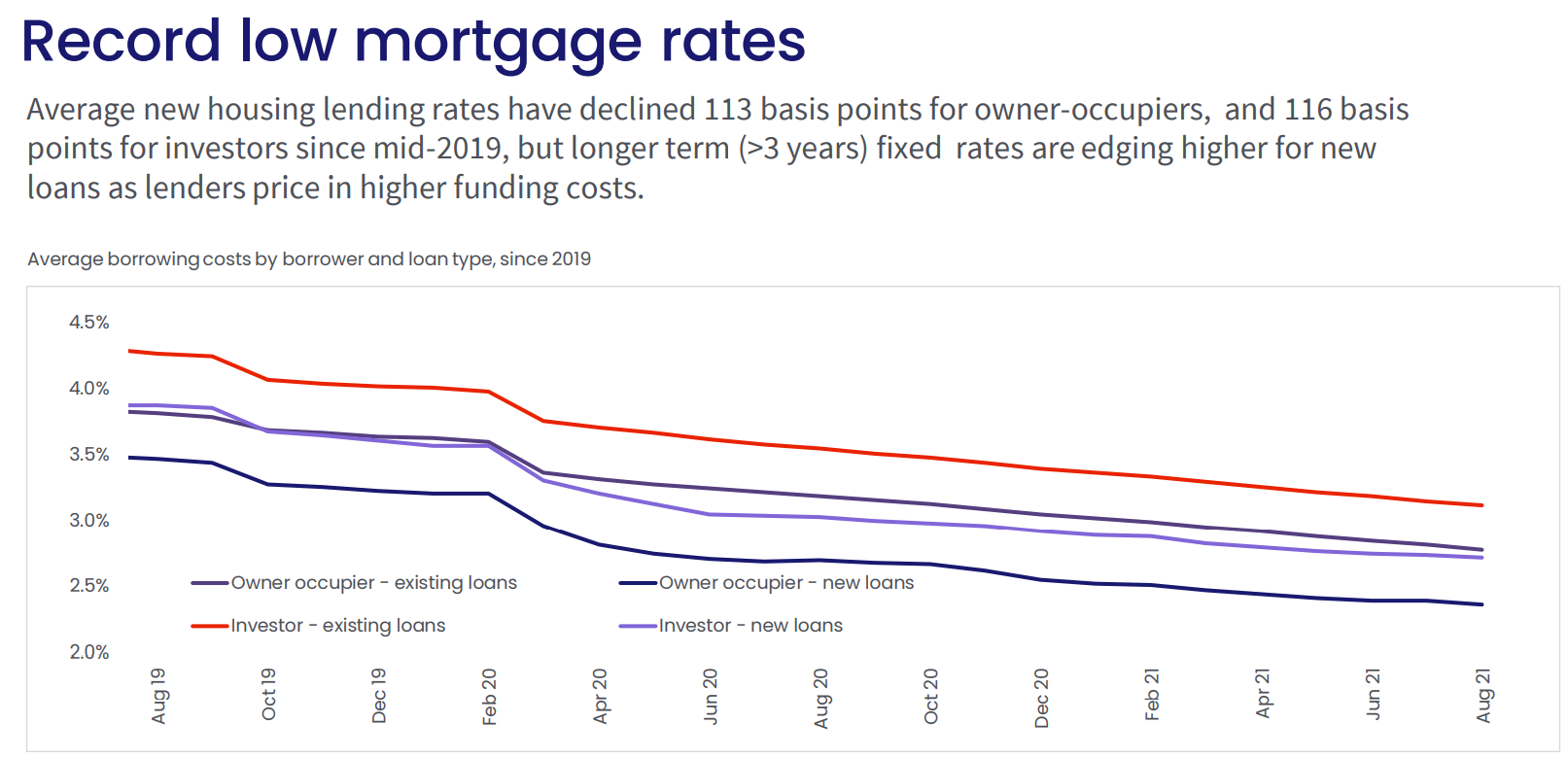

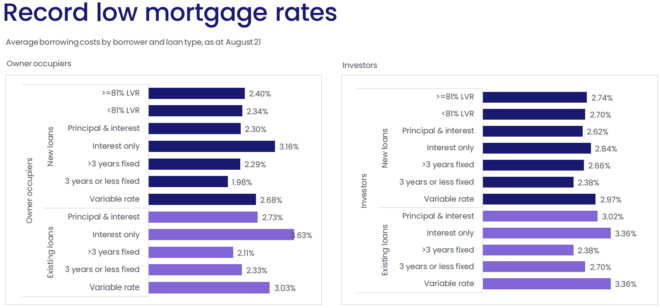

The below graphics from CoreLogic, which are current to August 2021, show the dramatic fall in mortgage rates across different loan terms:

Yesterday, Westpac was the latest big four bank to raise its fixed mortgage rates, suggesting we may have passed the bottom of the rate cutting cycle:

[Westpac] announced it would be increasing its two, three, four and five-year fixed rates by 0.10 per cent for new owner-occupied loans paying principal and interest repayments.

That follows in the footsteps of CBA, who hiked its two, three and four-year fixed rates by the same amount last Friday…

RateCity.com.au’s research Director Sally Tindall said the big banks are anticipating lending to become more expensive, despite no early indicators from the Reserve Bank of Australia (RBA).

“While the RBA is insistent the next cash rate hike won’t be until at least 2024, the banks are anticipating an increase to the cost of funding once borders reopen and the economy rebounds,” Ms Tindall said.

“While today’s fixed rate hikes from Westpac are relatively small, people in the queue for a home loan, who didn’t lock in their rate, will understandably be annoyed.”

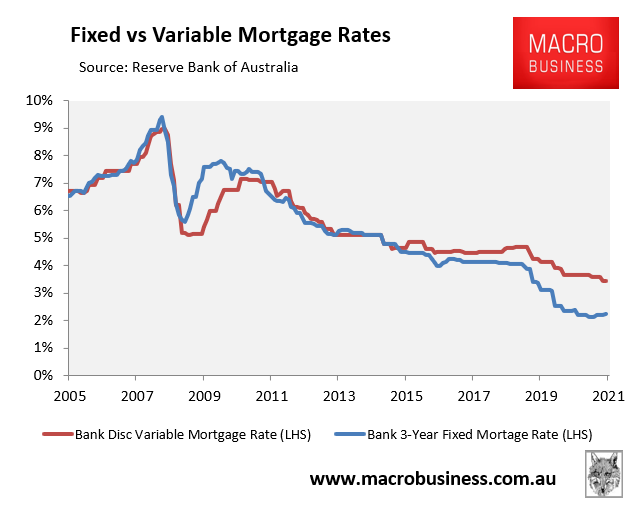

The latest lending indicator data from the RBA showed that average 3-year fixed mortgage rate ticked up a further 4 basis points to 2.23% in September:

This meant that average 3-year fixed mortgage rates are now tracking 9 basis points above their record low of 2.14% in April 2021.

This may be as good as it gets for borrowers with average mortgage rates likely to drift higher from here, alongside tighter loan eligibility arising from APRA’s macro-prudential mortgage restrictions.