Wall Street fumbled again overnight as concern over rising energy prices and inflation continued to weigh on stock markets with European equities also mixed despite a much lower Euro. USD remained relatively strong against most of the major currencies, particularly Yen but commodity currencies like the Australian dollar are rallying as 10 year Treasury yields pushed through the 1.6% level for a new six month high. Meanwhile the commodity juggernaut continued with oil and copper up 2%, the former to a three year high, gold unchanged and iron ore zooming more than 9% after a week long trading break.

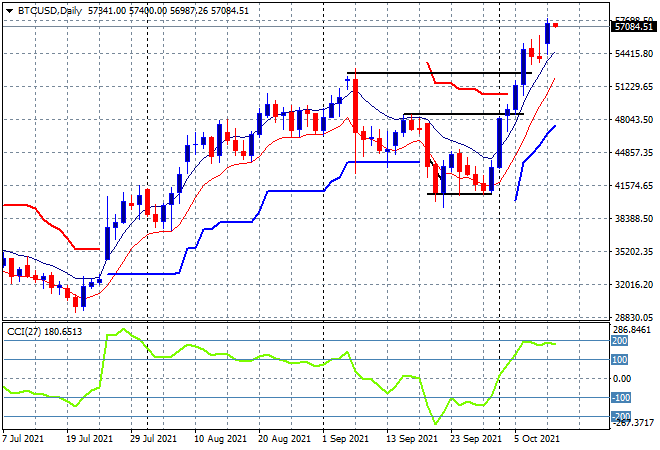

Bitcoin inched higher on its breakthrough, lifting just above the $57K level this morning after a minor retracement that had consolidated its recent new monthly high. The daily chart shows how price is well above the August highs with momentum readings still looking good, if a little overstretched. The next move is likely to be the previous historic highs above the $60K level but watch for support that must hold here at the $50K level:

Looking at share markets in Asia from yesterday’s session, where Shanghai Composite was up nearly 0.5% at one stage, back above the 3600 point level but lost ground to close dead flat at 3591 points while the Hang Seng Index followed through on its previous surge, up 2% to close at 25325 points. This breakout above the high moving average has continued after basing for more than a week as the return of mainland markets proved a solid catalyst to get things moving, but price action must get past that medium term downtrend line at the 25000 points level for a follow through:

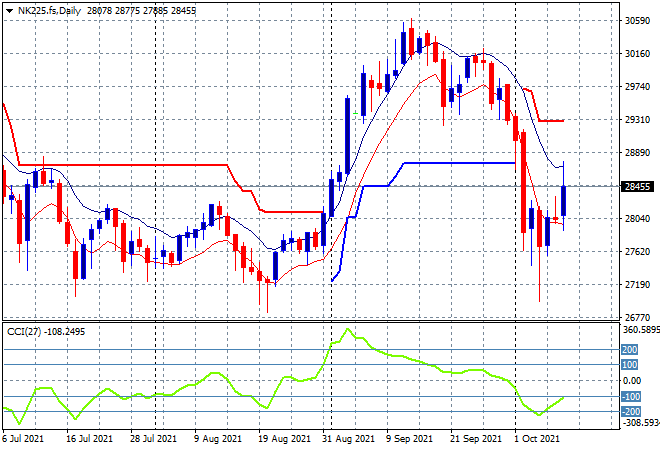

Meanwhile Japanese markets continued to find strong bidding support with a 1.6% gain by the Nikkei 225 to close at 28498 points. The daily chart is trying to paint a more promising picture but thats a steep ditch to climb out of despite a very weak Yen run at the moment. Note that price action is not yet above its own high moving average and while momentum readings have retraced from their oversold levels, its still nowhere near positive. I remain cautious here to see how how this swing plays out:

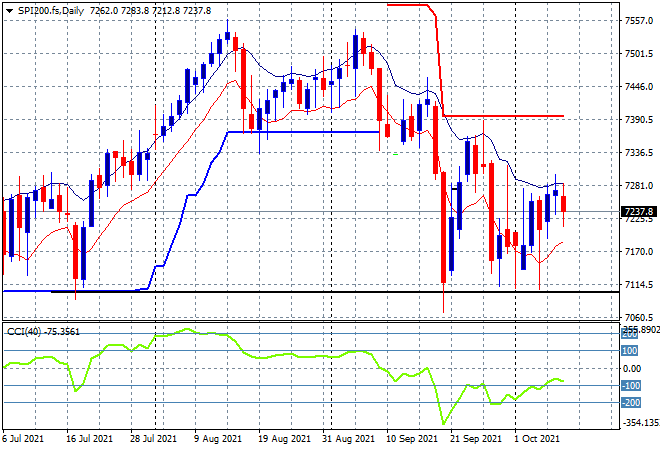

Australian stocks were the odd ones out and the losers even as freedumb NSW opens up, with the ASX200 closing 0.3% lower to 7299 points. SPI futures are down over 30 points given the misstep on Wall Street overnight, with a wider pullback likely on the open as the Aussie dollar soars higher. Remember that in the medium term, monthly support at the 7000 point level remains key here with daily price bunching up but not yet able to break above the high moving average but momentum is ready to get out of the oversold stage. Watch for a proper breakout above the 7300 level before getting excited:

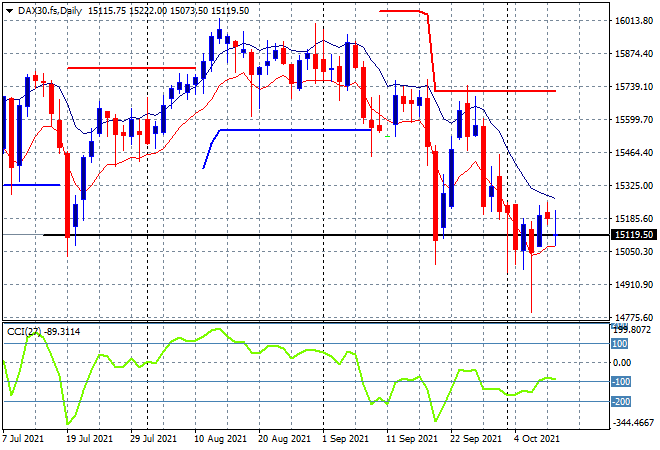

European markets were mixed again with the FTSE and French CAC lifting, while the peripheral markets and German DAX continued to wobble, the latter finishing a handful of points lower at 15199 points, just holding on above the key 15000 point level. The overall picture remains quite bearish, with price oscillating around weekly/monthly support at the 15000 point level and has not yet set up for a proper selloff, still indicating a possible bear trap, although those bears are getting frisky. Watch the high moving average at the 15300 point level for signs of a swing higher, but this market and indeed the whole continent will likely follow Wall Street first:

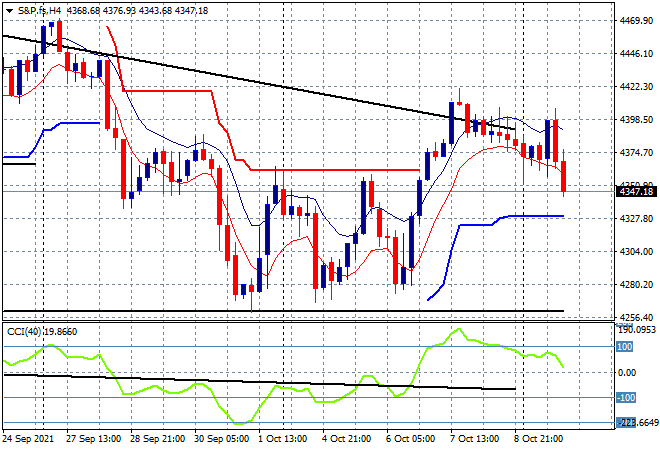

Wall Street pulled back across the board with the headline Dow, NASDAQ and the S&P500 all finishing 0.6 to 0.7% lower, the latter closing at 4361 points. The daily chart shows how the expected follow through after bouncing off monthly support at the 4250 point level has not eventuated, as price action head back below the daily downtrend line from the August highs. We’re in some very murky waters ahead here – I still contend the BTFD crowd is still around the corner so watch for any signs of buying pressure to push the market back above 4400 points:

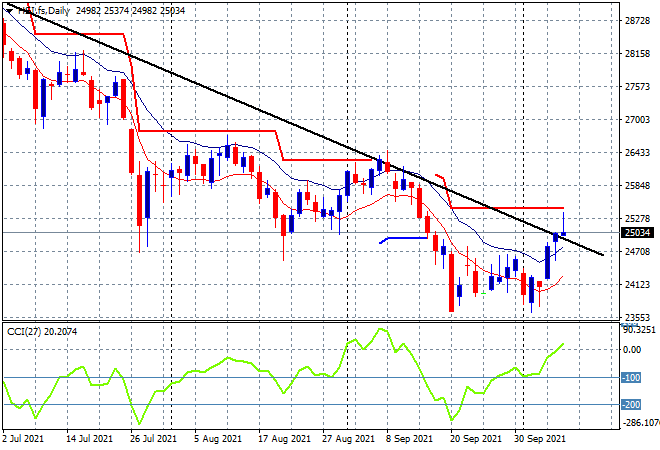

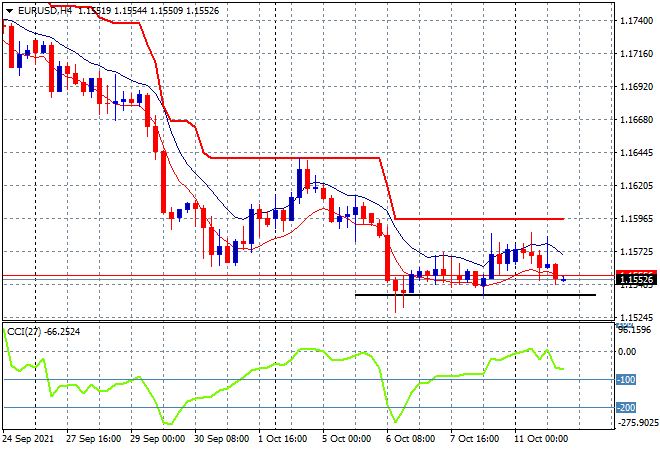

Currency markets reduced volatility levels from their Friday night machinations with the USD remaining quite strong against the majors as Euro is still depressed here at the mid 1.15 level as it retraces back to the newly made weekly and monthly lows. The union currency remains the one not to bid for now with price unable to go anywhere near overhead trailing ATR resistance:

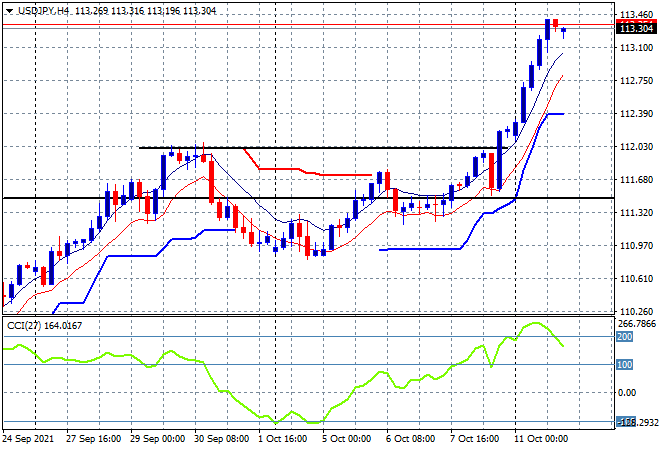

The USDJPY pair continued its push higher to break through the 113 handle to a new three year high. Its a very straightforward technical picture that in the short term is way overdone with the growing chance of a pullback to the lower 112’s as momentum goes extremely overbough, but medium term the 112 handle itself should prove a very sound Uncle point going forward:

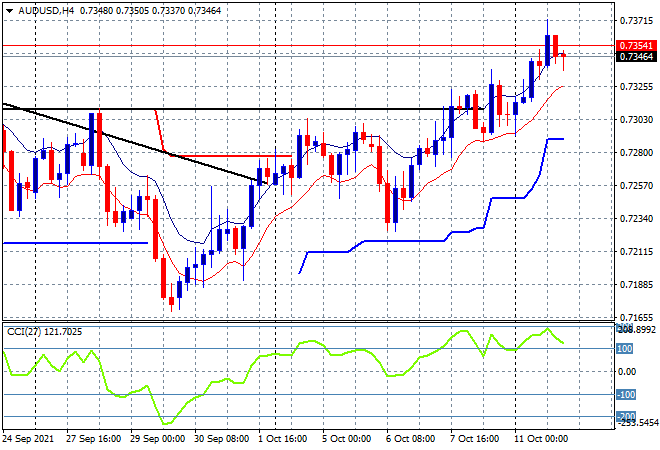

The Australian dollar is leading alongside commodity markets with a nice uptrend through the 73 handle and into the mid levels overnight as the iron ore price returns to burst higher again. My idea of a breakdown following the return of those Chinese markets has been proven wrong (strong opinion, weakly held remember!) as price remains above the previous weekly highs (solid black upper horizontal line):

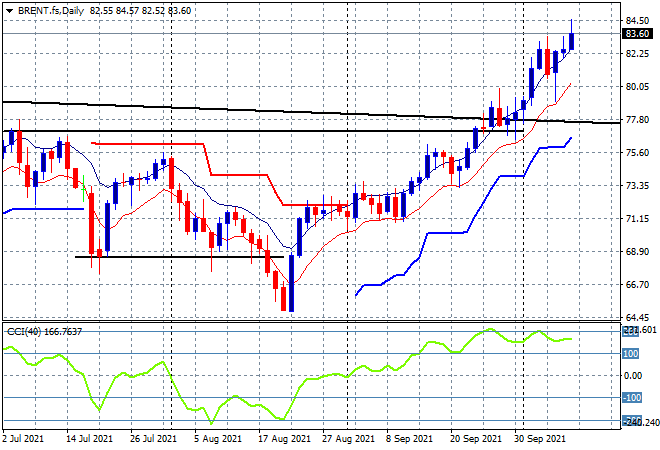

After being well contained on Friday night, Brent crude futures have launched some 2% higher for a new three year high, hitting the $84USD per barrel level briefly. Without much heat taken out of recent price action, the rally continues with strong momentum readings as it clears the medium term downtrend. My contention of a possible retracement is unlikely although a move to the low moving average at the psychological $80USD per barrel level is something to watch for on a blowout:

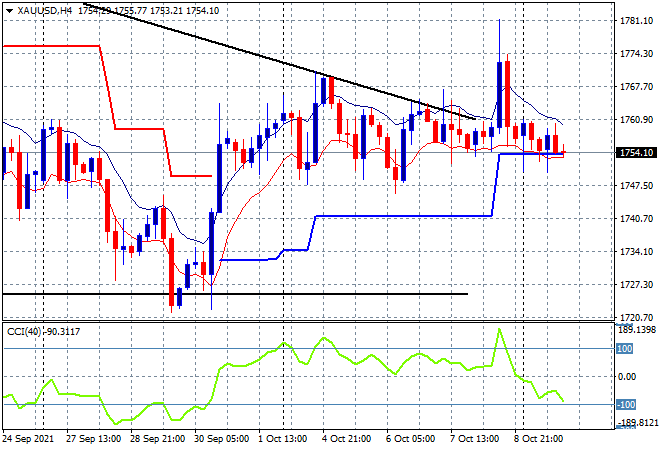

Gold’s major false breakout on Friday night is still reverberating here with price now pushed down to the $1750USD per ounce level at trailing ATR support as momentum completely abandons the shiny metal. The inability to break through the downtrend line from the early September rout belies the previous buying support that I thought had been building, so watch for a potentially big move lower soon:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out!