TSLombard with the note:

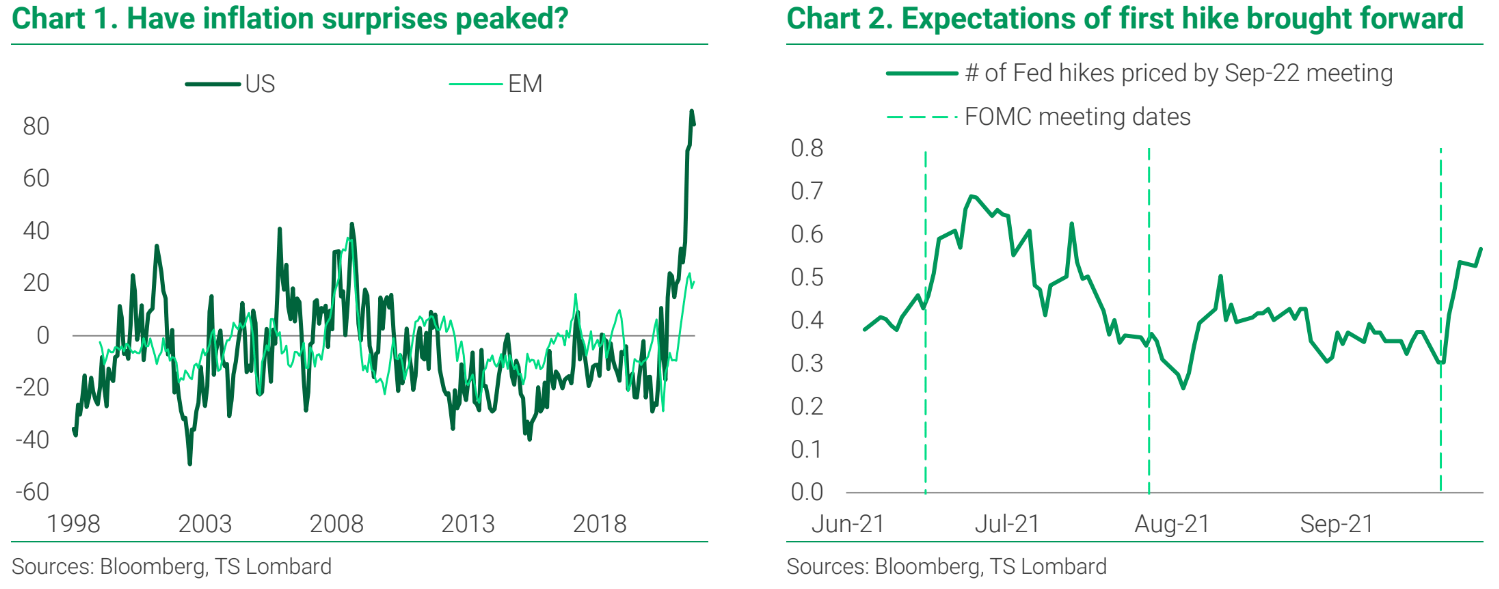

The new piece of information investors received from the FOMC meetinglast week was not about the taper, which the Fed had telegraphed extensively.What caught themarket by surprise wasthe hawkish tone and the higher policy rates projections in the dot plot. The 2021 fed funds rate median projection was hiked to 0.3% from 0.1% and the 2023 from 0.6%to 1.0%. Additionally,the figure for 2024 was 1.8%:this wasa huge jump from thepreviousannual projectionof 0.6% for 2023. The longer-run rate was unchanged at 2.5%.

We think the 2023projectionisthemostsignificantfor markets.The projection for 2024 lookshighbut thereareno comparable data, so ittells us nothing about how the Fed’s thinking mayhave changed. And the 2022 number is now indeed higher thanit was in June, butit has increased in line with higher inflation expectations (PCE went from 2.1% to 2.3%), implying asimilar reactionfunctionthis time round. However,the 2023 projection rose 40bp, despite a 10bp increase in PCE (from 2.1% to 2.2%). Is the Fed turning more hawkish?