Westpac with the note. Given the recession and now reopening, this looks more like a trailing index, no?

This is the first negative read – signalling below trend growth – since September last year when the economy was moving out of COVID lockdowns. In the following months of October, November, and December the Index surged to 4.5%, 5.0% and 5.2% respectively, signalling a strong recovery.”, Mr Evans commented.

This time, September 2021 marks the last full month with both Sydney and Melbourne locked down. As these cities begin reopening in October and November, we can expect another strong rebound in the economy. Moreover, this recovery is not expected to be disrupted by the various state snap lock-downs that dogged the previous recovery through much of late 2020 and early 2021.

Westpac expects the economy to expand by a solid 1.6% in the December quarter building towards a 5.6% surge in the first half of 2022.

As we saw in 2020, the Leading Index is likely to recover quite quickly as Sydney and Melbourne reopen, consistent with that strong outlook for the first half of 2022.

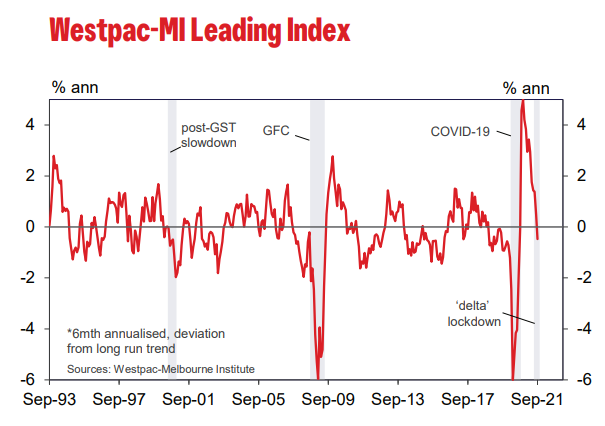

The Leading Index growth rate has fallen steeply over the last five months, from 2.9% in April to–0.5% in September. All components have contributed to the turnaround, most seeing sizeable drags.

About a percentage point of the 3.4ppt fall has come from a sharp turnaround in hours worked, which has swung from robust reopening-driven gains over the six months to April (+3.4%) to another lockdown-induced contraction (–3.5% since April).

A move lower in dwelling approvals (–0.5ppts) and a flattening in the yield spread as bond rates have edged lower (–0.5ppts) over the April-September period also contributed to the fall.

Other contributions came from falling commodity prices (–0.35ppts), down 10% in AUD terms since July; slower gains in US industrial production (–0.33ppts); and a move lower in the S&P/ASX200 (–0.30ppts).

Confidence measures have taken a further half percentage point off the headline growth rate, the Westpac-Melbourne Institute Composite Expectations Index down 12.5% from April’s high and the Westpac-Melbourne Institute Unemployment Expectations Index deteriorating 6.9% since May.

The Reserve Bank Board next meets on November 2. The Board will hold the line on its current policy settings with the next policy change to be a review of the weekly bond buying quota at the February meeting. Westpac expects that the quota will be reduced from $4 billion to either $2 billion or $3 billion.

The minutes from the RBA Board’s October meeting were highlighted by reports of a discussion that “underlying inflationary pressures in Australia could build more quickly than currently envisaged”.

The Board’s current forecast is that underlying inflation will only reach 1.75% by end 2022 and 2.25% by end 2023. The Governor’s clear statement that underlying inflation will need to sustainably reach the middle of the 2-3% band before the cash rate is increased explains why the Bank is not forecasting a move until 2024.

Since June 18 Westpac has argued in favour of an earlier move, in the first quarter of 2023, on the basis that underlying inflation will achieve this target by late 2022.

Markets have recently become even more adventurous, pricing in rate increases in the second half of 2022.

Accordingly, the most important aspect of the November Board meeting will be whether the Bank has lifted its inflation forecasts in the wake of developments around supply disruptions to labour and goods markets, including energy, interacting with the strong expected increase in demand.