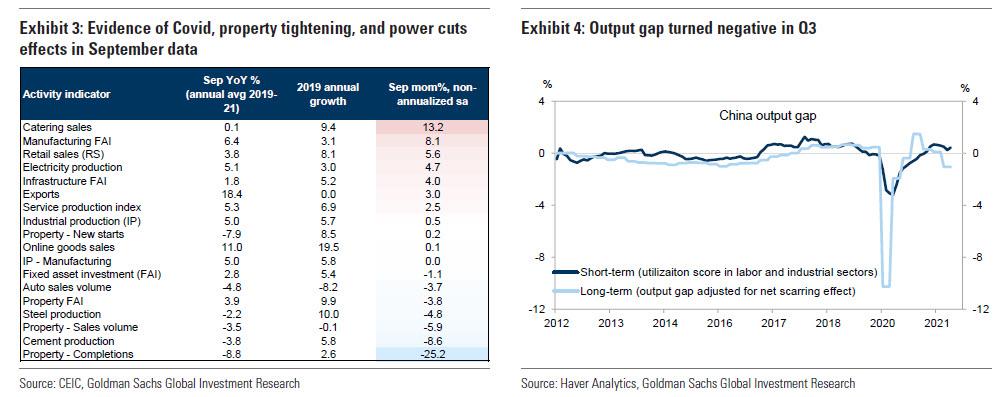

The weak Q3 growth was driven by a number of factors – Covid outbreaks and chip shortages that the government has less control over on the one hand, and property tightening and power cuts that are mostly policy-driven on the other. The September activity data show evidence on the combination of various shocks to the economy (fig.3) For example, catering sales (i.e., restaurant services) rebounded sharply in September after slumping in August on Covid lockdowns in multiple provinces. Auto production and sales remained soft on chip shortages. Property sales continued to drop on the government’s deleveraging efforts and lending restrictions. Output of high-emission products such as steel and cement fell sharply on the “dual controls” of energy use and severe coal shortages which led to power cuts and production halts in these sectors.

After the anemic sequential growth year-to-date (averaging only about 2% annualized rate), the Chinese economy appears to have gone from a positive output gap at the end of last year to some excess capacity in Q3.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.