Morgan Stanley is still making the most sense on Wall Street with daylight second:

Over the past few weeks we have discussed the increasing probability for a colder winter but a later start than previously expected. In other words, our Fire and Ice narrative remains very much intact, but timing is a bit more uncertain for Ice. Having said that, with inflation running rampant in bothc onsumer and corporate channels, the Fed is expected to formally announce its tapering schedule at next week’s meeting with perhaps a mor ehawkish “tone” to convince markets they are on the job. In other words, the Fire portion of our narrative (higher rates driven by a less accommodative Fed spurs multiple compression) is very much in gear and is a f ocus for investors.

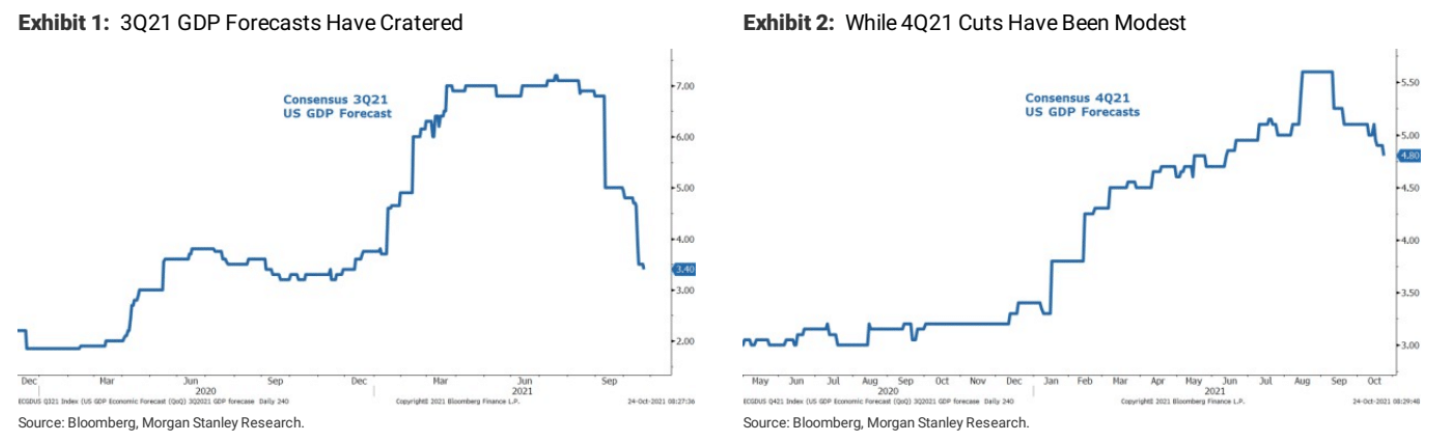

With so much attention on rising inflation now from both investors and the Fed, we shift our attention to the ongoing macro growth slowdown and when we can expect it to bottom and reverse course. As noted for months, we have been expecting a material slowdown in both economic and earnings growth amid a midcycle transition. The good news is so does the consensus as illustrated by the sharp declines in 3Q21 economic growth forecasts (Exhibit1). While 4Q21GDP forecasts have also declined, the expected growth rate is higher than 3Q—i.e.,the street expects growth to reaccelerate from here (Exhibit2). Most have blamed the Delta variant, China’s crackdown on real estate or power outages around the world for the economic disappointment in 3Q with the assumption all three will get better as we move into year end and 2022.