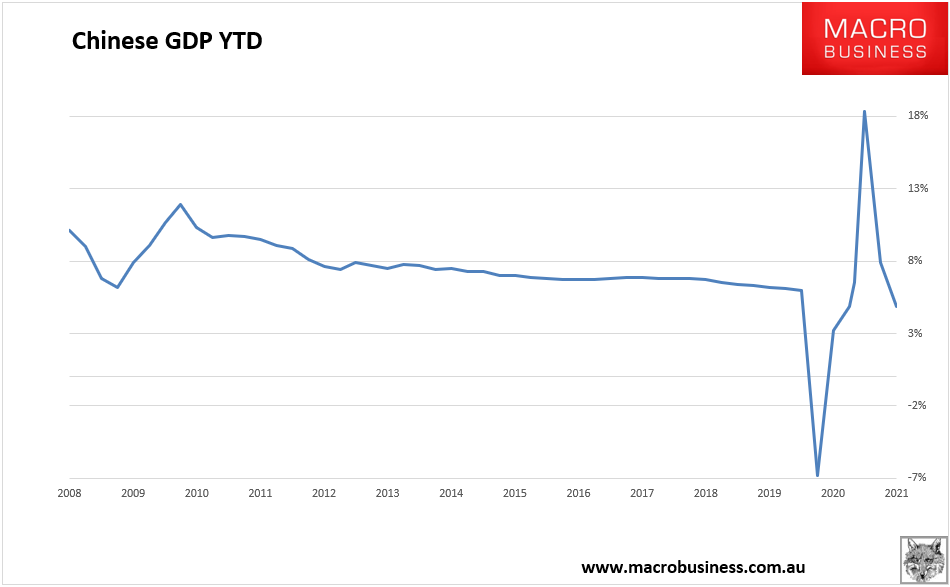

Chinese September monthly data is out and missed bigly. Sept QTR barely grew at 0.2% and YTD is down to a 4.9%:

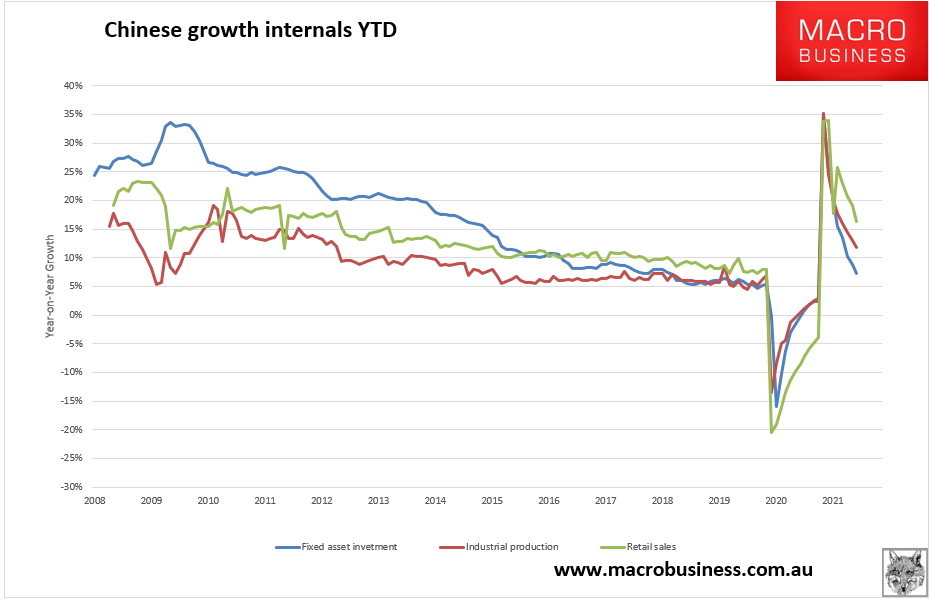

Under the bonnet and monthly data is noteworthy for two reasons. Firstly, growth has stalled out as it is hit by the combined property and power shocks. YoY industrial production is a lousy 3.1%, YTD 11.8%. Fixed asset investment is a decent 7.3% but sliding fast. Retail sales were pretty crappy at 4.4% Yoy and 16.4% YTD:

Advertisement

In short, the big discrepancy between YOY and YTD tells us growth is slowing fast.